🌏 Hot off the press: China’s 15th plan for the era of security

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

Happy New Year 🎉 We’re glad to be back in your inbox after a little R&R over the holiday break, and we’ve got one last gift for you: our 2024 Climate Tech Investment Trends report, live now.

It’s our fourth (!) year releasing this report, and while the climate capital stack has expanded and matured since we first started out, the VC layers are still crucial. They serve as launchpads for getting innovative climate technologies out of the lab and into the world as FOAK plants or new products — and we crunched the numbers to show just how much.

This 2024 Climate Tech Investment Trends report has all of the funding and deals data by stage, vertical, and product type, but we also have a whole other layer of analysis just for clients. Sightline Climate clients can access the full report and underlying data pack, with complete data and analysis of 2024 climate investments across graduation rates, sectors, ‘first-of-a-kinds’, exits, investors, geography and product type via the platform here. If you’re interested in becoming one, request a demo here.

📊 So what does the data say? Investors didn’t fully push the restart button in 2024, as the 2023 “wait-and-see” crowd had hoped. The still-high interest rates, delayed IRA funding rollouts, and political uncertainties created headwinds that hit strategies and deployment. Don’t expect to see another 2021/22 ZIRP-fueled funding mania anytime soon.

But 2024 did bring fits and starts of opportunity and optimism for the sector. AI spurred clean firm power, Europe strengthened carbon markets, and emerging economies’ climate tech demand opened up. Hesitant investors now have more clarity around interest rates, geopolitics and policies, and exits (the good kinds, and the bad kinds). Mainstream infrastructure and growth investors increasingly view climate infrastructure as just, well, infrastructure.

Buckle up as we speed through a TLDR of the report in this newsletter. But you can sit back and enjoy the ride with the full public version, with additional charts and commentary here.

📅 And if you want to dive in even deeper (and get access to some more insights), join us for a webinar on Thursday, January 23 to review key highlights from this and our recent climate capital stack report with Sightline Co-founders Kim Zou and Mark Taylor to get our take on what’s to come in 2025, followed by an audience Q&A.

