🌎 Meet the FOAK folks

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

Few climate tech founders have much scar tissue from Cleantech 1.0. From those that do, the refrains of technical substance first, smart capital, and pure dogged survival through the Valleys of Death ring true as a mix of caution and inspiration to their fast followers. In this Q&A with Rob Hanson of Monolith, we go deep on situating Monolith within the context of cleantech cycles, lessons learned and hard choices made (both forced and fortunate) that have helped the company close a Tesla-sized $1B loan from the DOE Loan Programs Office in pursuit of the massive markets of clean hydrogen and clean carbon black.

Monolith has been at this for a while! Tell us about the journey to Lincoln, Nebraska!

Back in 2012, my co-founder Pete Johnson and I were coming off a successful solar thermal startup, Ausra, now Areva Solar. At Ausra, we built linear fresnel tech which concentrates solar heat onto an overhead receiver to boil water and generate steam for industrial processes or electricity. Solar thermal ultimately lost to solar PV, but at the time it was a real race.

That experience was formative as Pete and I thought about our next company. We wanted to build something impactful for the energy transition, but function on a standalone economics basis without relying on Investment Tax Credits (ITCs) or grants.

We’ve always envisioned a world in which solar and wind gets down to $10/ mwh. The idea has been to build out an infinite number of renewables, batteries, and electrify everything - and be done with the energy transition. But in reality, wind and solar prices are going back up. The technology curves are largely done, so the last five years have been about cost of capital and financing. Now raw material costs and interest rates are rising, and the best sites have already been taken.

Unfortunately, this means the energy transition will be harder than we originally thought. But from an entrepreneurial perspective, it’s also an opportunity for companies who have the standalone economics to make it through tougher economic cycles.

How did this realization lead you to hydrogen?

We went from looking at solar and wind to the other half of decarbonization - long duration energy storage, heavy transport, etc. We eventually landed on hydrogen. This was back when most people talking about hydrogen were viewed as a bit crazy. Now everyone’s like “oh of course hydrogen,” but back then you said it quietly. You didn’t want to raise red flags that investors would run away from.

But we knew hydrogen was going to play a role, because there’s a massive hydrogen market that already exists to make the world’s ammonia and feed billions of people. The lightbulb moment happened for us with a process called methane pyrolysis. Methane pyrolysis uses clean electricity to heat up natural gas (which is primarily methane) to split it into hydrogen and solid carbon. So you output clean hydrogen and carbon as two high value products. The carbon can actually be used, so you get standalone best-in-class economics.

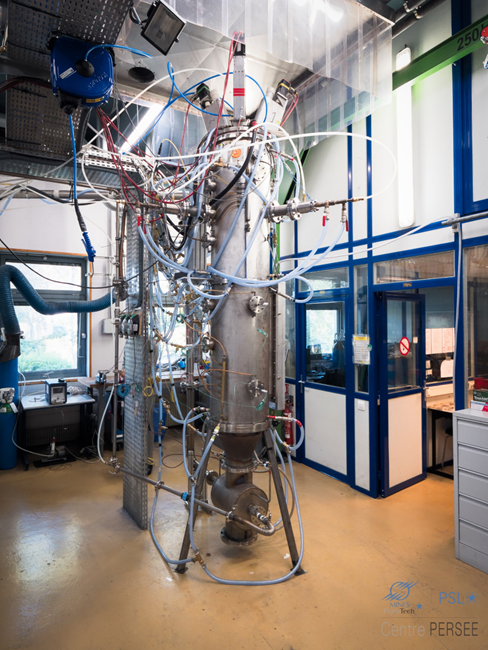

We found Professor Laurent Fulcheri at Mines ParisTech who had been working on this tech for 30 years. He had a pilot plant in France that not only could split methane into hydrogen and carbon, but actually produce carbon black which goes into everything from tires to inks to cosmetics. Carbon black is ubiquitous. That was the key discovery we’d spent a year looking for. We went from a concept on paper to finding a pilot plant that worked at a reasonable scale. From there, we built the company to deploy this technology.

