🌎 Q1 2025 roundup: top deals, exits, and new funds

Investors hope to set off a chain reaction with new nuclear funding

We’re getting close to the finish line of New York Climate Week, the marathon climate-focused conference week that feels like a sprint. From policymakers to investors, startup founders to corporate sustainability teams, thousands of people rushed around New York this week — oftentimes, literally racing from neighborhood to neighborhood for back-to-back events.

Since its inception in 2009, Climate Week has grown up with the climate tech industry, from being a policy-centered offshoot of the UN General Assembly to an independent “unconference” climate epicenter. Since the UNGA also occurs in the final week of September, security is high, but the climate community’s energy is higher. Innovators, funders, customers, and policymakers convene to collaborate, challenge, and celebrate across party lines. Founders showed sci-fi-like tech at demo days, while artists premiered climate-focused films at New York City's first climate film festival. Grassroots activists marched the streets and interrupted events to protest the presence of fossil fuel interests. Much like New York, it’s impossible to see everything in one week — but our team was on the ground, and we’ve got all of the highlights for you to help fight the FOMO.

And of course, climate tech took center stage (not that we’re biased). The sheer volume of companies in the space is incredible — even overwhelming. But as the cohort that launched in the last half-decade matures, the focus for founders and funders has shifted to making the economics pencil out.

NYCW ‘24 top line

NYCW ‘24 bottom line

The world looks a lot different than it did 15 years ago when New York Climate Week first started — and in many ways, worse. Scientists said this summer that the planet surpassed 1.5 degrees C of warming for the prior 12 consecutive months, making the need for action even more urgent and necessary. And while this year's NYC Climate Week featured the largest crowd with the most diversity we’ve seen to date, there was still a noticeable lack of non-white and non-American representation in some rooms, despite the fact that the Global South disproportionately experiencing climate change’s impacts today.

There’s no silver bullet of climate leadership or climate tech that will solve climate change. Passion and innovation are no longer the top priorities, as we put the pedal to the metal and focus on accelerating deployment.

We’ve been beating the drum about this, but the gap between Series B and C is growing wider, as late-stage and growth investment and deals have dropped off. It’s not about tech innovation anymore — it’s all about business model innovation, and companies that have believable, investable unit economic stories to fill the “missing middle” investment gap amid market uncertainty.

While growth investors are holding on to record levels of dry powder, they're hesitant to be the first ones to back something new (although once one is on board, others often follow quickly). It’s not news that exits are lagging, but investors are growing more impatient. Everyone is crowding the table, hungry for exits. The risk is if they don’t get fed, folks will go home (from the market) en masse.

When no one wants to take on the risk, companies are having to get more creative to access financing. Catalytic capital, venture and project debt, and even credit facilities are starting to cover parts of the so-called Valley of Death.

This week, venture investors were laser-focused on connecting with later-stage investors to bridge the messy, missing middle or Series B gap for their portfolio companies. Rather than networking with VCs at the same or earlier stages, they were eager to engage with growth funds, strategics, and even pension or sovereign wealth funds to help scale promising startups. The shift in the climate investor community was clear, represented by NYCW participants — there's growing attention on mid-market, private equity, and infrastructure investors rather than just early-stage VC.

What we heard:

Simply put, there’s no financing without offtake, and often no offtake without financing. For startups, demand for their products has to be there — and proven via long-term structured offtake. Offtake unlocks finance because it proves that the tech works (or at least, is commercially de-risked), and that customer revenue can repay investors. Project financiers and lenders will only take calls from startups that have secured this type of offtake.

Of course, different markets require different approaches: Europe is more sticks, so the policy incentivizes procurement of low-carbon goods — customers might be more willing to accept a green premium rather than pay a carbon tax. Meanwhile, America is more carrots, so market development has to start earlier.

Buyers alliances and pooled offtake are emerging as green market makers, coming in and acting as intermediaries between the buyer and seller and helping take on some of the green premium. There’s SABA for aviation, ZEMBA for maritime shipping, and a new buyers alliance for trucking.

