🌍 Rise of the robots, NY Tech Week edition

What happens when climate tech meets robotics

The future is unknowable, but it’s not unimaginable. Luckily, we can phone a friend - in this case 15 clairvoyants - for a sneak peek into the future. And because we can’t help ourselves, we then attempted to extrapolate the straight line between these divergent views of what’s to come for climate tech in 2024. Read on to hear our expert views, or take your foresight test here.

But first, a quick retrospective. This past year’s challenge has been all about getting commercial deployments to ‘become boring’ - when climate tech works so well that it’s unremarkable, when breakthroughs are so widespread that they’re innocuous. But we’re not quite at the point of churning projects out as fast as the bank can finance them or the developer can build them.

2023 raised these hurdles several inches higher – steep interest rates shortened the clock, giving many less time to make the leaps, leading to canceled projects and a subsequent drop in funding. But it was also a year where the worlds of policy and finance became leading - not lagging - indicators. IRA led the way, allocating money and flexibility to maximize impact, while a more sophisticated climate stack stepped up with innovative asset layers like emerging infrastructure to bridge the gaps.

Meanwhile, CTVC continued to grow, passing 60,000 industry leading readers. For us this year’s hurdle was to move from delivering point-in-time insights on climate tech to building a platform that could be a single point of reference for the space. Since we launched Sightline Climate, we’ve had the chance to help dozens of clients – from investors to corporates to governments – understand key climate tech sectors; how they work, who’s playing, drivers, obstacles, and how close they are to the promised land of ‘boring’.

Thanks for looking forward, backward, and into the depths of your inbox with us every week. Most grateful for your perpetual belief that all of this matters. We’ve got a long way to go!

Take the 2024 Oracle Survey and we'll publish your predictions in a future issue.

In 2022 total funding was $40B, in 2023 (as of end-November) the total is $28B.

Shayle Kann, Energy Impact Partners: Yes. We may not quite reach 2022 levels, but the trend line will bend upwards again as companies who have pushed off major fundraises go out to market in 2024 while early stage activity remains strong.

Lara Pierpoint, Prime Coalition: Yes. I don't think we'll get back to 2022 levels just yet, but the urgency is increasing and I think the number and commitment level of funders will go up next year.

Shanu Mathew: No. Investors are cautious given public markets activity and broader weaker macro sentiment. A lot of private capital funds are freezing up and too scared to have conviction right now.

Andrew Beebe, Obvious Ventures: Yes, 2024 will beat both 2023 and 2022.

Dawn Lippert, Earthshot Ventures and Elemental Excelerator: Beyond venture it will get creative. Funding will increase with many more types of funders: more federal funders (i.e., EPA with the Greenhouse Gas Reduction Fund), green banks, philanthropy, and blended finance vehicles like those we’re building at Elemental to fund early project finance and bridge the giant climate funding gap.

Kiran Bhatraju, Arcadia: Yes. I think investors will start to see IRA dollars flow, softening interest rates, and continued progress and milestones from bets made over the past few years unlocking new technologies and markets.

Ally Yost, Commonwealth Fusion Systems: Yes. Funds that raised in ‘21/’22 with a climate focus will have increasing pressure to deploy dry powder. But investors will be more likely to syndicate and pile in to more clear winners to reduce being perceived as too risky, resulting in more total dollars but going to a more concentrated set of companies. We'll also see more generalist VCs lean into climate tech as it becomes increasingly "the thing" - jury is out on if this will be helpful or harmful.

Mike Schroepfer, Gigascale Capital: YES! 2023 was a year of re-adjumented from an over-jubilant 2021 and 2022. However, the fundamentals driving the energy transition are stronger than ever. $500b in Solar investments in 2023 (up 75% y/y in US), 50% y/y growth in EVs in the US, and battery prices continuing their downward march another 50% by 2030 means many $1t industries are ripe for disruption. This is one of the best times to be investing in this sector I’ve ever seen.

Joshua Posamentier, Congruent Ventures: Yes. I think climate venture will be flat to slightly up given the trend in 2023 to push out fundraising for later stage companies that may still need to grow into their prior valuations. The overhang of committed venture dollars will also create pressure to invest.

Shayle: Yes. I expect there will be more flat/down/structured rounds in 2024 relative to 2023, as many companies have been electing to accept significant structure in order to avoid a lower headline price and we haven't quite worked through the backlog of companies with valuation overhang from their previous rounds in 2021/early 2022 yet.

