🌎 Climate brick by brick #194

A new framework for scaling climate tech companies, just in time for Earth Day

What two nuclear startups’ announcements mean for the future of fusion

Happy Monday!

SpaceX’s Starship isn’t the only thing taking off.

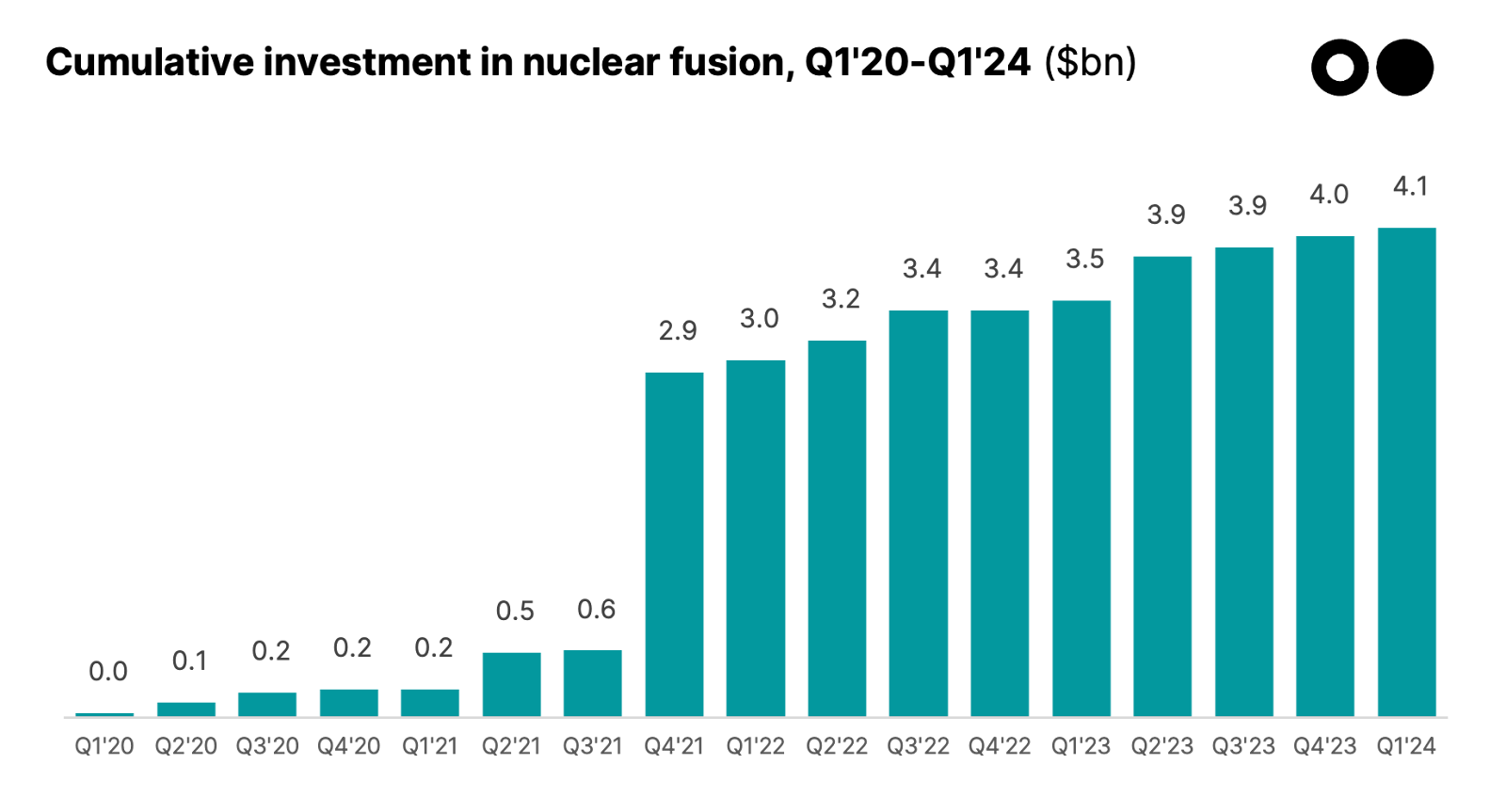

The nuclear fusion space is also seeing serious pedal to the metal. In the past month, two fusion startups, Longview Fusion Energy and Type One Energy, have announced construction and siting agreements for their pilots, marking the first signs of commercial progress. Both pilots aim to fully operate by the 2030s, although it remains to be seen whether or not these companies can overcome the sector’s challenges — such as securing adequate funding, overcoming engineering hurdles, and developing a reliable fuel supply — and meet those deadlines.

In other news, investments in small modular nuclear reactors (SMRs) have risen 60% over the last three years, while OPEC and the IEA’s oil demand forecasts are the most divided they’ve been since at least 2008. Plus, the first climate risk report from the EU is out.

In deals, $80m in modular direct air capture technology, $75m lithium-ion battery recycling, and a new $133m fund for deeptech early-stage companies.

Plus, we’re hiring! Sightline is looking for a Backend Engineer and a Research Intern.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

In the past month, fusion startups have been heating up. Following engineering breakthroughs and capital inflows in recent years, some startups are taking their first steps towards commercialization. On March 8, Longview Fusion Energy announced an engineering, procurement, and construction (EPC) agreement with Fluor for the world’s first laser fusion pilot plant, aimed at starting operations in the early 2030s. Meanwhile in late February, Type One Energy announced a site for its stellarator fusion prototype machine — a shuttered coal plant — for the same time frame.

Why now?

The Big Picture

On the plus side:

On the downside:

