🌎 New survey: How climate tech gets funded in 2026 #291

New founder survey from Sightline Climate × Elemental Impact

The Arkansas region has a motherlode of the critical mineral

Happy Monday! It’s officially spooky season, and the ghosts of critical minerals past are back again. This week, we’re digging into the news that Arkansas’ southwestern Smackover Formation region could be home to between 5 and 19 million tons of lithium.

In deals, $900m for pulsed magnetic inertial fusion, $100m for energy efficiency as a service, and $70m for AI precision weed control.

In other news, the eVTOL sector gets cleared for regulatory takeoff, the DOE announces billions for new grid projects, and the race to fusion heats up.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

Last week, a new report found that southwestern Arkansas’ Smackover Formation region could be home to between 5-19m tons of lithium — representing 35% and 136% of current estimated US lithium resources — drilling into one of the key challenges of the energy transition: critical mineral supply.

What happened

The porous and permeable limestone in Smackover has long been known for oil and bromine deposits, but only recently has industry begun to explore its lithium lode.

Notably, nearly a year ago, ExxonMobil unveiled its first-ever lithium mining operation in the Smackover Formation in Arkansas, marking its first major foray into lithium production. The O&G supermajor purchased 120,000 acres over Smackover in 2023, and started drilling its first well this year. It planned to blend its expertise in conventional O&G drilling methods to access lithium-rich saltwater, then use more nascent direct lithium extraction (DLE) technology to separate lithium from the saltwater and convert it onsite to battery-grade material. By 2030, it aims to produce 75,000 to 100,000 tons of Lithium Carbonate Equivalent (LCE), the refined product used in batteries, enough to power 1m EVs.

Now, we have more details on what’s possible. Scientists from the USGS and the state’s environmental agency used a combination of water testing and machine learning to quantify the amount of lithium present in brines there. Indeed, it’s a gold mine: there is enough dissolved lithium present in that region to replace US imports of lithium and more (the US imports over 25% of its lithium), researchers say.

The caveat is, these estimates are total resources available in Arkansas, not exploitable reserves. Whether the lithium is commercially or technically recoverable is up to the project developers to define. ExxonMobil is still “working on understanding that cost equation.”

Why it matters

Once Exxon's operations are in full swing, the largest US O&G major could also become one the largest lithium producers in the world — not a fundamental strategy swerve, as it’s still investing in the Permian Basin, but possibly a hedge against an uncertain future for clean energy incentives given the upcoming US presidential race, and a bet on EVs.

Lithium is a key part of EV batteries, and demand for it has tripled in the past 5 years. Existing lithium production pathways include:

But emerging production pathways, like DLE, promise significant benefits. By filtering out lithium ions from brine, DLE can minimize water and land use, increase recovery rates (from 40-60% to 70-90%), and unlock production from lower lithium content brines, e.g. oilfield and geothermal. While still early, DLE could be the catalyst for lithium’s “shale” moment.

And it’s a critical time for the critical mineral. Global EV adoption targets could drive demand for lithium up to 40x by 2040 compared to 2020, according to the IEA. Chinese players currently dominate the supply chain by either owning lithium mines at home and abroad, or by maintaining a stronghold over two-thirds of lithium processing. But the Biden administration has thrown its weight behind onshoring EV battery supply chains. It established the DOE’s Office of Manufacturing and Energy Supply Chains, as well as included several critical minerals-related tax credits in the Inflation Reduction Act. The EV tax credit, for instance, has strict requirements for vehicles to be eligible: a fraction of the value of the battery’s critical minerals — including lithium — must be extracted or processed in the US or in a US free-trade agreement partners (so excluding Chinese-controlled production).

The US currently has two lithium mines: Albermarle’s Silver Peak mine, which is active, and Ioneer’s Rhyolite Ridge in Nevada, which just received permitting last week. The rest of domestic lithium needs are met with waste tailings in Utah, or imports. This new resource estimate in Arkansas is a welcome signal: even on the low bound of 5MtLCE, Smackover could cover American and even global lithium demand multiple times over. The Arkansas resource also has the advantage of not overlapping with Indigenous land (for context, 90% of planned lithium mines elsewhere are within 10 miles of tribal lands).

Key takeaways

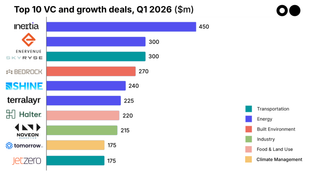

🏠 Redaptive, a San Francisco, CA-based energy efficiency-as-a-service provider, raised $100m in funding from the Canada Pension Plan Investment Board (CPP Investments).

🌾 Carbon Robotics, a Seattle, WA-based AI precision weed control platform, raised $70m in Series D funding from Anthos Capital, BOND, Fuse, Ignition Partners, NVentures, and other investors.

🚗 Outrider, a Golden, CO-based autonomous electric yard trucks developer, raised $62m in Series D funding from Koch Disruptive Technologies, New Enterprise Associates, 8VC, ARK Investment Management, B37 Ventures, and other investors.

🌾 Agrolend, a São Paulo, Brazil-based farm credit provider, raised $53m in Series C funding from Creation Investments, Syngenta Group, Barn Invest, Lightrock, Provence Capital, and other investors.