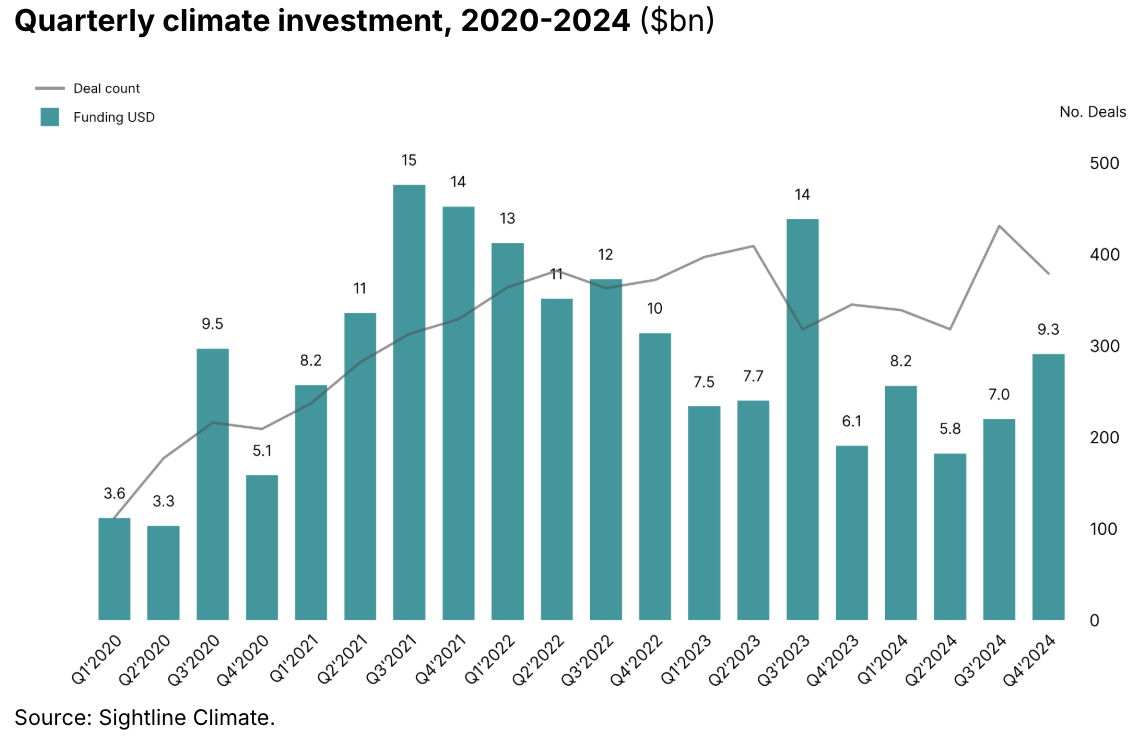

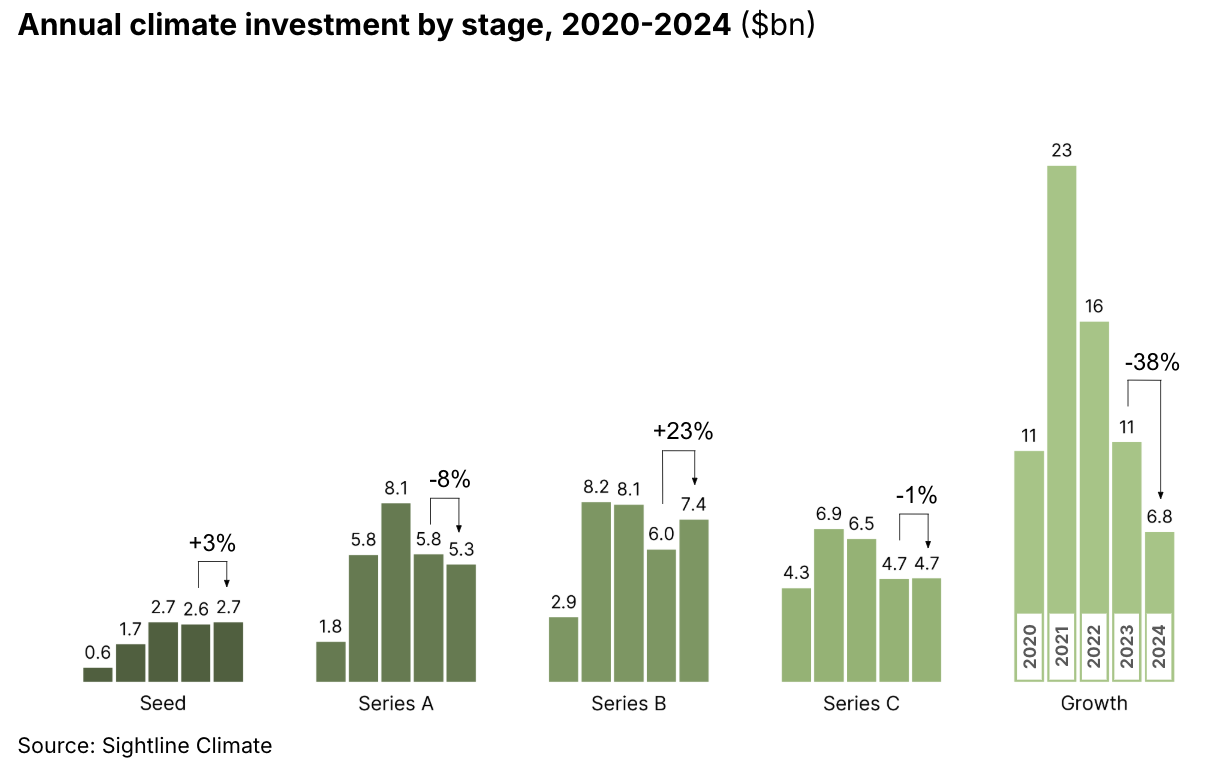

💰 2024 investment: Venture and growth investment in 2024 totaled $30bn, down 14% from 2023, much less than the previous 24% drop, showing the sector settling into a new normal.

