🌏 Overheard at NYCW '25

Move over, Climate Week, it was NY Energy & AI Week

Get Sightline’s signature H1’25 investment trends report inside

Today, we’re releasing Sightline’s H1 2025 Climate Tech Investment Trends report — your go-to recap of funding, deal flow, exits, investor activity, and what all this tells us about where climate venture and growth are headed.

Climate tech is settling into its new normal after last year’s funding freeze, and so far, 2025 hasn’t exactly thawed, but at least it’s not getting colder. H1’25 funding dropped 19% — better than H1’23’s 41% plunge, but still far from a rebound. We're calling this the end of the “see” in wait-and-see. Five to seven years into the current cycle, LPs are waiting for exits and liquidity — and not finding much.

But beneath the cooling headlines, a new investment thesis is heating up.

Rising protectionism is making access to domestic energy, critical minerals, and stable infrastructure a strategic priority. At the same time, with warming surpassing 1.5°C and climate impacts becoming harder to ignore, resilience is increasingly investible. Add a shifting macro backdrop — marked by weaker subsidies — and the market is moving from green premiums to green discounts. As the New Joule Order highlights, this may not be a bad thing: a security lens could lead to higher returns and a faster transition.

In H1’25, we saw this play out across multiple fronts:

And beneath it all, like this thesis, the capital stack is adapting. There are still surprises, some good news, and plenty to watch in the second half of this already-turbulent year.

We’ve rounded up the charts, trends, and takeaways below. Dig into the full report here.

Not a client yet?

Want to make sense of these trends (and what they mean for you)? We’re breaking it all down live next week in our webinar on July 8th, 11 AM EST, with Kim Zou, Mark Taylor, Julia Attwood, and Sophie Purdom. Sign up for the webinar here.