What we heard:

On the flip side, corporates are quietly pulling back from their sustainability goals with climate, impact, and ESG taking a backseat as AI and other trends gain priority. The result is less demand and willingness to pay for SAFs, carbon credits, and other low-carbon commodities — making offtake hard, and securing financing even harder, as mentioned above.

This pullback has hit carbon markets particularly hard. Conversations on the voluntary carbon markets touched on this impact, exploring how to ensure that durability and quality remain king, even with demand waning. In the realm of carbon removal, tools like grants and price guarantees are helping bolster the capital stack, but insurance can play a bigger role in covering the risks associated with these technologies and projects.

In the meantime, government could play a bigger role. The DOE hosted several of its Deploy Dialogues and workshops to try and go a lot deeper into the tipping points that can scale these sectors, with lots of solution-izing about offtake and the role government should be playing on procurement, as it could serve as a largest buyer for low-carbon materials like cement and steel. Plus, clarifying regulatory uncertainties could provide market signals in spaces like SAFs, which is reliant on subsidies at different levels, both for the feedstocks and the final product.

What we heard:

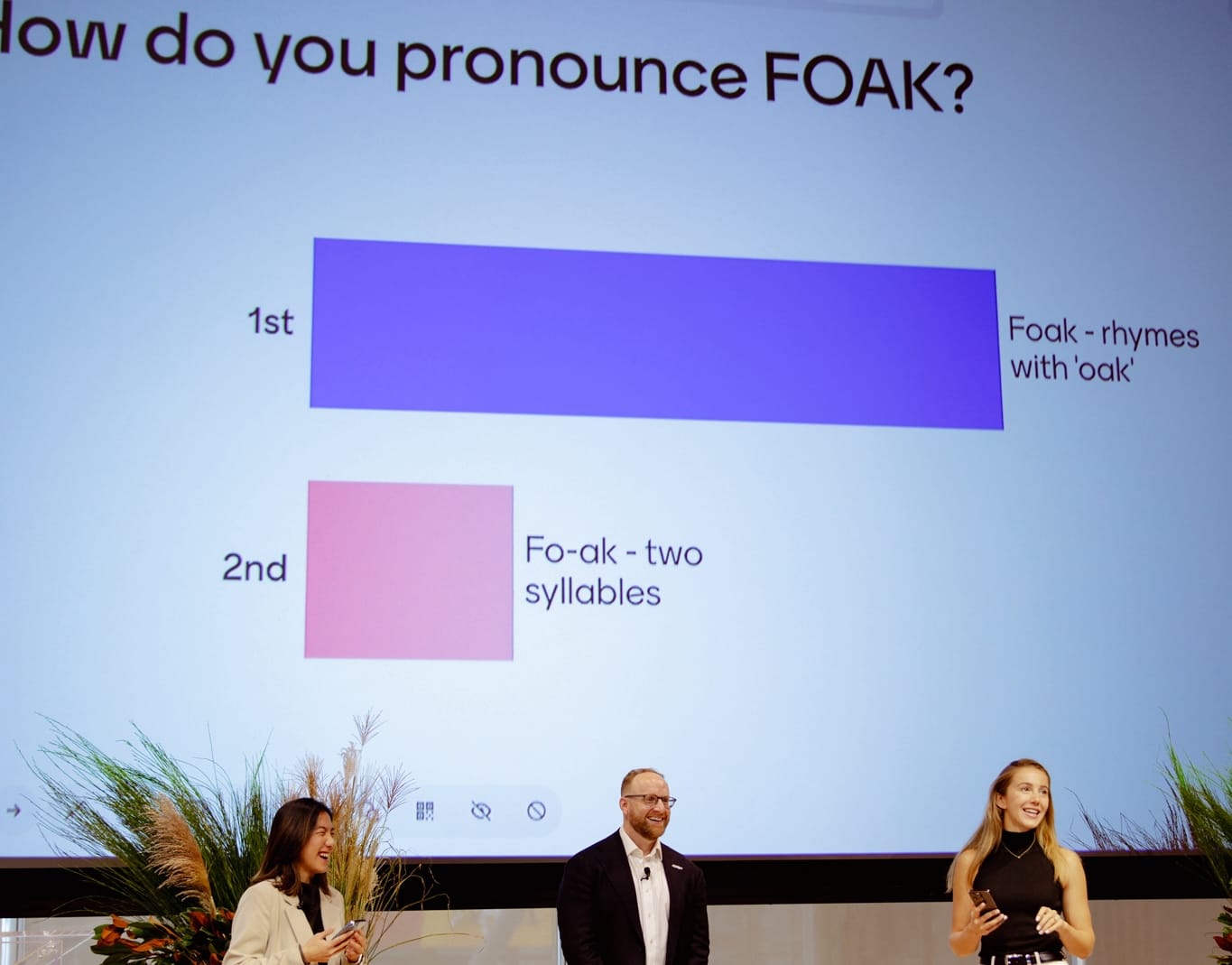

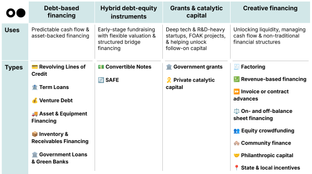

For hardtech companies building first-of-a-kind (FOAK) projects and demos, raising the right level of capital is critical — and it's no longer just about venture capital. Growth investors, private equity, and infrastructure players are increasingly trying to navigate the climate transition space, especially those who raised climate-dedicated funds in recent years. However, many of these later-stage institutional investors struggle to engage with climate tech opportunities, preferring more traditional “PE-style” assets — like minimum EBITDA/revenue thresholds, no tech or engineering risk, and asset-light service models.

A blended climate capital smoothie is needed, as mentioned above, possibly using catalytic capital or family offices as first-loss capital, layering in government grants and loans, and seeking strategic partners to fund projects in exchange for prepaid offtake deals — especially as a hedge against rising carbon prices. Yet, despite these strategies, there are still no clear pathways to capital for FOAK projects. Bridge financing, which was common in the early days of renewables, is now regaining traction as a tool to support companies through construction. While it's expensive, it can be refinanced at lower rates once projects are completed or near completion, making it a viable, though underutilized, option for climate tech firms approaching FOAK milestones.