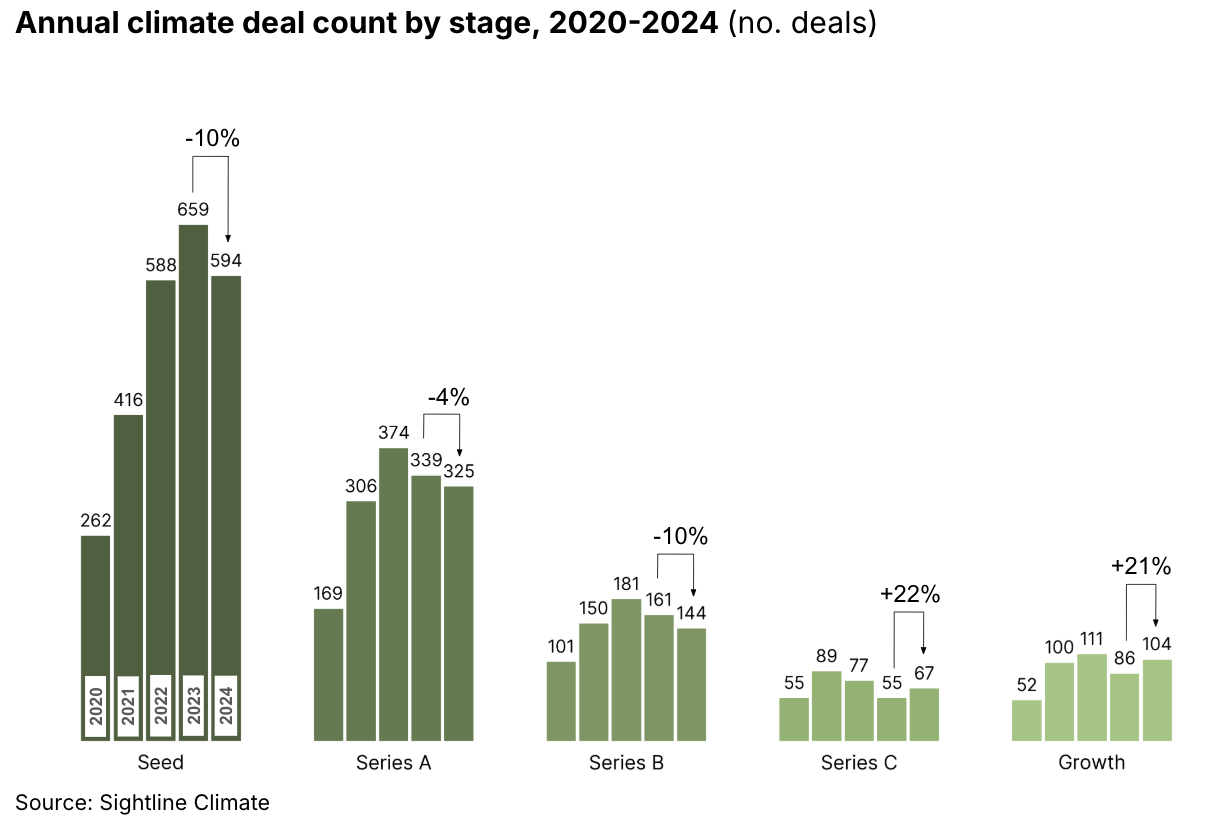

🤝 Deal count: Deal count was relatively flat, at 1,460 in 2024, compared to 1,468 in 2023 — but with increases in later stage deals as climate tech sectors mature.

📉 Late: Investment in Series D and beyond fell 38%, while Series C was essentially flat at 1% lower. Deal counts for both were up about 20%.

📈 Early: Seed and Series A split on investment trends, with Seed up 3% and Series A down 8%. Deal counts for both were down, Seed by 10% and Series A by 4%.

💸 Round size: Average deal size fell 14% to $24m. Growth deal sizes were down a dramatic 48%, but Seed and Series B were up 12% and 38% respectively.