⚡ Urbint, a Queens, NY-based AI grid monitoring platform, raised $35m from S2G Ventures, Blue Bear Capital, Climate Investment, Energize Capital, National Grid Partners, and other investors.

🏭 Conflux Technology, a Waurn Ponds, Australia-based heat exchangers with additive manufacturer platform, raised $11m in Series B funding from Breakthrough Victoria, AM Ventures, and Acorn Capital.

⚡ Pacific Fusion, a Fremont, CA-based pulsed magnetic inertial fusion platform, raised $900m in Series A funding from General Catalyst, Breakthrough, Lowercarbon Capital, Lightspeed, Leitmotif, and other investors.

🏠 Oriole Networks, a London, UK-based data center optimization software platform, raised $32m in Series A funding from Plural, Clean Growth Fund, Dorilton Capital, UCL Technology Fund, and XTX Ventures.

✈️ Beyond Aero, a Toulouse, France-based hydrogen-electric aircraft manufacturer, raised $20M in Series A funding led by Giant Ventures and Bpifrance.

🏗 Dunia, a Berlin, Germany-based AI-driven materials discovery platform, raised $12m from Elaia, Redalpine, Anglo American, Deep Science Ventures, European Innovation Council (EIC) Accelerator, and other investors.

💨 Planetary, a Dartmouth, Canada-based carbon removal through ocean alkalinity enhancement service platform, raised $11m in Series A funding from Evok Innovations, Amplify Capital, BDC Capital, DNX Ventures, and ICONIQ Capital.

🚢 Carbon Ridge, a Los Angeles, CA-based onboard carbon capture technology developer, raised $10m in funding from Crosscut Ventures, Berge Bulk, Canopy Generation Funds, Grantham Foundation, Incite Ventures, and other investors.

⚡ Hydrogen Mem-Tech, a Trondheim, Norway-based hydrogen separation membrane provider, raised $7m in funding from AP Ventures.

🏠 Measurable.energy, a Reading, UK-based electricity-reducing plug sockets developer, raised $5m in additional Series A funding from Clean Growth Fund and Vertex Holdings.

✈️ Universal Fuel Technologies, a Los Altos, CA-based SAF & renewable chemicals producer, raised $3m in Seed funding from Alchemist Accelerator, Claire Technologies, TO VC, and World Star Aviation.

🔋 Anthro Energy, a San Jose, CA-based battery technology developer, raised $25m in Grant funding from the US Department of Energy (DOE).

🚗 BasiGo, a Nairobi, Kenya-based EV buses in Africa, raised $24m in Series A funding from Africa50, CFAO, Mobility 54, Moxxie Ventures, Novastar Ventures, and other investors and also raised $18m in Debt funding from British International Investment and US International Development Finance Corporation.

🔋 Moment Energy, a Surrey, Canada-based EV battery repurposing manufacturer, raised $20m in Grant funding from the US Department of Energy (DOE).

🧱 Furno Materials, a Palo Alto, CA-based retrofittable oxyfuel in cement plants producer, raised $20m in Grant funding from the US Department of Energy's Office of Manufacturing and Energy Supply Chains (MESC).

☀️ Lightsource bp, a London, UK-based solar power developer, was taken over by BP who bought up the remaining 50.03% stake.

💰 TPG, a New York, NY-based investment firm, raised $4.9bn in funding to invest across all climate tech verticals.

💰 CRH Ventures, a Madrid, Spain-based investment firm, launched an accelerator to invest in climate tech and construction startups.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate.

The Federal Aviation Administration announced regulatory approval for electric vertical takeoff and landing aircrafts (eVTOLs), as well as pilot training and operating rules. eVTOLs lift up and down touch like helicopters, but fly forward like typical airplanes. The approval is a huge step forward for eVTOL startups like Joby Aviation, which launched a $200m public offering in anticipation of a 2025 commercial eVTOL release, showing that eVTOLs might finally be ready for takeoff after a lot of turbulence.

In DOE funding news, the agency announced it’s channeling $2bn into transmission projects across 42 states, bolstering the power grid to withstand extreme weather while expanding renewable energy access. It also announced a $162m loan guarantee for LongPath Technologies to support methane emissions monitoring across oil and gas fields in major US basins, its first GHG-tracking loan. Plus, it’s investing $58m in 11 early-stage carbon removal projects as part of the Carbon Negative Shot initiative, targeting a CO2 removal cost of below $100 per metric ton by 2032.

In fusion news, three companies are making significant strides in the race to fusion. Zap Energy has revealed a breakthrough fusion prototype, aiming to simplify and scale fusion technology by using a "shear-flow" design. Tokamak Energy recently unveiled its first fusion energy pilot plant, further accelerating research into commercially viable fusion. Meanwhile, Marvel Fusion breaks ground on its new $150 million laser facility in a bid to commercialize fusion energy by generating an ongoing fusion reaction through its laser-driven technology.