Lara: Yes. More flat and down rounds (and insider rounds) than 2023. Investors are skittish about the bigger stages and will remain so next year.

Sean Hunt, Solugen: Yes, most climate tech companies are private and private market valuations are a long lagging indicator of equity valuations. Potentially a fair number will go under in 2024, again as a lagging indicator.

Shanu: Yes. Many raised at peak optimism and euphoria, meaning a lot will need bridge rounds to stabilize runway or reset valuations at lower levels to attract new capital in the tougher environment.

Kiran: Yes. More flat, more down, and more structure. I think the seed deals from the past few years were still a bit crazy while growth valuations fell off a cliff. There's a mismatch that will get corrected at the A and B rounds.

Ally: Yes, but counteracted by more up rounds. Companies who have worked to extend their runway will run out of money. But a good set of companies that achieve clear value creating milestones - hardware demonstrations, pilots plants getting off the ground, factories being stood up, first commercial deals, etc - will also be able to raise and do so at a (responsible) uptick.

Amy Duffuor, Azolla Ventures: No, I believe that the market will start to (slightly) improve although it depends on stage, - early-stage will see no more flat/down rounds compared to 2023 but growth stage will.

2 out of the 3 most active acquirers in climate tech since 2021 were O&G companies.

Shayle: Yes - oil and gas companies remain acquisitive, deep-pocketed and interested in having a play in major areas of climate tech. Look particularly for the sectors that are adjacent or similar to their core businesses (molecules).

Sean: Yes, it could be a good match for folks to exit after they can't raise and for O&G companies to make low cost acquisitions and "acquihires".

Dawn: An optimistic No. A tremendous amount of funding from outside O&G is flowing into the space next year, both from the $27 billion Greenhouse Gas Reduction Fund and from private funding. Tech and corporates are back at the table as of the last few months of 2023, and I think will be active acquirers in 2024.

Akshat Rathi, Bloomberg News: No, not for the big and promising climate tech startups, especially given how oil & gas companies are currently behaving. Right now they’re holding cash from high oil prices, doing share buybacks and dividends. US oilcos are buying companies, but mostly other oil companies, and EU ones are shedding their renewable / clean businesses. Don’t see them suddenly shifting gears to acquire big promising startups. Oxy buying Carbon Engineering was an exception that had been in the works for a while.

Bob Mumgaard, Commonwealth Fusion Systems: Yes. But few acquisitions overall. O&G is going to continue to consolidate their own industry and those that are related (methane, CCUS, software stacks) will get eaten up. But don't look for a resurgence of BP-Beyond Petroleum “we'll do solar”.

Keeton Ross, Holocene: YES. You'll see a lot of companies run out of money / realize the business isn't there, and look for an exit. O&G have the most flexibility and cash flow to take a small bet and pick up the scraps. I think if utilities had more cash flexibility they'd do more acquiring, but their regulated structure makes it tough.

Joshua: No. The recent retrenchment of the oil supermajors makes me think that there may be more non-traditional buyers of climate startups. This will undoubtedly include other public companies (energy, chemical, manufacturing, software) but also private equity acquirers for those with some semblance of cash flow and/or roll-up opportunities.

Sean: Yes. I could see an executive order from either party aiming to encourage redirection of funds in certain directions. Unlikely congress is functional enough for a meaningful overhaul, but Democrats could make alterations to reflect changing sentiments/campaign promises. Republican directives would be more extreme.

Paul Martin, Spitfire Research: Yes, very sadly. Would the IRA survive election of Trump as president? No, it wouldn't. It'd be dead in a month.

Akshat: No, but this is a wild one — I’m seeing signals from both sides. Democrats say it’s real money going into all states, red states included. Republican leaders have applied for funds and factories and plants to go to their states. They want the jobs. But American politics is crazy and unpredictable, so it’s hard to say for sure, but given that incentives are going to Republican states, some of it, if not all of it, will remain intact regardless of the outcome of the election.

Kiran: The IRA passed in August 2022 but very few people have seen any benefit yet. I've been told by many technocrats that it takes over a year to get dollars out the door. If we get dollars out, get customers savings, do some ribbon cuttings, and prove America can do/build awesome things and lead on technology then partisan politics won't matter.

Bob: No. There will be lots of complaining and grandstanding but the money will still flow. IRA is going to jobs in red states and Congress is not going to be able to reverse it. Obamacare is the analogy. Bigger problem will be the size of tax credit markets, supply chains, and firm offtakes.

