🌎 Meet the FOAK folks

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

Investors hope to set off a chain reaction with new nuclear funding

Happy end of Q1 🎉 With the first quarter of 2025 officially in the books, we’re sending out a (light) quarterly roundup, spotlighting some of the top hits of the quarter. We’ve got an early snapshot of the top deals, exits, and funds from the past three months. Of course, our regular half-year report will be out at the end of Q2 and will dive deeper into the investment totals, deal counts, sector-specific activity, and most active investors. But here’s what we’re seeing so far.

The quarter has been marked by fits and starts — Trump 2.0 has already brought about seismic shifts in the regulatory and funding landscape, creating a broad sense of uncertainty (don't worry, we'll be tackling the tariffs in our Monday newsletter). Still, the new normal that we saw materializing at the end of 2024 seems to be holding. The deals haven’t stopped — particularly in the power sector, where both generation and grid technologies continue to attract investor interest – but they’re bigger and fewer.

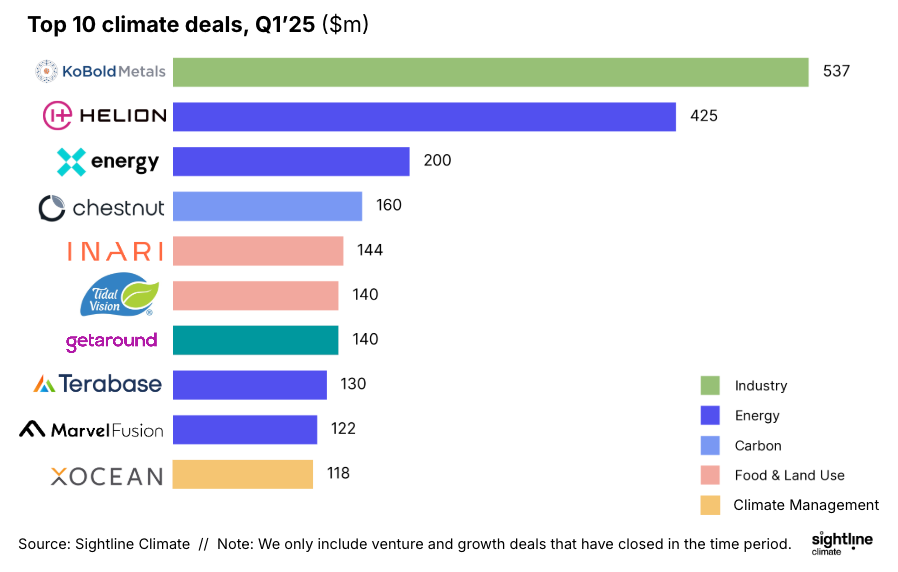

⚡ Energy led the top deals, nabbing four out of the top 10 biggest deals this quarter. Nuclear and fusion deals were three of those four. There was also an appetite for bigger biotech deals, and we saw a number of smaller grid-related deals.

💸 Average deal size remained healthy, especially for later-stage deals and especially in the energy sector. While there’s been a downtick in VC deal count compared to previous years, project finance deal count (and PF investment total) rose.

🤝 Acquisitions were the most common type of exits this quarter, with a number of strategic acquisitions by both startups and corporates, the majority with undisclosed terms. This is part of a broader trend where larger companies are using balance sheets and decreased valuations to scoop up valuable assets at a lower cost.

❌ Meanwhile, bankruptcies continued in sectors we saw declining last year, with notable companies like Northvolt (battery manufacturing) and Plenty (vertical farming) officially filing for bankruptcy.