The investors that do come in often look more like partners, helping enable everything from quicker permitting to banking to access to EPC firms (which are often in short supply).

FOAKs often look to corporate partnerships in various forms — from offtake to JVs to credit underwriting to strategic partnership agreements. The most successful startups are drinking Topco and project cocktails. For instance, corporate investors can help startups out investing debt or equity, sure, but also by signing offtake agreements, providing project support, and more. Later-stage investors can do this too by investing in the company and the project, as we saw with TPG and Twelve, and help set up channel partnerships in new markets. Advice for startups here? “Engage early,” as these relationships often take the better part of a decade to come to fruition.

What we heard:

Headlines shout about how energy demand is rapidly increasing, thanks to AI and electrification. But several panelists at NYCW advised a level of caution around the most fear-mongering upper-end estimates, saying that data center demand growth isn't as firm as it seems given factors like efficiency increases in AI and data center infrastructure. Regardless, energy demand is increasing, and will continue to do so — but the question is, how much? Utilities with long asset timelines are unsure of how to respond, especially given the increasing sources of energy coming online. The grid isn’t ready for these changes, but grid planning is increasingly difficult.

Opportunities like reconductoring and enhancing transmission systems came up as talking points throughout the week, along with a growing recognition that critical mineral security is energy security. Behind-the-meter solutions have fallen out of favor. Additionally, folks were bullish that innovative technologies such as small conduit hydro, advanced geothermal, and advanced nuclear are poised for deployment.

Meanwhile, generation and storage developers discussed how the scale of energy projects has evolved — that data centers are planning bigger facilities, with more flexibility to locate around clean energy sources with better grid transmission. But as these projects grow, transmission infrastructure and critical mineral supply chains must evolve alongside them.

What we heard:

What was your favorite moment or biggest takeaway from NY Climate Week? Whether you were on the ground this year or catching recaps from home, let us know what you most appreciated and which questions are still lingering as the week comes to a close. Drop us a note at [email protected].

Investors hope to set off a chain reaction with new nuclear funding

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

What’s actually working while the rest of the climate capital stack stutters