🌎 IMO sets sail for net-zero #242

The International Maritime Organization's first carbon tax ships out

The AI company’s debut shows where the chips are falling

Happy Monday!

We’re rebranding as an AI newsletter — just kidding, happy (early) April Fools! But we are talking about AI again — this time, with a look at the fallout from the CoreWeave IPO and what it could mean for energy demand and clean firm power.

In deals, $122m for nuclear fusion, $50m for renewable energy and storage, and $29m for lab grown meat.

In other news, there’s a new LPO director, the DOE is still betting on SMRs, and China expands its carbon markets.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

This isn’t an AI newsletter, but when the lines between AI, climate tech, and energy demand blur — we boot up. Last week, CoreWeave, in one of the most anticipated AI-adjacent IPOs in recent memory, hit the market, to high hopes and even higher valuations. But a crash landing suggests the AI compute boom hype might be starting to cool, with broader implications across the energy world.

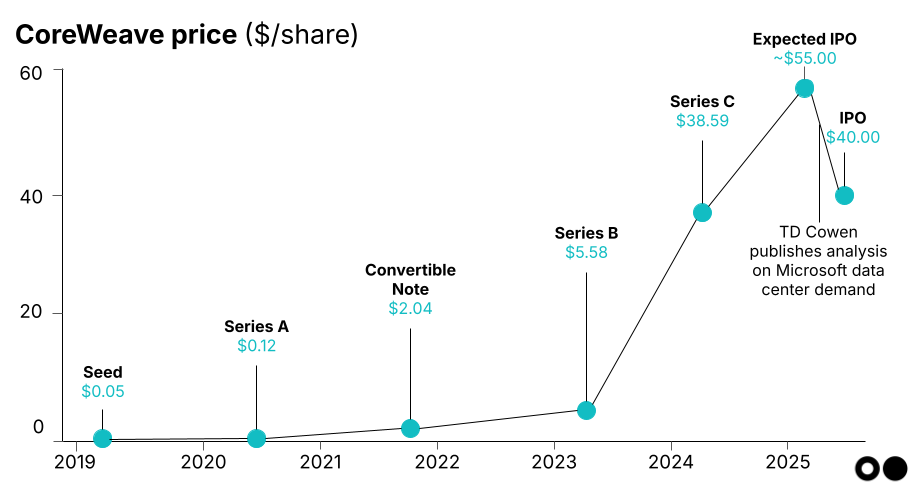

CoreWeave, a startup that operates data centers with high-powered NVIDIA chips tailored for AI workloads, went public on March 29. It was billed as the first in a wave of AI-linked IPOs — a signal that public markets were ready to bet on AI infrastructure.

CoreWeave’s business model is simple but capital-intensive: buy Nvidia chips, build data centers, and rent out cloud compute to AI customers. It works when demand for GPUs is sky-high, but it’s vulnerable to pricing pressure, high interest costs (the company holds ~$8bn in debt), weak demand for its servers, and eroding confidence in frontier AI’s long-term profitability. A drop in AI training costs or model demand could squeeze margins quickly (although skeptics argue Jevon’s paradox still means a rise in consumer use).

Meanwhile, cracks have been forming. Microsoft, CoreWeave’s largest customer, is reportedly scaling back its data center plans, canceling leases, and deferring capacity in the US and Europe. Plus, the release of DeepSeek, the Chinese AI model with radically lower training costs, rocked markets earlier this year.

Last week, the CoreWeave IPO faltered: The company raised only $1.5bn at $40/share — well below its $47–$55 target range — giving it a $20bn valuation. Even then, shares struggled to open, with investor appetite cooling fast. Behind the scenes, a last-minute $250m anchor order from Nvidia helped, but half the shares ended up in the hands of just three unnamed investors.

This IPO seems like a bellwether for AI infrastructure, raising questions about whether hyperscaler demand has been overblown and whether we’re heading into overbuild territory. Emerging trends like AI infrastructure expansion, along with ongoing shifts such as electrification and decarbonization, are driving new generation investment announcements. These include advanced orders for clean, firm power sources like advanced nuclear and geothermal, as well as new natural gas plants.

While these projects are still years away from coming online, they rely on the assumption of massive AI-related electricity demand from hyperscale data centers. Electricity demand surged 4.3% in 2024 (driven by industry, air conditioning, electrification, and data centers, according to IEA) and is expected to continue at a similar pace through the decade. However, these projections are variable, and investors — both in public markets and in energy projects — are unsure how to factor in all the moving parts.