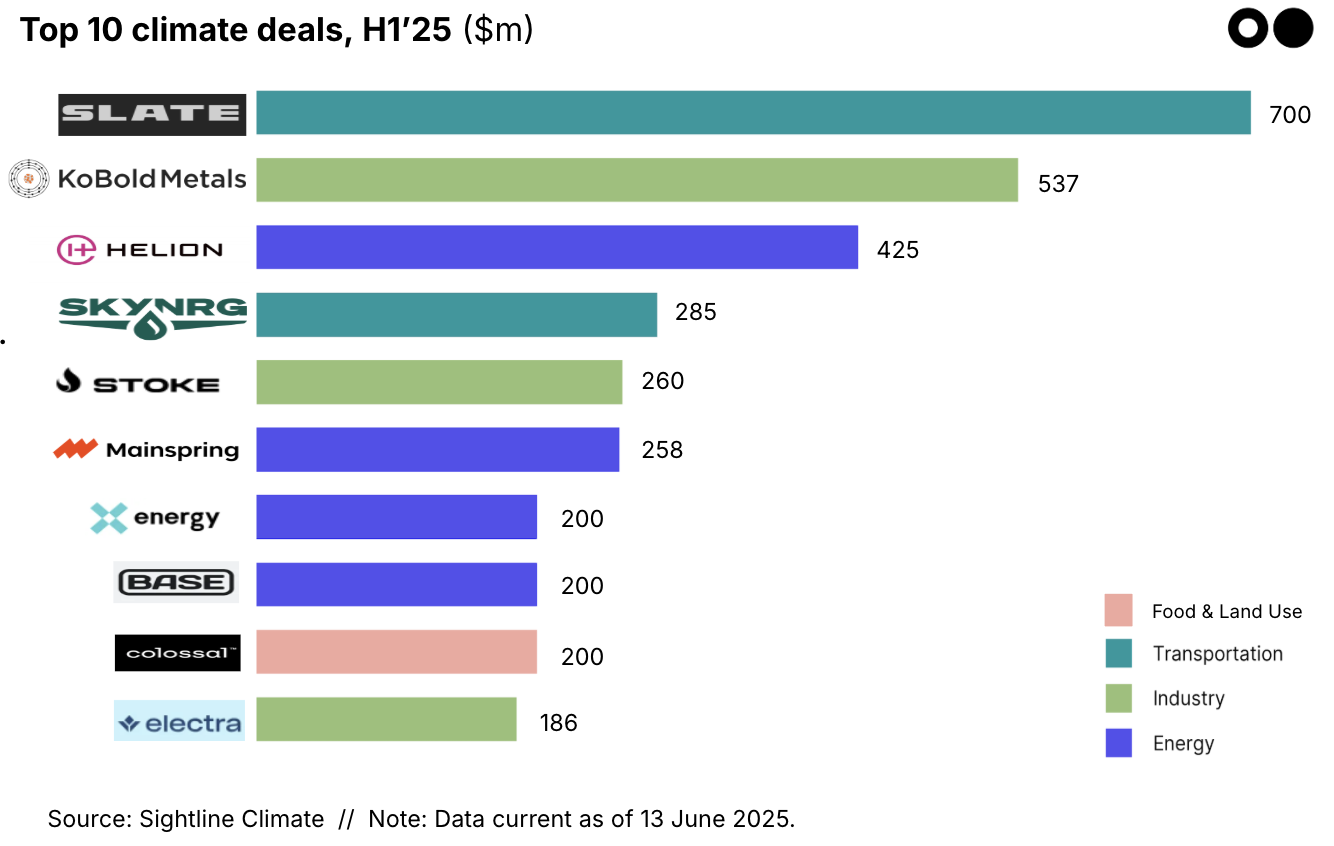

🎯 Security, adaptation, and resiliency come into focus: Mega deals reflected a growing focus on energy security and adaptation with nuclear, space, critical and strategic materials, and de-extinction all appearing in the top 10.

🇪🇺 Investor sentiment for Europe is strong, but it’s not showing up in the numbers yet: US investment rose 21% in H1’25 compared to H1’24, while Europe fell 51%. With very similar deal counts (259 in the US to Europe’s 248), it’s the mega deals keeping the US on top. Expect to see more project deployments and late stage investment moving to Europe in the next few quarters, but for now, US companies still command the largest investments.

