🌎 Q1 2025 roundup: top deals, exits, and new funds

Investors hope to set off a chain reaction with new nuclear funding

What’s actually working while the rest of the climate capital stack stutters

As the federal government’s new deluge of directives floods the zone with noise, there's everything but clarity. We’ve heard from you that the continued fallout from the DOE funding freeze has thrown a wrench into financial plans. And we know it isn’t the friendliest VC fundraising season right now, either. We feel you — it's tough to make any plans in times of uncertainty.

For those pulling back from venture capital, now is the time to lean into working capital. Think of it this way: Venture capital is the fuel — it ignites the engine. Working capital is the thrust — it keeps you moving forward. That means liquidity management is as important as securing venture backing. Unlike SaaS startups with predictable revenue cycles and low overhead, climate companies often require real capital outlays, rely on partnership dependencies, and have long-term investment horizons for returns. The most capital-efficient companies are masters of blending distinct types of funding to meet different needs. In times of fluctuating federal funding and fleet-footed investors, the capital efficiency game ratchets up to a whole other level.

We’re here to break down what working capital is and the mechanisms to secure it, and provide some case studies of companies who have successfully navigated these questions in climate.

Special thanks to Dimitry Gershenson and the Enduring Planet team for championing the importance of this working capital slice of the climate stack and teamwork on this playbook.

There are countless types of financing instruments to secure working capital. Below, we'll decode the most common approaches and when the best time is to use them.

First, it's important to understand what working capital is. Simply put, working capital represents the funds a company has on hand to cover its short-term expenses (payroll, inventory, and day-to-day operations). It’s calculated as:

📊 Working Capital = Current Assets – Current Liabilities

If that number is positive, you have a cushion — you can pay employees, fund production, and invest in growth without scrambling. If it’s negative, you’re operating on borrowed time.

For climate tech, working capital is even more critical because:

🚀 Hardware & Deeptech (can) burn more cash – Unlike software, climate startups often need to finance physical assets (manufacturing, equipment, inventory). This means longer cash conversion cycles and higher upfront costs.

💰 Venture Capital won’t always save you – In a funding slowdown, relying on VC money for working capital can lead to dilution and loss of control. Remember: VCs bet on upside. Lenders hedge against downside. A strong financing strategy blends both perspectives.

🏗️ Scaling requires smart financing – As startups move from prototype to commercialization, they need capital-efficient strategies to fund production, sort supply chains, and achieve growth. Not all money is equal — securing the right financing mix is key to scaling while managing risk. The most successful climate startups balance funding sources to minimize dilution and maximize flexibility.

That means founders need to make the right money moves, and consider:

✅ Beyond VC: Equity is our most expensive option — how do we maximize other forms of capital while using it strategically?

✅ Capital stack strategy: What are we using the capital for, so we can match capital to risk, timelines, and outcomes?

✅ Long-term goals: How can we plan ahead knowing that lenders won’t back a company on the brink of running out of cash, and acquirers have more leverage with a low-runway company?