For example, CoreWeave’s IPO shakeup was partly influenced by TD Cowen’s report on Microsoft’s pullback from new data center projects. Microsoft has paused plans for new data centers in the US and Europe — expected to add about 2GW of capacity — citing an oversupply of computing resources for AI (although Meta and Google bought some of those leases and capacity). One interpretation is that hyperscalers’ plans may not have changed as much as it seems; they may have always placed more bids than necessary to keep options open. If that’s the case, this adjustment doesn’t necessarily signal a shift in their overall strategies, but still, these signs of wavering demand will impact energy planning, especially with high interest rates persisting and geopolitical uncertainty. Already hesitant investors could become even more cautious.

Emerging clean firm power developers that rely on hyperscalers as key buyers may need to adapt, as more flexible, distributed energy resources could better align with fluctuating demand patterns. Geothermal and small modular reactors (SMRs), once viewed as long-term, firm power solutions, could face greater challenges if AI infrastructure demand slows or diversifies. It’s still early days, and everyone is waiting to see if today’s changes reflect future trends — if two things can be true at once: a) data center demand will be lower than some expected, and b) demand over the next 5-10 years can still drive significant adoption of emerging clean tech like SMRs and next-gen geothermal.

⚡ Marvel Fusion, a Munich, Germany-based fusion technology developer, raised $122m in Series B funding from Bayern Kapital, EQT Ventures, European Innovation Council, Siemens Energy Ventures, and Tenglemann Ventures.

⚡ XGS Energy, a Palo Alto, CA-based closed-loop geothermal developer, raised $13m in additional capital from Aligned Climate Capital, ClearSky, Climate Innovation Capital, WovenEarth Ventures, and existing investors.

✈️ TCab Tech, a Shanghai, China-based eVTOL developer, raised an undisclosed amount in Series B funding from Chi Fortune Venture Capital (Zifeng Capital) and Grand Neo Bay Venture Capital.

💨 Regrow Ag, a Durham, NH-based agriculture resilience platform, raised an undisclosed amount in Growth funding from SE Ventures.

🍎 Topanga, a Los Angeles, CA-based food-service waste reduction platform, raised $8m in Series A funding from Blue Bear Capital, Amasia, Struck Capital, and Wonder Ventures.

💨 ClimateCamp, an Antwerpen, Belgium-based supply chain emissions platform, raised $4m in Seed funding from Expon Capital, Birdhouse Ventures, Flanders Innovation and Entrepreneurship (VLAIO), KBC, and other investors.

🚗 Novac, a Modena, Italy-based supercapacitor for industrial energy storage developer solutions, raised $4m in Seed funding from CDP Venture Capital, Eureka! Venture, and Galaxia.

💨 ARK Capture Solutions, a Louvain-la-Neuve, Belgium-based industrial CO2 capture technology provider, raised $2m in Pre-Seed funding from Aperam Ventures, Seeder Fund, BeAngels, Climate Club, Invest.BW, and other investors.

🥩 Differential Bio, a Munich, Germany-based AI-driven bioprocess optimization platform, raised $2m in Pre-Seed funding from Ananda Impact Ventures, ReGen Ventures, Better Ventures, CDTM Venture Fund (Center for Digital Technology & Management), Carbon13, and other investors.

🔋Octet Scientific, a Cleveland, OH-based specialty chemicals for non-lithium batteries manufacturer, raised $2m in Seed funding from ICIG Ventures and BOLD Ventures.

☔ Maiven, a London, UK-based AI-driven climate policy platform, raised $2m in Pre-Seed funding from Ada Ventures and Pale Blue Dot.

⚡ AmpIn Energy Transition, a New Delhi, India-based renewable energy and storage service provider, raised $50m in Corporate Strategic funding from Siemens Financial Services.

🥩 Aleph Farms, a Reẖovot, Israel-based lab grown meat developer, raised $29m in convertible note funding from Cargill, DisruptAD, and L Catterton.

🌾 Grow Indigo, a Mumbai, India-based sustainable agriculture input platform, raised $10m in Corporate Strategic funding from British International Investment.

⚡ Safegrid, a Helsinki, Finland-based grid fault detection and sensing technology provider, raised $9m in Corporate Strategic funding from G&W Electric.

🚆 Viggo, a Copenhagen, Denmark-based e-bike rental service provider, was acquired by Bolt.

🌾 Plenty, a South San Francisco, CA-based vertical farming provider, filed for Bankruptcy / Out of Business.

⚡ Terrestrial Energy, a Charlotte, NC-based advanced nuclear reactor developer, announced a SPAC merger at an implied valuation of $280m.

🍎 Shelf Engine, a Seattle, WA-based demand forecasting platform, was acquired by Crisp for an undisclosed amount.