Looking ahead, it’s going to be all about timing, timing, timing. Many people working in fusion are confident that the engineering challenges will be overcome in the coming years. But there’s a big difference between the 2030s and 2040s — both for climate impact, and for how fusion will compete against alternative firm power sources like SMRs/nuclear, geothermal, and LDES. If fusion doesn’t get electrons on the grid before the 2040s, it will be competing with much more mature and established technologies.

Thank you to Dr Melanie Windridge and Andrew Holland for their expert confinement of the issues.

🏠 Sealed, a Queens, NY-based smart home retrofits platform, raised $30m in Growth funding from Keyframe Capital Partners, CityRock Venture Partners, Cyrus Capital Partners, and Fifth Wall.

🛵 VOI, a Stockholm, Sweden-based electric scooter platform, raised $25m in Growth funding from Balderton Capital, Black Ice Capital, Creandum, Nineyards Equity, Project A Ventures, and other investors.

🔋 Lohum, a Greater Noida, India-based lithium-ion battery recycling platform, raised $14m in Series B funding from Singularity Growth, Baring Private Equity India, and Vyoman Indian.

⚡ Mapon, a Riga, Latvia-based fleet management software platform, raised $3m in Debt funding from Signet Bank.

💨 CarbonCapture, a Pasadena, CA-based modular direct air capture technology platform, raised $80m in Series A funding from Prime Movers Lab, Alumni Ventures, Amazon Climate Pledge Fund, Aramco Ventures, Idealab, and other investors.

⚡ Quaise, a Cambridge, MA-based geothermal drilling technology platform, raised $21m in Series A funding from Prelude Ventures, Safar Partners, Mitsubishi Corporation, and Standard Investments.

🥩 ProteinDistillery, an Ostfildern, Germany-based plant-based food platform, raised $16m in Seed funding from Green Generation Fund and Startup Family Office.

🔋 Pure Lithium, a Boston, MA-based lithium metal electrodes developer, raised $15m in Series A funding from Oxy Low Carbon Ventures.

⚡ SUBLIME, a Paris, France-based biogas liquefaction technology platform, raised $13m in Seed funding from Crédit Mutuel Impact and PSL Ventures.

📦 Packfleet, a London, UK-based electric parcel courier service provider, raised $10m in Series A funding from General Catalyst, Creandum, and Voyager Ventures.