The S&P Global Clean Energy Index tracks the market value of 100 clean energy companies from around the world. The fund rose rapidly in 2020, from a little over $750 to topping out at over $2,000 in January 2021. In 2023, it declined to its current position under $900.

Shanu: A recent Bloomberg survey suggested 57% of investors think the selloff continues into next year.

Andrew: Yes. When rates start moving down again, we'll see it climb over 1500. If Biden gets elected, over 2000 by year end. Trump: below 1000

Joshua: Yes. I think it will slowly trend back over $1200 over the course of the year given stabilization and growth in its components. Goldman Sachs and other banks forecast a drop in interest rates as early as July 2024 which, if true, will drive more growth from the power producing components in the index and follow on to the equipment makers.

2023 saw investigations highlighting issues with carbon offsetting projects that weren’t delivering what they’d promised. The VCM has been estimated at ~$2B in 2023.

Shayle: Yes. We're in for a significant reckoning in the VCM, and I expect buyers to pull back while the market sorts out what is real and what is not. In contrast, the CDR market (particularly for verifiable, durable removals) will continue to grow from a smaller base.

Sean: No. Big demand funnel even with the lower quality credits exiting the supply.

Andrew: Criticism of the VCM is fair, but it can also work with the right support creating transparency, cross-border mechanisms, and trust (see portco Senken). We have no option other than to plug the holes and get this market moving (while reducing and in-setting everywhere else).

Akshat: Yes, it will likely shrink. But this could be a good thing. There has been an oversupply of low-quality offsets in the market. A market contraction could refocus on only the highest, or at least higher, quality assets. An Article 6 agreement at COP could be the wildcard here. It could stir a new round of growth, but in that case the strength of the offsets would still be in question.

Joshua: No! It’ll grow in terms of dollars even if it shrinks in terms of tonnage. It’ll be a flight to quality.

The expectation for DAC costs today is $600-$1,000 a tonne, but has been reported to be able to get to $150 a tonne by 2050.

Sean: No. If there is, it would be an investor subsidized sales price. Hard to envision the cost structure enabling this in the absence of fully depreciated CAPEX.

Shanu: I’d be shocked if all these commercial agreements are anywhere near these values for meaningful volumes but hard to get actual verbiage from buyers/sellers. But, I’d bet not.

Paul: No, not without hidden or overt subsidies to pay the cost difference between $600 and reality. DAC is structurally expensive for reasons you can’t fix with innovation. It's a predatory delay strategy and a fossil fueled meme, not a decarbonization strategy.

Keeton: Yes. I hear Oxy is already doing this and so is CarbonCapture (in their Frontier deal it was <$600/tonne). But price does not = cost, so it doesn't matter. Think about scale. DAC plants are going from thousand tonne to million tonne facilities. You can easily go 10x down in price, probably more like 20-50x at that range.

In 2022, 14% of all new cars sold were electric, up from 9% in 2021 and less than 5% in 2020.

Lara: Yes, but primarily driven by sales outside the U.S.

Shanu: No. Based on my math/dataset EU5+China+US was ~16-17% YTD thru Sep-23 and 4Q23 isn’t expected to be a blowout. Slowing penetration/environment might mean even falling short in ’24.

Paul: No, but it might get close. It will be hampered not by a lack of demand, but by a lack of supply of sufficiently affordable EV models outside of China, from vendors who really want to sell them, rather than using a small sales volume as basically "compliance cars".

Amy: Yes, but only if there are more chargers installed that are also reliable, which is a huge pain point for consumers.

Joshua: Not in the US. Trends are slowing and will only pick up significantly when the state of the non-Tesla charging networks improves. 1/3 of Americans rent their home, making charging more challenging, and 1/3 of Americans have no garage in which to charge. Infrastructure is important.

Andrew: The fast-charging chicken-and-egg issues as well as costs will constrain this transition slightly. However, this level of global scaling was simply not considered remotely possible 5 years ago, so let's not beat ourselves up here.

In 2023 interest in the geologic hydrogen extraction rose, with US DOE providing $20M in funding and startups like Koloma raising venture capital. Geologic hydrogen has been accidentally discovered before, with a site powering a town in Mali today, but will 2024 see an intentional project launch and successfully demonstrate that it can be commercially viable?

Shayle: Yes, it’s coming.