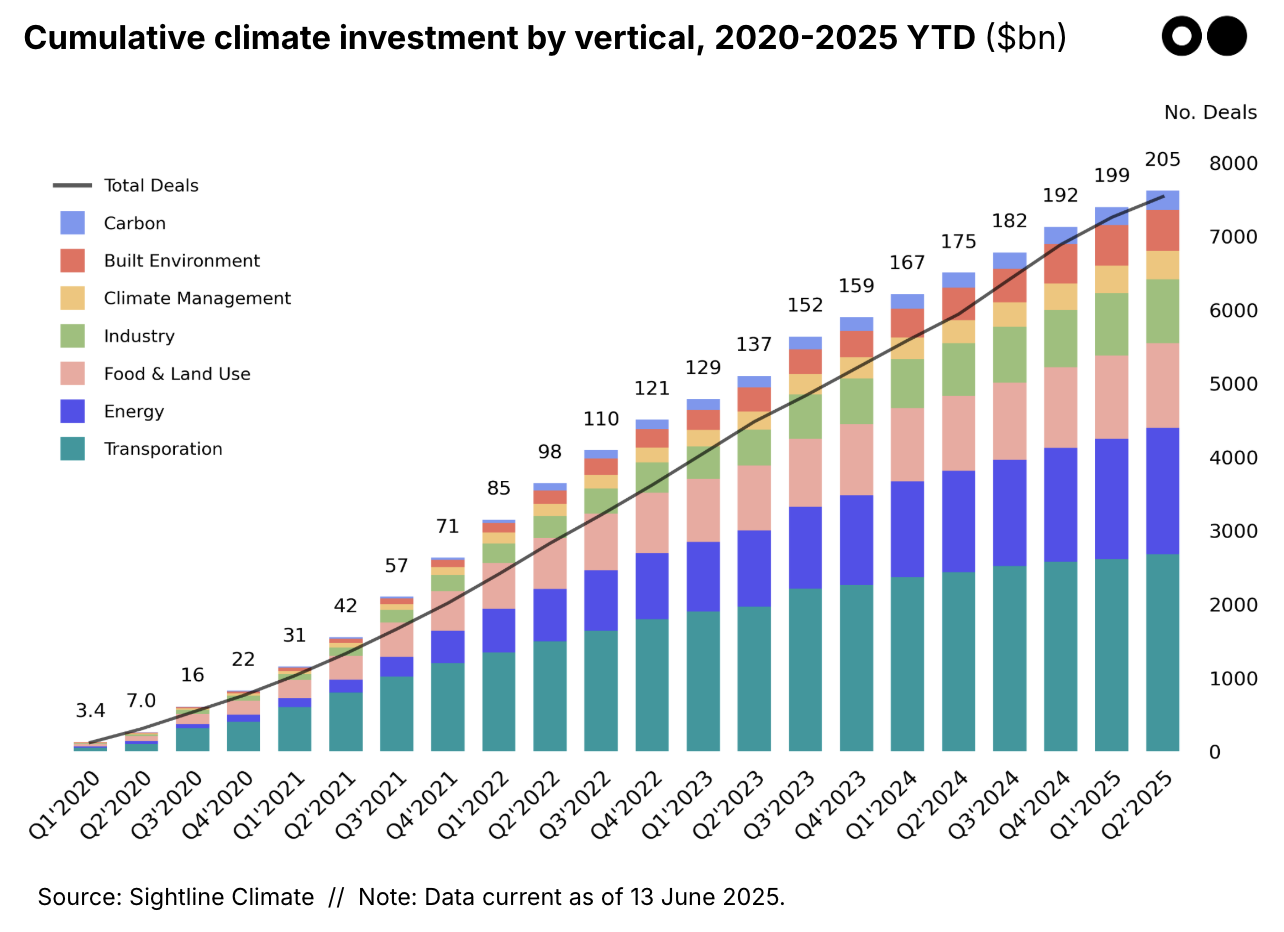

🏭 Industry sector funding holding steady is a victory: Industry has historically attracted patient capital geared toward large assets and hardware development. In today’s more conservative, asset-lite investment climate, that model faces headwinds — so funding holding steady counts as a meaningful win.

🚪 Exits (or lack thereof): SPACs have returned for not-yet-commercial climate tech like SAF and SMRs, while traditional IPOs are still scarce everywhere but India. Meanwhile, M&A activity is picking up — acquisitions doubled from H1’24. Bankruptcies slowed but still stung, with some former darlings going under this half, including Northvolt, Sunnova, and Li-Cycle, squeezed by policy changes and post-ZIRP macro headwinds. A quieter wave of companies unable to secure funding is also likely fading from view. Expect more consolidation soon.

And now, the stats you’ve been waiting for. Scroll on for a few key numbers — but download the full report for more analysis and what it all means for the rest of 2025.