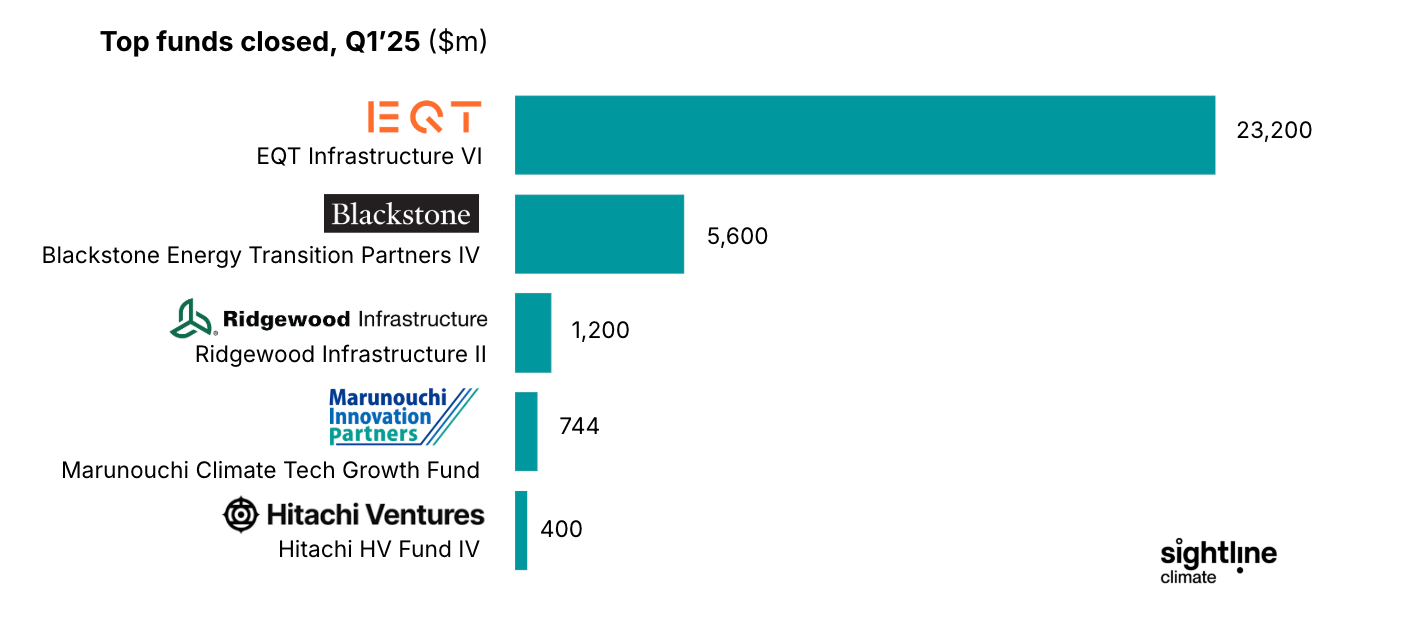

📈 Funds with climate remits closed this quarter for a total of more than $31bn. The biggest were infrastructure funds, now throwing their weight behind mature climate sectors. Mega-funds from EQT and Ridgewood Infrastructure are backing digital and sustainable infrastructure projects, and energy transition more broadly.

Interested in becoming a Sightline client?

Deep dive: X-energy's $200m follow-on round

Advanced nuclear reactor and fuel company X-energy closed $200m as a C-1 round, after a previous $500m Series C last year. The follow-on investment came from additional investors impressed by the backing from Amazon’s Climate Pledge Fund, Citadel, Ares Management Corporation, NGP, and the University of Michigan. This follows a trend we noticed in our 2024 Climate Tech Investment Trends report — there’s still money to spend, but everyone wants to spend it in one place.

The company has signed partnerships with AWS and Dow, helping to prove its commercial case, as it continues to make progress on permitting for sites. The capital X-energy raised will support reactor design work and licensing, as well as the first phase of its TRISO-X fuel fabrication facility in Oak Ridge, Tennessee. It plans to complete site prep at its TRISO-X fuel fabrication facility by this summer, aiming to begin vertical construction later this year.

“The growth of energy demands from AI has placed a premium on clean, affordable, and reliable power – an opportunity that X-energy’s technology is designed to meet,” Clay Sell, CEO of X-energy, told us.

Deep dive: Chestnut Carbon's $160m Series B

Another interesting deal was Chestnut Carbon, which raised a massive $160m Series B round. Founded in 2022 by PE firm Kimmeridge, the company focuses on purchasing marginal and degraded farmland in the Southeastern US, restoring it with native trees, and generating carbon credits. The round attracted backing from institutional investors like Canada Pension Plan Investment Board, DBL Partners, and Cloverlay, among others.