What got you excited about methane pyrolysis compared to alternative hydrogen production methods?

Right now, most of the world’s hydrogen is made through a process called steam methane reforming, where you combine steam and either methane or natural gas at high temperatures. This process is cost effective, but you make 11 tons of CO2 for every ton of hydrogen produced, so it’s not clean.

Then there's the “academic” clean hydrogen pathway, electrolysis, where you split water with electricity. The challenge in this case is that water is at a zero state, and to liberate the hydrogen takes huge amounts of electricity. You get clean, but expensive, hydrogen which doesn't work for Monolith’s thesis.

We finally came across methane pyrolysis, which has two attractive factors. First, you’re splitting methane instead of water. It takes 7x less electricity to split methane than it does to split water. So while electrolysis can get more efficient, from a fundamental physics perspective it will never be as efficient as methane pyrolysis. Secondly, we can simultaneously produce carbon black which has a huge existing market worth over $1,000/ ton. We can make two products with less energy than electrolysis, which means we get this incredible economic boost from the start.

You make this sound easy, but Monolith’s success has been a decade in the making. What critical challenges have you had to overcome to get to scale?

All this sounds simple, but it's incredibly complicated. We've now built the world's largest plasma torch using an electric arc to heat the reactor. Outside of fusion, we may have the highest temperature reactor on the planet. There’s a ton of cool physics, material science, and electrical engineering that goes into this - enabling magnetohydrodynamic modeling, magnetic fields, even plasma control. Carbon black sounds like this boring, speciality chemical that goes into tires, but just one car tire can have 10 different grades of carbon black each with different nanostructures. These properties can influence the tire’s resistance, toughness, and shock absorption. So we’ve really got to nail the science behind carbon black, considering it’s a safety product.

Lastly, the physical infrastructure required to make all this happen is massive. At our current scale, our reactors are 100 ft tall, 14 ft in diameter, and equipped with complex operating structures. We’ve had physics and chemistry PhDs making fundamental scientific discoveries simultaneously working alongside 24/7 shift operations keeping this giant plant running nonstop. The impact comes from both the nitty gritty chemistry but also getting the logistical and operational side to work.

What are the greatest challenges when it comes to talent and team building for such a large, technical business? What does it mean to hire and staff up a 100 ft reactor?

From the beginning, we recognized we absolutely needed to recruit – and retain – a core of the company that's incredibly technically sophisticated. We hired the standard starting technical team: engineers across different fields, scientists, Masters and PhDs, the best possible talent that can work together to solve hard problems.

As we’ve scaled commercially, we’ve needed to build the rest of our workforce. That means 24/7 shift operations to run the plants in rural Nebraska but also a sales and marketing team to actually get these products to end markets. As we pursued more sophisticated financings, including a billion dollar loan guarantee from the US Department of energy (DOE), we've also had to grow our finance team to include professionals who understand those complexities.

What does the business look like today? How do you serve customers across both carbon black and hydrogen?

We produce and sell both carbon black and hydrogen. Carbon black is straightforward because it's a huge existing market for tires and inks. We also have the advantage that our carbon black is clean - whereas conventional production requires partially burning a heavy oil resulting in 2.3 tons of CO2 for every ton of carbon black, on top of SOx, NOx, mercury and other emissions.

On the other hand, hydrogen has both existing and emerging markets. The existing market is why we’re in Nebraska, since most hydrogen today is used to make the ammonia in nitrogen-based fertilizers. Russia had been supplying 20% of the world's ammonia, but ceased due to the war in Ukraine. Prices have now gone through the roof, driving food inflation and impacting people around the world. So there are also important implications here for agriculture and equity.

Our potential in emerging markets lies in hydrogen’s growth opportunities - clean steel or synthetic liquid fuels for heavy transportation. We’re watching these end applications, but at the end of the day, it’s going to come down to carbon and cost. As those markets emerge, we’ll be ready to serve them with clean, cost-effective hydrogen.

Monolith is the marquee example of raising from the full “climate capital stack”. Walk us through the key phases of growth and inflection points.