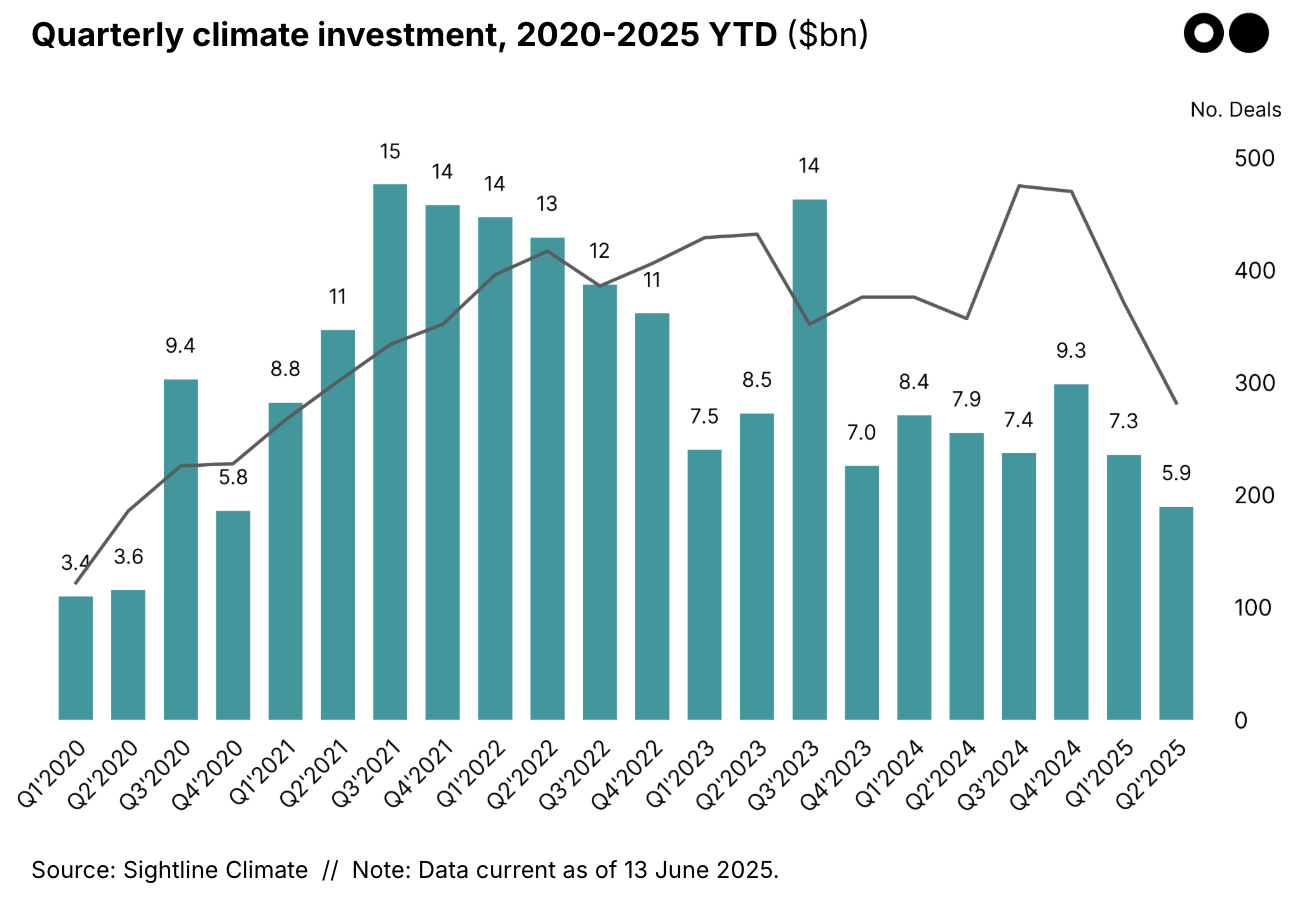

💰 H1’25 funding: Climate tech venture and growth investment totaled $13.2bn in H1’25, down 19% from H1’24, and 17% from H1’23. There were 653 deals in H1’25, 11% less than in the first half of 2024.

📈 Cumulative growth: H1’25 increased cumulative investment since 2020 by 7% to $205bn, but that growth is marching along at a slow and steady pace, compared to 10% growth in H1’24 and 13% in H1’23. Quarterly growth is decelerating too: just 3% in Q2’25, down from 5% last year and 7% the year before.