🧱 Furno Materials, a Palo Alto, CA-based retrofittable oxyfuel in cement plants platform, raised $6m in Seed funding from Energy Capital Ventures, Breakthrough, Cantos, Neotribe Ventures, and O’Shaughnessy Ventures.

⚡ Necture, a Vienna, Austria-based EV fleet management platform, raised $6m in Series A funding from SmartEnergy Innovation Fund, Smartworks Innovation, Speedinvest, and Verbund X Ventures.

🚗 Telo Trucks, a San Carlos, CA-based small electric vehicles manufacturer, raised $5m in Seed funding from Spero Ventures.

🛰 MarineLabs, a Victoria, Canada-based real-time coastal intelligence platform, raised $4m in Seed funding from BDC Capital and Seaspan Shipyards.

⚡ Suiso, a Sheffield, UK-based hydrogen generation technology platform, raised $4m from NPIF - Mercia Equity Finance.

🛰 Orbio Earth, a San Francisco, CA-based methane monitoring platform, raised $4m in Seed funding from Initialized Capital, Collaborative Fund, Y Combinator and the European Space Agency.

🔋 Anaphite, a Bristol, UK-based dry coating composites for batteries platform, raised $2m in Equity funding from Elbow Beach Capital, Bristol Private Equity Club, and Wealth Club and Grant funding from Investor Partnerships Future.

🥩 Opalia, a Montréal, Canada-based cell-based dairy platform, raised $1m from Hoogwegt Group, BoxOne Ventures, Cycle Momentum, Kale United, Natural Products Canada, and other investors.

🔋 Li-Cycle, a Mississauga, Canada-based lithium-ion battery recycling platform, raised $75m in Convertible Note funding from Glencore.

🔋 Vianode, an Oslo, Norway-based sustainable anode materials manufacturer, raised $33m in Grant funding from Innovation Norway.

💨 Carbonova, a Calgary, Canada-based carbon nanofibers from CO2 platform, raised $6m in Corporate funding from Kolon Industries and NGIF Capital.

Elaia, a Paris, France-based investment firm, announced the launch of a $133m fund that invests in deeptech early-stage companies.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate

The last three years saw a 60% increase in pipeline for Small Modular Nuclear Reactors (SMRs), driven by interest from heavy industrial players. This pipeline represents 22GW of projects with over $157bn in potential investments. Although the vast majority of the world's SMRs are not yet under construction, the first SMR was activated last year, marking an important milestone for the industry.

In a promising yet gloomy step forward, the EU issued its first climate risk report, which found there were steep consequences ahead if no action was taken by the bloc. The report mentioned particular regions were especially vulnerable, such as Southern Europe to wildfires, low-lying coastal regions facing flooding, and heat as the top issue overall. It further stated that Europe’s technology and policy deployment was not on pace with these growing risks.

In a race to secure critical minerals onshore, the US DOE offered a $2.26bn loan to Lithium Americas Corp. to develop the country’s largest lithium deposit in Nevada. This is the largest-ever loan to a mining company from the DOE’s Loan Programs Office, and the plant is expected to produce 40,000 metric tons per year of battery-grade lithium carbonate for use in EV batteries. Indigenous American tribes objected to the location of the mine, but lost a legal case last year to block its construction.

New York State completed its first offshore wind farm off of Long Island. South Fork Wind is fully operational and delivering power to over 70,000 homes and businesses in the area. This is the first commercial-scale project in the US to be completed, and marks a huge milestone for an industry hard hit by inflation and high interest rates.

OPEC and the IEA are the most divided on oil demand since at least 2008, according to a new Reuters analysis of the last 16 years of monthly reports. The gap in demand between these two organizations’ reports, around 1% globally, reflects competing worldviews about the pace of the energy transition — and could have dire consequences in terms of potential investments and effort put into the transition.