EQT, a Stockholm Sweden-based investment firm, closed its $23.2bn EQT Infrastructure VI fund, backing digital infrastructure and assets focused on energy generation, storage, and distribution.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate.

President Trump appointed Lane Genatowski, former ARPA-E director, to lead the Department of Energy's Loan Programs Office (LPO). During Trump's first term, Genatowski expanded ARPA-E’s focus to include nuclear fusion and carbon management. He will now oversee the deployment of the LPO’s $400bn in energy and manufacturing loans amidst ongoing funding freezes and legal confusion at the agency.

Meanwhile, the DOE reopened applications for $900m in funding for small modular reactors (SMRs), but removed the requirement for community selection criteria. This could have broader implications for grant-making and project investment if communities' needs are not adequately considered, though it aligns with the Trump administration's bet on nuclear energy as a solution to rising electricity demand.

China is expanding its carbon market to include steel, aluminum, and cement in 2025, adding about 1,500 firms and covering 60% of the country’s emissions. However, these industries will receive uncapped free allowances until 2027, delaying stricter emissions limits. While the move broadens market coverage, the softer caps raise concerns about near-term climate impact.

Hyundai announced it will invest $21bn in the US through 2030 to ramp up EV production and advance hydrogen and battery technologies in anticipation of incoming tariffs. As part of this, the company plans to build a new steel plant in Louisiana, with electric arc furnaces instead of coal, to supply its EV factories in Alabama and Georgia. This shift toward low-carbon steel production signals tailwinds for domestic clean(er) manufacturing.

The European Commission has selected 47 strategic projects across 13 EU member states to strengthen Europe’s critical raw material supply chain. To accelerate implementation, the permit-granting process will be limited to 27 months, significantly reducing delays. These projects, spanning mining, processing, and recycling, aim to reduce reliance on external sources and support its clean industrial transition plan.

In 2024, global renewable energy capacity increased by 15.1%, marking the largest annual expansion to date. However, this growth falls short of the 16.6% annual increase needed to meet the COP28 goal of tripling capacity by 2030. China led this expansion, accounting for nearly 64% of the global increase, adding more than eight times the capacity of the U.S. and five times that of Europe.

Enhanced rock weathering startup Eion secured $33m in purchase agreements. As other carbon removal methods, outside of direct air capture (DAC), gain traction, buyers appear more interested in credits from these alternative approaches due to lower prices for carbon offsetting.

This humid city in India stays chill with minimal AC — a cool approach to climate adaptation.

Tesla's BEV market share in Europe has plummeted over 50% due to rising competition and Musk’s political charge

A new paper that captures the science behind direct air capture.

European investors are finding renewed interest in climate tech, with startups weathering political shifts in net-zero targets (featuring Sightline data).

This longread with everything you need to know about the transformer, the device powering everything electrical.

Startups that once charged toward climate solutions are now jetting off toward defense and AI.

Meet the scientists racing to keep quickly disappearing government science data in the spotlight.

Invertebrate of the year winner: this colorful cuttlefish.

💡 VINE Connect: Apply by April 3 to join VINE Connect, a program linking food and agriculture startups with California farmers to demonstrate new technologies in the field. Selected startups will participate in a workshop series, a Field Demo Day on June 26.

💡 SPARK Cleantech Accelerator Cohort 4: Apply by April 15 to join the SPARK Cleantech Accelerator's fourth cohort, a 12-week program supporting early-stage cleantech startups with mentorship, funding opportunities, and access to prototyping facilities.

📅 ClimateTech Connect: Register to attend ClimateTech Connect on April 15–16 in Washington, D.C., a premier global conference and trade show focusing on climate resilience and technological innovation.

📅 San Francisco Climate Week 2025 Events: Explore and RSVP to various events happening between April 21–27 during San Francisco Climate Week 2025, bringing together climate leaders, innovators, and advocates.

Will you be at SFCW? We’re making a tracker to help CTVC readers navigate the event. Submit your event here and we’ll publish our tracker next week.

Senior Account Executive, Senior ML Software Engineer, Research Associate - Grid, Senior SWE, Research Associate - Generalist, Summer Research Intern @Sightline Climate

Software Engineer @Arch

Founding SWE @Jane Energy

Product Manager @Verse

Strategic Finance Manager @Lunar Energy

Full Stack Founding Engineer @Fram Energy

Investment Analyst/ Senior Investment Analyst @Angeleno Group

Investment Associate @First Time Fund – Sustainability Focus

Senior Full Stack Engineer @Coral

Continuity Fund Analyst @Congruent Ventures

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

The International Maritime Organization's first carbon tax ships out

Trump’s coal push ignores economic reality and attractive alternatives

The tariffs' toll, explained sector-by-sector

Newsletter

Newsletter