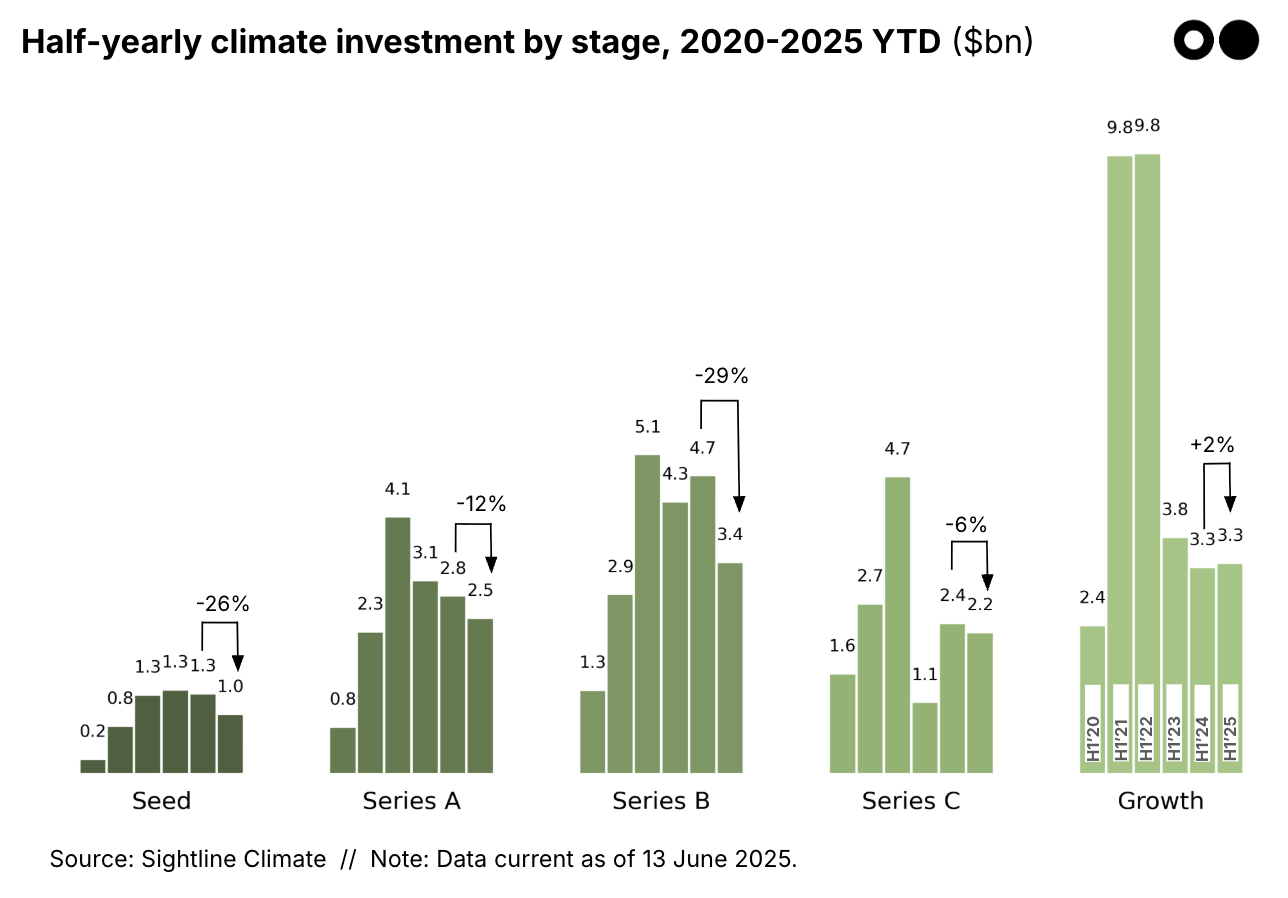

📉 Stage: Funding dropped across almost all rounds, with Series B down the most at 29% lower than H1’24. Seed funding wasn’t far behind with a 26% decline. Still, later rounds continued to appeal to investors, offering proven companies and more mature tech. Series C was only down 6%, and Growth investment actually went up very slightly, bolstered by mega deals in fusion and low-carbon fuels. [Get more insights into stage-specific investment, like deal size by stage, in the report.]