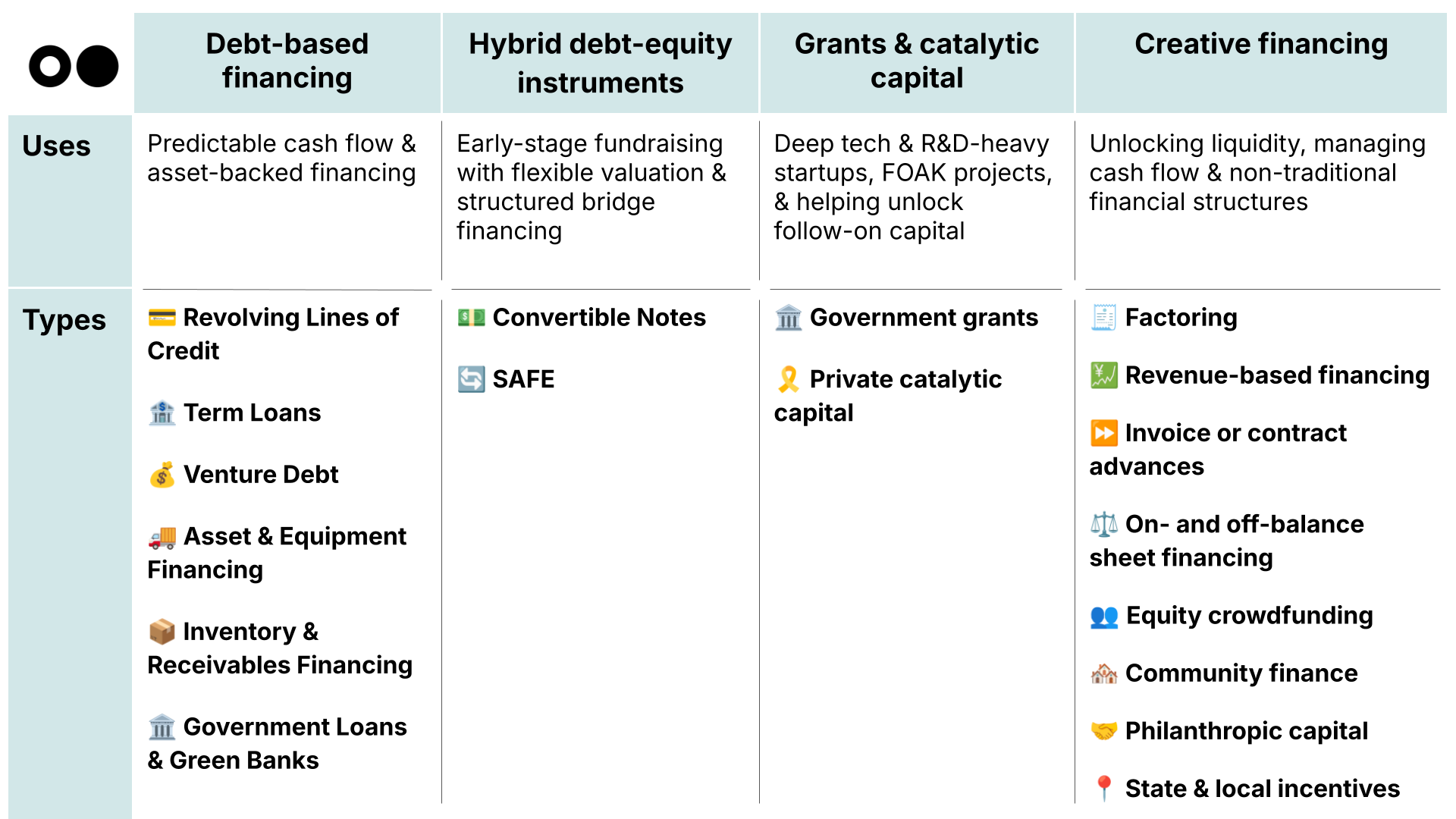

This is a non-exhaustive list of financing options available to climate startups. The right mix depends on your company’s stage, capital needs, and risk profile. Each funding source comes with trade-offs — understanding when and how to use them is key to capital efficiency.

A revolving line of credit functions as a flexible pool of capital that startups can draw from as needed and repay on a rolling basis. Unlike a term loan, interest is only paid on the amount used, making it a cost-effective way to manage short-term working capital needs. This is particularly useful for businesses with seasonal cash flow fluctuations, those waiting on invoice payments, or startups needing quick access to capital for short-term opportunities. However, credit lines often require a strong credit profile, may involve collateral, and can have variable interest rates that increase with market fluctuations.

✅ Pros: Flexible, quick access to capital, only pay interest on what you use.

❌ Cons: Can be expensive if rates rise, requires strong credit, may need collateral.

Good for: Working capital, managing uneven cash flow, short-term financing needs.

Providers: Traditional banks, fintech lenders, credit unions

A term loan provides a lump sum of capital that must be repaid over a set period with fixed or variable interest. These loans are ideal for startups with predictable revenue streams or credit-worthy contracts that need capital for specific projects such as scaling operations, purchasing equipment, or expanding production capacity. While term loans offer stability and structured repayments, they often require collateral or personal guarantees, making them less attractive for early-stage startups without significant assets.

✅ Pros: Fixed repayment schedule, lower interest rates than credit lines, good for scaling.

❌ Cons: Requires collateral or strong financials, less flexible, longer approval process.

Good for: Expansion, hiring, capex for scaling operations.

Providers: Banks, credit unions, green banks, the DOE Loans Program Office, and impact-specific programs like the LACI Cleantech Debt Fund, Kiva Capital, and more

Venture debt is a term loan designed for VC-backed startups that need additional capital without diluting ownership. Unlike traditional bank loans, venture debt lenders focus more on a startup’s growth trajectory and VC backing rather than profitability. These loans are often structured with warrants, giving lenders the right to purchase equity later. Venture debt also generally follows a recent funding round (completed within the preceding 6 months). Venture debt is ideal for startups looking to extend runway between equity rounds or finance large capital expenditures. However, if a company fails to hit growth targets, repayments can become a burden, potentially leading to financial distress.