Paul: I doubt it. My real concern with geological hydrogen is that minor hydrogen content will be used to greenwash natural gas and used as an excuse to produce a fossil gas stream which contains SOME hydrogen.

Joshua: I think it will likely be 2025 before we see commercial extraction given the subsurface and surface EPC work, timelines, and logistics.

Andrew: Geologic H2 is a powerful idea, but as with all silver bullet solutions, it will take time to get to (below) ground truth in terms of availability, access, purity and transport.

eSAFs or ‘electrofuels’ are synthetic fuels derived from renewable energy.

Lara: No. I think this market is moving way too slowly. HEFA may be slightly more likely but I'm not seeing real efforts from airlines.

Sean: Yes. I could see a PR stunt with a very expensive tank of e-SAFs on a small plane.

Shanu: No. Depends on the flight (and how much fuel needed). The first transatlantic flight using 100% SAF happened recently but I’m unsure if we have commercial production/trials ready for e-SAF.

Paul: No, for a commercial jet airliner for regulatory reasons alone. I don't think e-SAFs are ever going to be a thing. They are so structurally inefficient that we'd need to be both very rich and very desperate to ever use them. Biofuel SAFs are the only game in town that makes chemical engineering sense. And they will be greatly more expensive than fossil jet fuels, so it will take real policy measures- taxes and emission bans- not voluntary actions by airlines, to transition flight to lower GHG options.

Mike: We could do it today, it would just cost a fortune and thus be a stunt. The real question is when can e-SAFs get within 2x of traditional JetA at any reasonable volume. That’s gonna take a while unfortunately.

Keeton: Does it matter? eSAFs won't be economical. We know you can make them so I'm not sure this would be anything more than a buzzy news article until we find a path to affordability, a carbon tax, or a recognition via consumers that they are "worth" paying for.

Bonus: What will be the buzzy topic in 2024? What will we all be talking about?

Shayle: Industrial heat!

Lara: Repowering fossil electricity production and powering data centers (sometimes together). I don't know if "buzzy" is the right word, but I'm all in on industrial partnerships, electrification, and repowering in 2024!

Sean: The peaceful transfer of power coming up in January 2025.

Shanu: Clean firm power – people are waking up to the fact that we can’t do all solar/wind, and batteries won’t fill in the gap everywhere, so there’s a lot of chatter around a nuclear/geothermal renaissance. Check out uranium spot prices and the announcement that Google-Fervo’s first-of-its-kind geothermal project is now operational.

Andrew: Fusion and small modular fission reactors. Generative AI for advanced chemistry of batteries and solar cell designs.

Dawn: Investments and projects coming online in Justice40 communities and starting to deliver real benefits. A year and a half into the IRA, we’ll see more projects in the ground and local news covering them…fingers crossed.

Akshat: Marine CO2 removals, because all CO2 techniques right now that can scale are quite expensive and energy intensive and their economics will keep them expensive. Marine CDR has potential to scale at low energy consumption and potentially minimal environmental impact. Some interesting scientific studies currently going on, if the results are favorable, we could start hearing more about this.

Kiran: Nuclear. Vogtle is complete and the Barakah UAE project is almost ready to provide 1/4 of the country's energy. Both projects are large with Vogtle being one of the largest union deployments in history. I think governors will be lining up to be the next state in the US to build nuclear, attracting data centers for AI and new industry…they just have to convince their utilities to take the risk and not put all the downside on ratepayers.

Bob: Checking my hype-o-meter. What was hot this year? DAC, Voluntary Carbon Markets, Nature based solutions. What faded out? Synthetic meat, EV trucking. The hot topic of December 2024 is going to be....carbon-market derivative banking (save us).

Ally: I think more people, and more mainstream discussions, will finally connect the dots that AI and climate tech are inextricably linked. If you believe in AI you better believe in finding clean solutions to power it.

Amy: All things methane!

Keeton: I think one of the fusion start-ups will demonstrate something wicked cool – but I don't think it will matter for *on-earth* climate, b/c it won't be an affordable power source.

Enough from the oracles - what do you think? Follow this link and send us your answers and comments and we'll publish them in a future issue. It’s your turn!

What happens when climate tech meets robotics

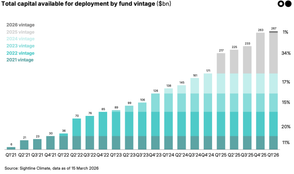

$90bn in climate dry powder in Q1 2026, after record fundraising in 2025

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

Newsletter

Newsletter