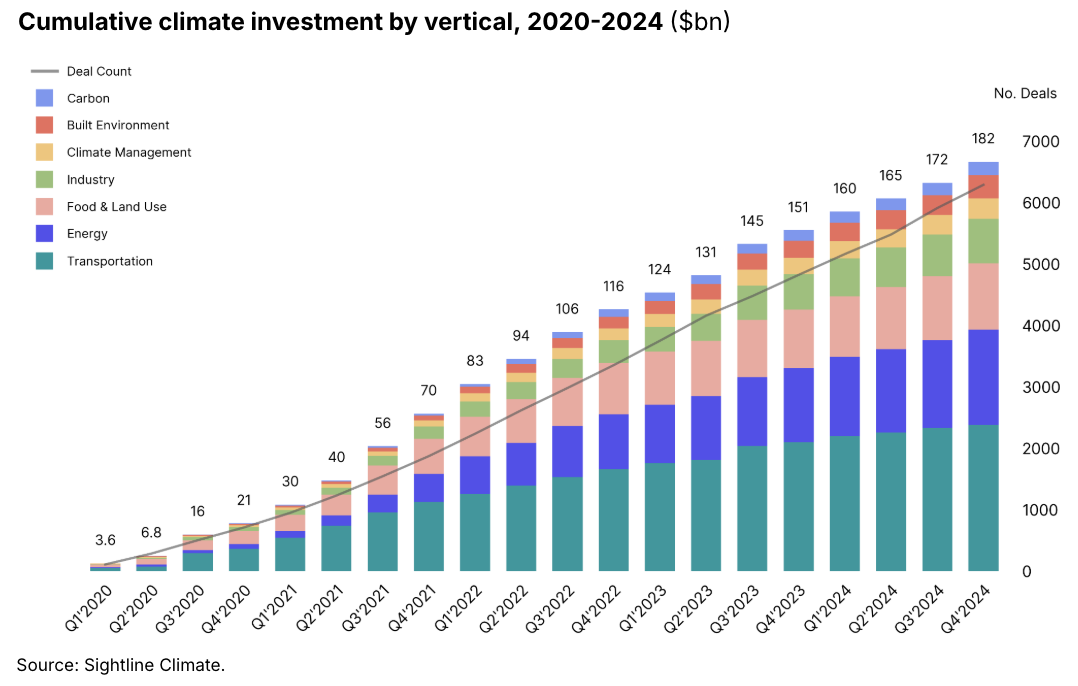

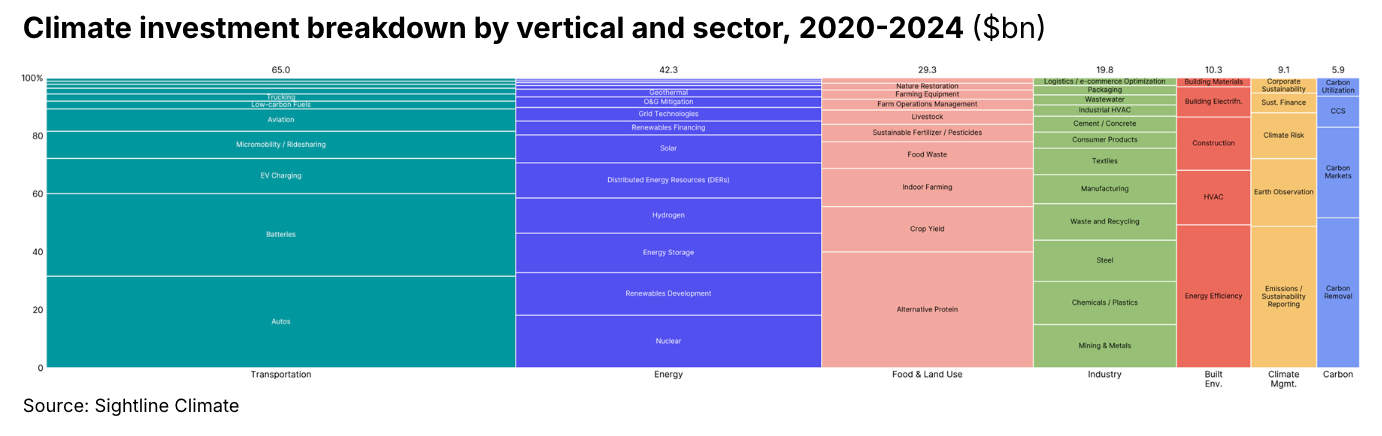

🚗 Vertical: Energy came out on top in 2024 investment, up 12% to $9.4bn. Transportation underperformed, down 36%. Industry was down 29%, returning it to fourth place behind Food & Land Use.