✅ Pros: Minimal dilution, extends cash runway, aligns with VC-backed growth.

❌ Cons: Requires venture backing, includes warrants (potential future dilution), strict repayment terms.

Good for: Extending runway, bridge financing, post-Series A+ companies.

Providers: Large financial institutions, like HSBC Innovation Banking, Citizens Bank, NatWest, and Stifel

Asset and equipment financing allows startups to purchase expensive infrastructure, hardware, or machinery by using those assets as collateral. This method ensures that companies can scale operations without diluting equity. Since the loan is secured against the asset itself, interest rates are typically lower than unsecured debt. However, if the company defaults, the lender can seize the asset, making this risky if revenue projections do not materialize.

✅ Pros: Low-cost financing, preserves equity, spreads cost of major purchases over time.

❌ Cons: Asset can be repossessed if payments are missed, limited to tangible assets.

Good for: Buying equipment, vehicles, hardware, and production infrastructure.

Providers: Equipment leasing companies like CSC Leasing, plus banks and green banks

This type of financing allows startups to access capital by borrowing against unpaid invoices (accounts receivable financing) or unsold inventory. It is particularly useful for companies with long sales cycles or government contracts where payments can be delayed for months. However, lenders charge fees based on the risk of non-payment, and high borrowing costs can erode margins.

✅ Pros: Improves cash flow, fast access to capital, no dilution.

❌ Cons: Can be expensive, requires strong accounts receivable or inventory.

Good for: B2B startups with large purchase orders, government contractors.

Providers: Factoring companies, alternative lenders, invoice financing platforms

Government-backed loans offer lower interest rates and longer repayment terms than traditional bank loans. Programs like those from the DOE’s Loan Programs Office (LPO) and Small Business Administration (SBA) are designed to fund climate solutions, clean energy infrastructure, and industrial innovation. While attractive, these loans often have rigorous application processes and long approval timelines.

✅ Pros: Low-interest, long-term, supportive of climate projects.

❌ Cons: Lengthy application process, complex eligibility requirements.

Good for: Scaling infrastructure, clean energy projects, and industrial tech deployment.

Providers: US-based providers like the LPO, SBA, and state green banks, as well as UK-based DESNZ and EU-based EIB, among others

Convertible notes are short-term debt that automatically converts into equity at a future funding round, typically with a discount for early investors. This structure allows startups to raise capital quickly without setting a formal valuation. However, interest accrues, which increases dilution upon conversion.

✅ Pros: Fast fundraising, delays valuation, flexible for early-stage startups.

❌ Cons: Increases dilution upon conversion, interest accrual.

Good for: Early-stage fundraising, bridge rounds before priced equity rounds.

Providers: Angel investors, early-stage VCs, accelerators

SAFEs are founder-friendly agreements where investors provide capital in exchange for the right to future equity without accruing interest or having a maturity date. The D-SAFE (from Elemental Impact) can convert to debt or equity, making it a hybrid instrument and flexible alternative.

✅ Pros: No interest or maturity, simple structure, founder-friendly.

❌ Cons: Can result in higher dilution later, investors may demand valuation caps.

Good for: Early-stage fundraising with flexibility.

Providers: Y Combinator, Elemental Impact

There’s a lot of uncertainty around the availability and reliability of government grants right now. In general, they provide capital that does not need to be repaid, making them highly desirable. However, they come with strict usage requirements, detailed reporting, and long application processes. Those might be getting longer and more complex amid all of the changes in federal direction.

✅ Pros: No repayment, no dilution, credibility boost.

❌ Cons: Competitive, lengthy approval process, strict usage rules.

Good for: Technology development, pilot projects, and infrastructure buildout.

Providers: US-based agencies like DOE, ARPA-E, OCED, NSF, NREL, and state energy agencies, like NYSERDA; grant services organizations like Climate Finance Solutions and Streamline

Catalytic capital firms finance or enable early climate tech projects with dollars that seek a lower return on investment than typical VC or Growth. These funds prioritize impact over financial returns, accepting disproportionate risk and/or concessionary returns to support startups through funding gaps they might not otherwise overcome. It plays a critical role in de-risking first-of-a-kind (FOAK) projects, where technical or market uncertainty is high.