🤝 Top deals: Out of the total $3.3bn in mega-deals, $2.3bn and eight out of the ten deals focused on security, resilience, and adaptation. Security plays included funding for novel nuclear power (Helion, X-energy), critical and strategic minerals supply (KoBold, Electra), and space (Stoke). Notably, the average top 10 deal size was 31% higher than in H1’24.

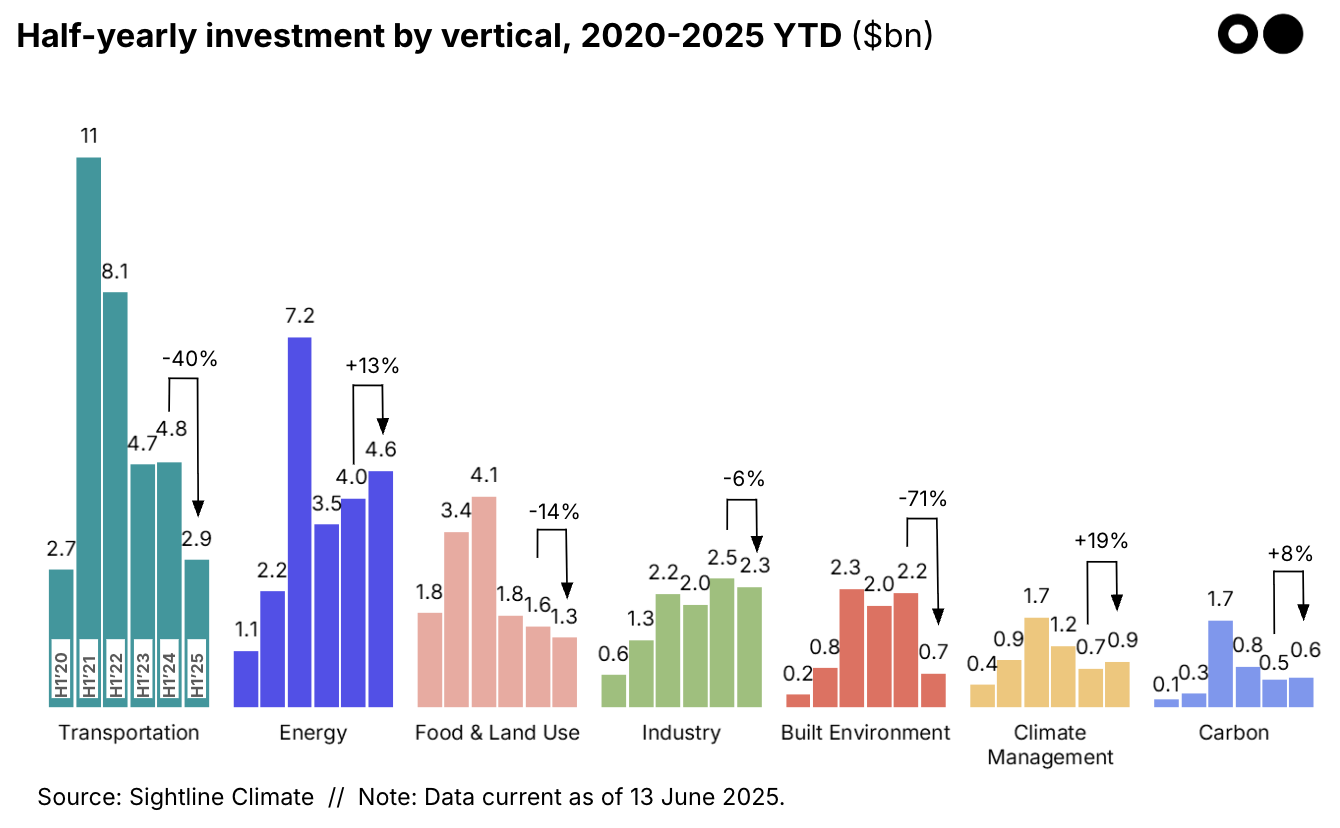

⚡ Vertical: Energy was once again the top vertical, with 35% of H1’25 funding. It grew 13% to $4.6bn. Fusion displaced energy storage as the second largest sector within energy. Meanwhile, earth observation funding jumped amid the renewed interest in climate adaptation. [Get more insights into vertical-specific investment, like breakdowns by vertical and sector, in the report.]

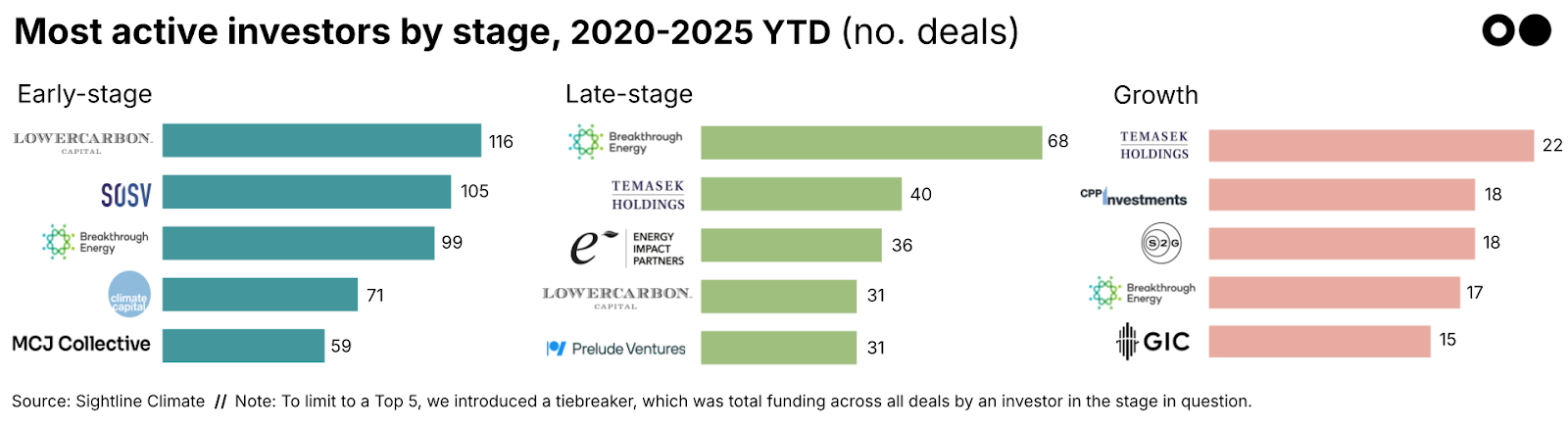

👔 Investors: The list of top climate investors changed very little as specialists doubled down with follow-ons and maintained deal count leads established in the 2021-2022 heyday. That said, a few shifts emerged: S2G replaced Goldman Sachs on the Growth leaderboard with deals in ag fintech and ocean data, and Lowercarbon’s Series B streak pushed it into later-stage territory.

This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of June 13, 2025. Read more about methodology and definitions in the methodology section of the full report.

NOTE: You may notice that some of our numbers are larger in this update than previous editions. We constantly update the dataset to have the most accurate data possible, including adding post-dated deals.

Have a different take on what’s driving these climate tech investment trends? Or questions about our analysis? Drop us a note at [email protected] if you’re looking to dig deeper into the H1 2024 funding numbers.

Move over, Climate Week, it was NY Energy & AI Week

Exclusive data and insights on the power behind the data center buildout

Survey results: what’s working, what’s stalled, and what’s missing