This little French proof of concept pilot plant is where it all started in 2012, producing 1 kg H2/ hour. We took the private equity route and raised our first round of financing co-led by Warburg Pincus and Azimuth Capital. They funded the first five years of the business up front, which is how long it would take to scale the business up to the next inflection point.

In 2014, we built our demonstration plant in Redwood City, California with 24/7 operations producing 10kg H2/ hour. After solving the production type run and making tens of tons of materials that passed quality control, we proved the unit economics at relative scale. The demonstration plant was an awkward size, commercially unviable due to heat loss and other inefficiencies, but made our point. At the end of this, we’d gone through our first $70m of capital. We then raised our Series B, adding another private equity group called Cornell Capital. That capital got us through the following 3-4 years to scale this up 60x to our first commercial plant.

This is what the commercial plant looks like now. That middle part is the main reactor and you can actually see the corn growing in the background - which makes it kind of obvious why you want to make ammonia at a location like this. Once construction ended, we had additional strategic financing from NextEra, SK, and Mitsubishi.

Overall, Phase One was pilot to demo and Phase Two was demo to a commercial scale unit, which we're now at the tailend of. Our technology works, it's ramped up, and products are being sold successfully. Now, we’re in our growth round, ready to get to the next stage building commercial plants with multiple reactors, not just individual units.

We're going to build 12 units next to each other, basically 12x our current commercial plant. We’re past tech risk into execution, EPC, and construction risk. This is a >$1B capital project, which means we're planning to raise more project equity in the second half of this year.

Looking forward, we've got 40 plants in development around the world. Our partnerships with NextEra, SK, and Mitsubishi - and other non-public partners - enable us to expand to countries like South Korea and Japan.

Why raise private equity in the early days? How have you thought about the type of capital you’re raising?

For us, it was by necessity. We started Monolith in 2012 when no one was writing checks. Climate venture had been a huge thing from 2005 to 2009 but it all went away after the Cleantech 1.0 bust. When we were getting this idea together, most investors flat out rejected us for being too capital and time-intensive. But we knew we had a good business, and energy and climate couldn’t care less about the fickleness of specific financial markets.

We kept looking and found people who would write checks, which happened to be the PE energy folks. They were traditionally doing non-climate, big energy projects, and became early movers in putting capital towards the energy transition. They invested in us for the climate aspect, but their DNA was more in unit economics and IRR. While Silicon Valley startups typically need only a bit of traction to get venture valuations, our investors made sure that our business was sound from the beginning. Our PE funding came by necessity, but we’re fortunate that we ended up with our original shareholders.

Now you’re setting another precedent by bringing another type of financing into the climate capital stack. Walk us through the DOE LPO process that resulted in Monolith’s conditional approval for a $1B loan.

I came into the workforce in 2007 during the cleantech boom and saw firsthand what the Loan Programs Office (LPO) is capable of. My colleagues were at companies like Tesla, which essentially got launched by the DOE loan, or BrightSource, which had its solar Ivanpah Project outside of Las Vegas funded by a $1.6B DOE loan. Everyone remembers Solyndra, but I remember the success stories and how the DOE is supposed to work. I’ve always had a lot of respect for the program.

We actually applied to the DOE LPO under the Trump administration despite everyone around us thinking they’d kill the program. But we knew it’s a legit program, the dollars are accrued, and the Department of Energy is a big place. At the end of the day, they’re pragmatic, technical, and financial folks. So we got all the way through the three part DOE process:

We completed the eligibility and underwriting first and second parts under the Trump administration. Then after the election, when Jigar Shah was named the newest Director of the LPO, we were thrilled to have someone in the role with such a deep appreciation for innovation. In 2021, we moved into the final stage of diligence and finally into conditional commitment. Now we’re working through the fairly typical conditions like getting all of our permits to construct the plant, finalizing the EPC contract, and hitting operational metrics on our first unit. Once we check off all of the conditions, we’ll close the loan, go live, and start building the plant.

Where do you continue to see Valleys of Death in this capital stack? How did you specifically overcome them?