✅ Pros: No repayment, great for FOAK projects.

❌ Cons: Limited funding available, targeted toward specific missions.

Good for: De-risking first-of-a-kind (FOAK) projects, early-stage tech development.

Providers: Catalytic funds, like Breakthrough Energy Catalyst, Prime Coalition, and Elemental Impact; family offices, like Builders Vision and CREO Syndicate; and foundations, like Schmidt Family Foundation and Hewlett Foundation

🧾 Factoring – Sell unpaid invoices at a discount for upfront cash.

💹 Revenue-based financing (RBF) – Get an advance on projected revenue, repaid as a percentage of future sales.

⏩ Invoice or contract advances – Borrow against invoices from creditworthy customers, useful for long B2B/government payment cycles.

⚖️ On- and off-balance sheet financing – Structures that optimize debt without affecting core financials.

👥 Equity crowdfunding – Allows retail investors to fund climate startups (e.g., Raise Green, Wefunder).

🏘️ Community finance & co-ops – Shared ownership and investment models for mission-aligned climate solutions.

📍 State & local incentives – Tailored programs for clean energy deployment (varies by region).

🤝 Philanthropic capital – Awards from impact-focused nonprofits and foundations.

Remember: If the investment is risky, uncertain, or has a long payback period, equity and grants make sense. If it’s predictable, asset-backed, or revenue-generating, debt can be a smarter play.

Here’s a sample framework:

✅ Frontier R&D? → Grants or equity

✅ Uncertain investments (new hires, product development)? → Equity

✅ Predictable receivables (signed contracts, recurring revenue)? → Debt

✅ Physical assets (equipment, infrastructure, inventory)? → Asset-based lending

✅ High-margin revenue growth? → Equity or debt

Financing: Enduring Planet provided a grant advance to low-emissions material developer DexMat, allowing it to bridge funding gaps between grant awards and reimbursements.

Why creative financing: DexMat frequently secures grant funding, but upfront capital requirements can slow R&D and commercialization. The grant advance ensured uninterrupted operations without dilution or restrictive terms.

Result: The financing helped DexMat scale operations amid 25% YoY growth, meet customer demand, and accelerate commercialization without giving up equity or taking on personal guarantees.

Comment: This highlights how grant advances can be a critical tool for climate startups needing working capital while navigating capital-intensive R&D cycles. Non-dilutive capital solutions like this allow founders to maintain control while scaling.

Financing: HSBC Innovation Banking provided a $7m venture debt facility to fusion company Thea following its $20m Series A fundraise (2024) from Prelude Ventures and Lowercarbon Capital.

Why venture debt: Taking venture debt from a bank, as opposed to raising more capital through VC equity, allows Thea to raise further funds without dilution during development.

Result: Thea is taking a novel approach compared to many other stellarator developers. Rather than building the complex stellarator shape physically, they’re planning to create the shape within a magnetic field. This method could streamline engineering challenges and accelerate commercialization. The $7M venture debt facility provides critical non-dilutive capital to advance its technology without additional equity dilution, giving Thea the runway to validate its approach before seeking larger funding rounds.

Comment: Thea is still a long way from a commercial power plant. It may be hoping that if it can show its tech works in a test reactor, it will then be able to raise money more cheaply than it can now, making non-dilutive financing until then desirable.

Financing: BEV has three deals with Rondo; led $22m Series A (2022), followed in $60m Series B (2023), and $80m Project Finance (2024) for Rondo’s heat battery solution for industrial decarb.

Why catalytic capital: There’s massive potential for impact in industrial decarb, making Rondo's technology attractive. Plus, Rondo’s the first company to deploy a heat battery for this use case, making its FOAK too risky for many other investors.

Result: BEV’s ongoing support for Rondo helped it deliver its FOAK and move from early stage VC financing to Project Finance with the European Investment Bank.

Comment: This was one of BEV’s first deals of this type and where it developed its playbook for helping companies get past FOAK to start accessing Project Finance. Its ability to offer flexible types of financing (equity + project finance), hands-on support, and guidance seems to be the missing link in bringing Rondo’s technology to market.

You can read more in our climate capital stack report here, and if you have any creative financing case studies that we should know about for future newsletters, send them to [email protected].

Investors hope to set off a chain reaction with new nuclear funding

A Q&A with Precursor's David Yeh and Mark1's Julian Ryba-White, new strategic partners in the ecosystem

Announcing Sightline Climate's $5.5M Seed fundraise from Westly and Molten