Still, Chestnut is navigating the challenges of the voluntary carbon market where credibility has been a major concern. To overcome this, the company focuses on owning land in the US, where robust property rights and clear ownership structures help ensure stability and boost credibility for its longer durability claims, under Gold Standard. It also works with third party land-owners to develop high quality removal IFM credits under Verra. Early on, it signed an offtake contract with Microsoft, structured like a Power Purchase Agreement (PPA), a contractual framework used in conventional assets that helps enable the space to mature and attract lower costs of capital. Microsoft also then signed a second, larger offtake contract soon after. The buyer’s creditworthiness signaled trust in Chestnut’s ability to deliver on its commitments, and helped attract investors who saw the potential for scaling the business and meeting demand for verified credits.

Looking ahead, Chestnut’s long-term goal is to lower the cost of capital, with plans to move beyond equity funding and into debt financing. This step will help reduce financing costs and increase the company’s ability to scale, but Chestnut is still focused on keeping the business model simple, a “rinse and repeat” project development approach with a focus on conservation for profit, to deliver risk-adjusted returns to investors and ensure the business itself is sustainable.

There’s a strong trend of consolidation and market maturation in these exits, with larger players securing strategic assets, while some smaller companies continue to face tough conditions in today’s competitive environment.

On the other hand, the not-so-great exits this quarter included a handful of high-profile bankruptcies, all facing execution challenges of different flavors. Among the most notable was Northvolt, the once-promising battery manufacturer, which filed for restructuring bankruptcy at the end of last year and ultimately folded this quarter. Now, Volvo is stepping in to take over its assets. Startups are struggling to compete with established incumbents which are better positioned to overcome the high capital and technological barriers required to scale. EV maker Nikola also went bankrupt, but it faced a whole other set of problems, such as financial fraud from the founder that resulted in jail time and recently, a presidential pardon.

Meanwhile, high-profile ag startups continue their tough times. Vertical farming startup Plenty shut down, after facing hefty upfront costs it couldn’t overcome. The sector’s infrastructure, like lighting and climate control, along with the energy required to run it, is expensive. Ynsect, a producer of insect-based protein primarily for animal feed, also filed for bankruptcy last month. Though well funded, it was unable to recover from the two-year delay in its mega-factory due to Covid-19, combined with mounting losses.

Despite today’s challenging fundraising environment, several major climate tech funds have closed, collectively raising a total of $31.9bn. Among the largest funds is EQT Infrastructure VI, which raised a staggering $23.2bn, followed by Blackstone Energy Transition Partners IV with $5.6bn. These substantial figures reflect a continued strong interest in energy transition and infrastructure, particularly in North America and Europe EQT’s fund surpassed its target raise, while Blackstone’s grew about a third since the predecessor fund, showing a strong appetite for climate infra funds. Ridgewood Infrastructure II and Marunouchi’s Climate Tech Growth Fund also made notable contributions, raising $1.2bn and $744m, respectively. These funds are particularly focused on large-scale, long-term projects aimed at advancing decarbonization and energy infrastructure. Several other funds announced this quarter also said they were targeting energy transition projects, including grid technologies and electrification.

Emerging markets have also arrived at the party, with funds like Equator focusing on early-stage investments across Africa in sectors like energy, agriculture, and mobility. There’s also a rising focus on tech-enabled solutions, particularly in sectors like AI, industrial technologies, and clean energy with funds like Hitachi HV Fund IV driving innovation in Asia. While vertical farming’s troubles may have put the dampers on the ag sector, nature-positive initiatives and sustainable food systems are gaining traction, with new funds such as LITA.co impact fund and Just Climate's Natural Climate Solutions fund focused on transforming land use with nature-based solutions and sustainable agriculture.

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

What’s actually working while the rest of the climate capital stack stutters

Announcing Sightline Climate's $5.5M Seed fundraise from Westly and Molten