There have been two notably severe Valleys of Deaths for Monolith. Number one was getting the financing to build the first commercial unit once the demo plant worked. Getting through the demo isn’t that hard. Raising $40-50m for a pilot with a lot of promise is relatively easy. Raising $100-300m for a commercial unit, which doesn’t have great economics on its own, is much harder. It’s a relatively small plant, but still needs a full team to run it with the same safety considerations. It doesn’t benefit from economies of scale and yet still has a lot of the same risks. It’s a 60x scale up of really hard physics and chemistry to build the reactor.

We spent 2 years trying to raise that capital, first starting on our own to reach out to 100 people - who all said no. Then we brought in J.P. Morgan to help us and went out to another 100 investors. 99 said no, until we finally got 1 yes. It was 200 investors and 2 years. The only way through a Valley of Death is to keep walking forward, foot in front of foot, trying not to die. There’s no secret solution. Most will die and few will make it through.

So that’s the first Valley of Death where the scale of capital and risk is high. Funds writing $5-10m checks can write twenty checks where 5 fail and it’s expected. Funds underwriting $100m need a 100% success rate.

We just made it out of the second most challenging Valley of Death. Once the commercial plant is built and the technology is working, you need to make it work every single day, day in day out, for some of the most demanding customers in the world. Tesla went through this; Elon said that building a factory to build cars is materially harder than it is to build a car. Building the car is not the hard part. The hardest part is getting the whole system to work at six-sigma quality levels, with no safety or environmental incidents. A lot of companies are going to drop off at that stage, especially if they take an extra couple of years getting through it and don’t have the capital structure to allow it.

Is the market today different from a funding perspective than when Monolith was going through its first Valley of Death?

A large part of scaling a successful climate company is access to low cost capital. A large cohort of startups are about to enter the first Valley of Death at the same time, right as the cost of capital has gone up. Of course in any capital market, the most resilient, best performing businesses will survive. But it’s going to be a tough slog.

Our first challenging commercial-stage fundraise happened in 2018 and it took us around 18 months to raise. The market was entirely different. Transition investors like hedge funds and pension funds had been putting money into the market, and then all of a sudden there was a massive switch and the capital dried up overnight. The market today looks eerily similar. Let’s just say that it’s going to get hot in the Valley… in a dehydrating way!

You just raised $300m in growth from a stack of big-name growth funds including TPG Rise Climate, Decarbonization Partners, NextEra Energy Resources, SK, Mitsubishi Heavy Industries America, and Azimuth Capital Management. How did that round come together?

TPG and Decarbonization Partners are at-scale climate-dedicated PE funds, which signals that there’s structural and long-term capital coming into the market. LPs want exposure to the cohort that Monolith is in right now - companies that have made it through their first couple Valleys of Death and are now scaling their businesses.

These are dedicated climate pools of capital at scale, and groups that are incredibly rigorous. Their diligence this round was on par with the DOE’s and they got into the nitty gritty of the business. We were down to “who owns which fertilizer tank, how much of our ammonia is going into each tank, what happens in extreme weather scenarios” level of very nitty gritty supply chain diligence that we hadn’t been asked from earlier investors.

That’s exciting! Because we want not only the most amount of capital, but the smartest possible capital. Super smart, abundant capital is critical to scaling climate tech, so I’m thrilled that these types of investors are coming in.

Monolith is poised to remain a pillar of climate tech scale up done right, given it bridges the decades between climate tech investment and the pathway from lab to revenue. And they’re hiring across all areas of the business across all of their offices in the Bay Area, Denver, Kansas City, Lincoln and Hallam, Nebraska - as well as the South of France. Oh là là! As a veteran of the industry, Monolith is excited about the earlier pipeline of climate entrepreneurs and wants to connect with new Seed stage companies about partnership and potential licensing opportunities. Big thanks to our CTVC team and friends, Gabriela, Shreya, Ethan, and Brandon for their rock-steady support with producing this interview.

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

A Q&A with the DOE LPO director Jigar Shah and Solugen CEO Gaurab Chakrabarti

The White House’s new announcement clears the air about the voluntary carbon market