💤 Fewer repeat investors: There were 12% fewer investors overall in climate tech in 2024, with repeat investors rising to make up the majority. Sector tourists have left for other pastures as climate-focused funds topped the charts for deals in every investment stage.

🎉 Cumulative: Since the start of 2020, ~3,900 climate tech companies have raised $182bn+ of venture funding across over 6,200 deals.

A note on methodology: This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of December 31, 2024. Read more about methodology and definitions at the bottom of this post.

This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of December 31, 2024. We also verified deals directly with the most active investors. Where other market observers may promote larger climate market sizes, we stay true to our Climate Tech VC name and carefully exclude:

We’ve long held that climate tech is a theme not an industry. Our definition of climate tech comes with two filters: 1) climate impact and 2) climate vertical. Companies must tick the box in at least one category for both filters in order to make the cut.

To be counted as climate tech, companies must fulfill one or more of the following “climate impacts”:

Mitigation - Directly decarbonize across key emissions sectors.

Examples: electricity & heat, ag & land use, industry, transportation, buildings

Adaptation - Adapt to a changing climate with new products and economic models.

Examples: New insurance products, producing food to use, geo-engineering

Monitoring - Gather information / data about emissions or climate risks and impacts to generate insights.

Example: Emissions and sustainability reporting, climate risk and intelligence

Removal - Remove existing emissions from the atmosphere

Examples: Carbon removal, nature-based solutions, reforestation

Regeneration - Enhance general environmental “positive externalities” and “do more good, not just less bad”

Examples: Regenerative ag enhances biodiversity & sequesters carbon

In addition to having climate impact, companies must fall into at least one of the seven broad climate verticals below. These verticals encompass 60+ sectors and 250+ technologies helping us mitigate, adapt, monitor, remove, and regenerate in our warmer and weirder world.

⚡ Energy - The electrons and fuel that power us

Sectors: new generation technologies (e.g., nuclear, solar, geothermal), energy storage, hydrogen and other low-carbon fuels, enabling renewables software, marketplace, and grid management platforms, DER and demand response tools, utility transmission and distribution services

🚗 Transportation - The movement of people and goods

Sectors: battery technologies, EV autos, EV charging and fleet management, electric micromobility and ridesharing, zero-emission planes, boats, and trains, urban public transport

🌾 Food & Land Use - The nutrients and resources that give us life

Sectors: alternative proteins, regenerative farming, vertical farming, sustainable fertilizer and animal feed, nature restoration and ecosystem services, remote sensing for crop yield optimization, autonomous farming equipment, water tech, and food waste reduction

🏭 Industry - The goods and raw materials we use every day

Sectors: low-carbon cement, chemical and plastics, steel, manufacturing, metals and mining, circular economy commerce, sustainable textiles and packaging, waste and recycling

☔ Climate Management - The data, intelligence, and risk associated with a changing climate

Sectors: emissions and sustainability reporting, earth observation through remote sensing, climate risk and intelligence platforms

🏠 Built Environment - The places we live and work

Sectors: sustainable building materials, low-carbon heating and cooling, prefab construction, energy efficiency, building electrification and energy optimization

💨 Carbon - The avoidance and removal of emitted carbon

Sectors: carbon offset marketplace and procurement platforms, carbon utilization, carbon removal and storage technologies, point-source CCS, verifiers and ratings enablers

NOTE: You may notice that some of our numbers are larger in this update than previous editions. We constantly update the dataset to have the most accurate data possible, including adding post-dated deals.

🎁 Now that’s a wrap on the TLDR! If you’ve got this far in the email and haven’t yet clicked, get the full report here.

Have a different take on what’s driving these trends? Or questions about our analysis? Drop us a note at [email protected] if you’re looking to dig deeper into the 2024 investment numbers.

A breakdown of China’s new FYP and what it means for the next decade of the energy transition

We asked, you answered, and experts weighed in on 2026

My visit to China's cleantech factories, labs, and HQs

Newsletter

Newsletter