Shell further weakened its 2030 energy transition goals. The company cited expectations of continued gas demand, particularly LNG, leading to rolling back some of the decarbonization goals it had previously laid out. In addition to scaling back its 2030 goals, it completely scrapped the 2035 target for net zero, and introduced a target to cut emissions from oil sales instead. [See full report here].

The DOE is getting busy with carbon removal programs. The three programs include: the Voluntary Carbon Dioxide Removal Purchasing Challenge, a $35m Carbon Dioxide Removal Purchase Pilot Prize, and Carbon Negative Shot Grant Funding Opportunities. Google has further agreed to match the programs’ funding for companies and projects that win. These policies and prizes aim to accelerate technologies like DAC and simultaneously bolster the carbon market in the US.

Amazon announced it bought a nuclear powered data center campus in Pennsylvania from power company Talen Energy for $650m. One driver for the increase in data center electricity demand: the use of generative AI. One report shows that if Google were to integrate generative A.I. into every search, its electricity use would rise to around twenty-nine billion kilowatt-hours per year — more than is consumed by many countries, including Kenya, Guatemala, and Croatia. Meanwhile KW Sidewalk Infrastructure Partners issued a call to action paper on data center flexibility and sustainability.

From green snowmobiles to giant wind turbine carrying planes, new hardware hopes to take off.

Welcome to the jungle! From the UK's rain-kissed redwoods to NYC's mini-forest marvel.

CarbonPlan publishes a revealing database on carbon offsets.

Blast from the past as the UK returns to emissions levels from 1879.

A bitter future for sweet stone fruits.

US methane leaks are bigger than we thought.

Massachusetts residents see $600k flood defenses destroyed in under 72 hours.

Bloomberg is on an emission mission with $200m announced for emissions reduction in 25 US cities.

America’s 2024 Greentech greats.

Night time solar reflects the take off in satellites.

Could adaptation be the next Climate-Finance Gold Rush?

📅Latin America Climate Finance Accelerator: Register for the Climate Finance Accelerator's virtual events on March 19-21st for an opportunity to join networking spaces and learn about climate innovation, low-carbon infrastructure, and impact investment in Latin America.

📅 ChangeNOW Summit: Register for the ChangeNOW Summit in Paris from March 25-27th for an opportunity to connect with thousands of other climate professionals, attend insightful workshops, and discover innovative climate solutions.

📅 Climate Career Week: Register to attend the Terra.do Climate Career Week from March 25-29th to join others in five days of free virtual programming and meet leading climate founders, investors, and experts in the climate tech industry.

💡 Climate Challenge: Apply to the THRIVE Climate Challenge by March 29th for a chance to receive a $100k investment from THRIVE and join their 2025 global accelerator for startups advancing the biofuels value chain, on-farm energy, and water stewardship.

💡 Biomimicry Accelerator: Apply to the Biomimicry Institute Fifth Ray of Hope Accelerator Cohort Class by May 3rd for opportunities to access robust training, networking, and $15,000 in non-dilutive funding for nature-inspired startups addressing environmental challenges.

Backend Engineer, Research Intern @Sightline Climate

Founder, Enteric Methane (Microbiome Scientist); Founder in Residence, Geothermal @Marble

Community Engagement Lead, Controller, VP Project Development @Planetary Technologies

Program Manager @Evergreen Climate Innovations

Managing Director, Strategy and Operations @Invest in Our Future

Technical Project Manager/ Engineer @Aeromine Technologies Inc.

Climate Finance Specialist (Clean Energy); (Adaptation); (Value Chains) @U.S. DFC

Associate - Industrial Decarbonization; Chief of Staff, Investor Ops @LowerCarbon Capital

Associate Program @Collaborative Fund

Director, Private Investment @Builders Vision

Technology/Building Controls Researcher @Lawrence Berkeley National Laboratory

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

A new framework for scaling climate tech companies, just in time for Earth Day

Tech companies and utilities cover their bases as data center electricity demand skyrockets

A new green bank to finance climate projects

Newsletter

Newsletter