In nuclear fission news, both Vietnam and the US are ramping up their nuclear strategies. The DOE is bolstering domestic production of high-assay low-enriched uranium (HALEU) through newly announced contracts, a move to support the deployment of advanced nuclear reactors and establish national supply for HALEU. Meanwhile, Vietnam is now amending its national power strategy, known as PDP8, to include nuclear as a reliable, low-carbon energy source, positioning itself for a more sustainable energy future. These developments reflect nuclear energy's expanding role in the clean energy transition.

In another win for geothermal energy, the Interior Department’s Bureau of Land Management gave final approval to Fervo Energy’s Cape Geothermal Power Project. This project, when fully operational, could generate up to 2GW of power and provide 24/7 energy that may be attractive to tech firms in need of stable energy sources for data centers. This signal shows that geothermal is maturing, as projects are successfully going through permitting.

Mixed signals in the hydrogen market, as Verdagy has launched a hydrogen electrolyzer gigafactory designed for large-scale hydrogen production, although the facility is not yet not fully operational. However, Neste canceled its planned investment in a 120 MW electrolyzer for renewable hydrogen production due to challenging market conditions and financial performance issues. These developments show both the growth potential and the ongoing challenges in scaling renewable hydrogen, crucial for energy transition in hard-to-abate sectors.

Hedge funds are ramping up short positions in clean tech stocks, betting on industry volatility amidst slower green energy growth and policy shifts. A Bloomberg analysis reveals that investments in companies tied to electric vehicles, renewables, and carbon capture are increasingly vulnerable to speculative trading, even as climate tech capital continues rising globally. This shift points to persistent market uncertainties around exits for climate tech companies.

Fruitful harvests lie ahead with the World Bank set to double agriculture funding to $9bn a year by 2030, amidst rising food demand and climate challenges.

Delegates cross-pollinated conservation ideas at the biodiversity COP last week in Colombia.

Tree in a bottle: Berkeley scientists claim to have designed a powder that can remove as much CO2 from the air as a tree can in a whole year.

The Clean Air Task Force analyzed Weighted Average Costs of Capital to attract investment in green energy projects across Africa.

The race to save rice – scientists in Japan are scrambling to crossbreed a heat-resistant DNA pattern into famous Koshihikari sushi rice.

A new supermarket staple? Pawpaw fruits thrive as other fruits wilt under rising temperatures.

Proof points: The Carbon Removal Alliance released a roadmap to improved carbon removal monitoring, reporting, and verification.

Hot new rock on the block. A Quaise permeability study in superhot geothermal systems supports their potential to be renewable energy game-changers.

Terraset purchased $3m of carbon removal – that’s over 5,000 tons of CO2!

SunCable receives approval for a PowerLink project to transmit solar energy from Australia to Asia via subsea cable.

Out without a bang. Astera released a guide to gracefully winding down deep tech ventures.

Ready to rumble. The final rule for the IRA’s Advanced Manufacturing Production Tax Credit is out, notably allowing critical mineral extraction to qualify for a 10% tax credit.

Gravity-based energy storage was not looking up, so Energy Vault transitioned away to 1GWh lithium batteries selling for $234m a piece.

📅 Mapping the Future of Biodiversity: RSVP to attend the Mapping the Future of Biodiversity livestream on October 31st, to discuss aligning planning and conservation with Biodiversity Net Gain (BNG) to support COP16’s global biodiversity targets.

📅 Non-Dilutive Finance for Climate Startups: Register to attend the Non-Dilutive Finance for Climate Startups workshop on November 7th for founders and investors to learn more about the non-dilutive financing landscape, examine case studies of transactions, and open Q&A.

📅 Out in Climate Fireside Chat: Register to join the Out in Climate fireside chat on November 13th to hear from NYC Climate Government Leaders Elijah Hutchinson and Louise Yeung.

📅 Harbor Climate Collaborative: RSVP for the Harbor Climate Collaborative via email to attend an evening of NYC-based climate tech showcases on November 18th, including remarks by First Deputy Mayor Torres-Springer and Dr. Michael Oppenheimer of Princeton University.

💡 Scale For ClimateTech: Apply for the opportunity to join the 6th cohort of Scale for Climate Tech by November 30th and receive support ranging from manufacturing assistance to access to a vetted supplier network and help in commercializing your hardware product.

Product Manager, Research Analyst, Enterprise Customer Success Manager @Sightline Climate

Business Development Executive, Senior Associate, Business Development, Full Stack Engineer, Enterprise Marketing and Strategy, Analyst / Associate, Finance and Transactions @Reunion

Associate, Operations Manager @Aiga Capital Partners

Full-Time Venture Capital Analyst @G2 Venture Partners

Technical Lead - Functional Coatings @Earthodic

Building Decarbonization and Ops Technical Lead @Lawrence Berkeley National Laboratory

Reaction Engineer (Senior and above) @Ammobia

Analyst @Volta Circle

Senior Account Executive, UK Market Lead @Sumday

Analyst Intern - Summer 2025, Power & Renewables Investments @GE Vernova

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

New founder survey from Sightline Climate × Elemental Impact

Why dedicated water investors are building out a new asset class, with Burnt Island Ventures and Echo River Capital

Storage, satellites, and the SaaSpocalypse

Newsletter

Newsletter