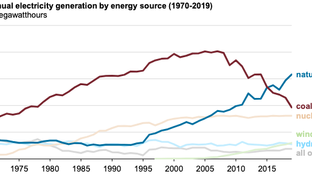

🌎 Coal hard facts #241

Trump’s coal push ignores economic reality and attractive alternatives

Ringing in the new year with fresh guidance on hydrogen, domestic manufacturing, and SAFs

Happy Monday! We’re back!

…We hope you didn’t miss our tax credit coverage ;) New year, new IRA guidance on hydrogen, domestic manufacturing, and SAFs. We breakdown who’s best positioned to tap the money pot. In other news, a major $11bn HVDC line between New Mexico and Arizona, new EV battery sourcing rules reduce eligible models, and BYD surpasses Tesla in EV sales.

In deals, $2.2bn in electric cars, $800m for Octopus’ expansion, and $34m for EVs in India.

Overwhelmed by your new year inbox and missed our Friday 2023 Investment Trends report? Be sure to skim here, or download it directly. Or if you’d rather that we read to you, save the date for Jan 25th and join us for a webinar on Sightline Climate’s 2023 investment trends, insights, and discussion.

P.S. We’re hiring for an Editor at Sightline Climate, apply here and DM us with folks we need to meet!

P.P.S. Thanks to your feedback, we’ll be publishing Features every other week. So crack those knuckles next for a deep dive on the 19th, where we’ll be publishing the results of the 2024 Climate Tech Oracle Survey. Put your 2024 predictions to the test here and see how you stack up.

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at [email protected].

💼 Find or share roles on our job board here.

December brought a flurry of Biden Administration and IRS definitions and rules for IRA tax credits. Each has its winners and losers, whose gripes and endorsements will echo throughout the proposals’ ensuing 60-day comment periods going on right now. Here are a few of the highlights and what’s needed for these credits to become effective climate tools.

On December 22nd, the Biden administration proposed long-awaited guidance for the 45V hydrogen production tax credit. The credit will range from $0.60 to $3.00 per kg depending on the production mechanism’s lifecycle emissions. Credit qualifications are based on “three pillars” of eligibility where projects must:

Lobbyists grappled over these three pillars throughout the drafting process, and their inclusion primarily decided which stakeholders came out on top.

Winners: Next generation, “smart” electrolyzers that can integrate seamlessly with intermittent renewable generation assets (e.g. Verdagy, Electric Hydrogen).

Losers: Existing electrolyzer manufacturers, primarily located in China, don’t have the operational flexibility to scale up and down in line with renewables. Industry incumbents like utilities, nuclear, hydro, and oil and gas with legacy energy production along with regions with little access to solar and wind may also be left in the cold.

Steps for success: Hydrogen transportation infrastructure out of renewables rich regions must scale quickly while hourly matching software will have to pick up the pace by 2028. The sleeper hit of the 45V rule is that it could set the foundation for a true 24/7 clean electricity market, and accelerate the infrastructure required to measure and track clean power on an hourly basis paired with locational-specific data (e.g. LevelTen, Granular).

Tax credit 45X, which received its guidance from Treasury and the IRS on December 15th, offers incentives for investments in domestic renewables manufacturing and critical mineral production. Credits cover inverter, solar, wind and battery technologies alongside 50 minerals.

Winners: Thermal batteries are included in the rules, indicating belief by the regulators that the technology has a role in economically decarbonizing hard-to-abate sectors (e.g. Antora, Rondo Energy). Transferability markets are responding positively. First Solar sold $700M of 45X credits just before the new year (e.g. Crux).

Losers: Long-duration storage startups that rely on geology or site-specific engineering may not qualify as the rule is angled towards factory-made, manufactured products.

Steps for success: 45X was already responsible for $80bn of new renewable manufacturing infrastructure before the new guidance. It remains to be seen whether new guidance will be enough to wrestle sector dominance away from international players like China, especially in solar and minerals processing.

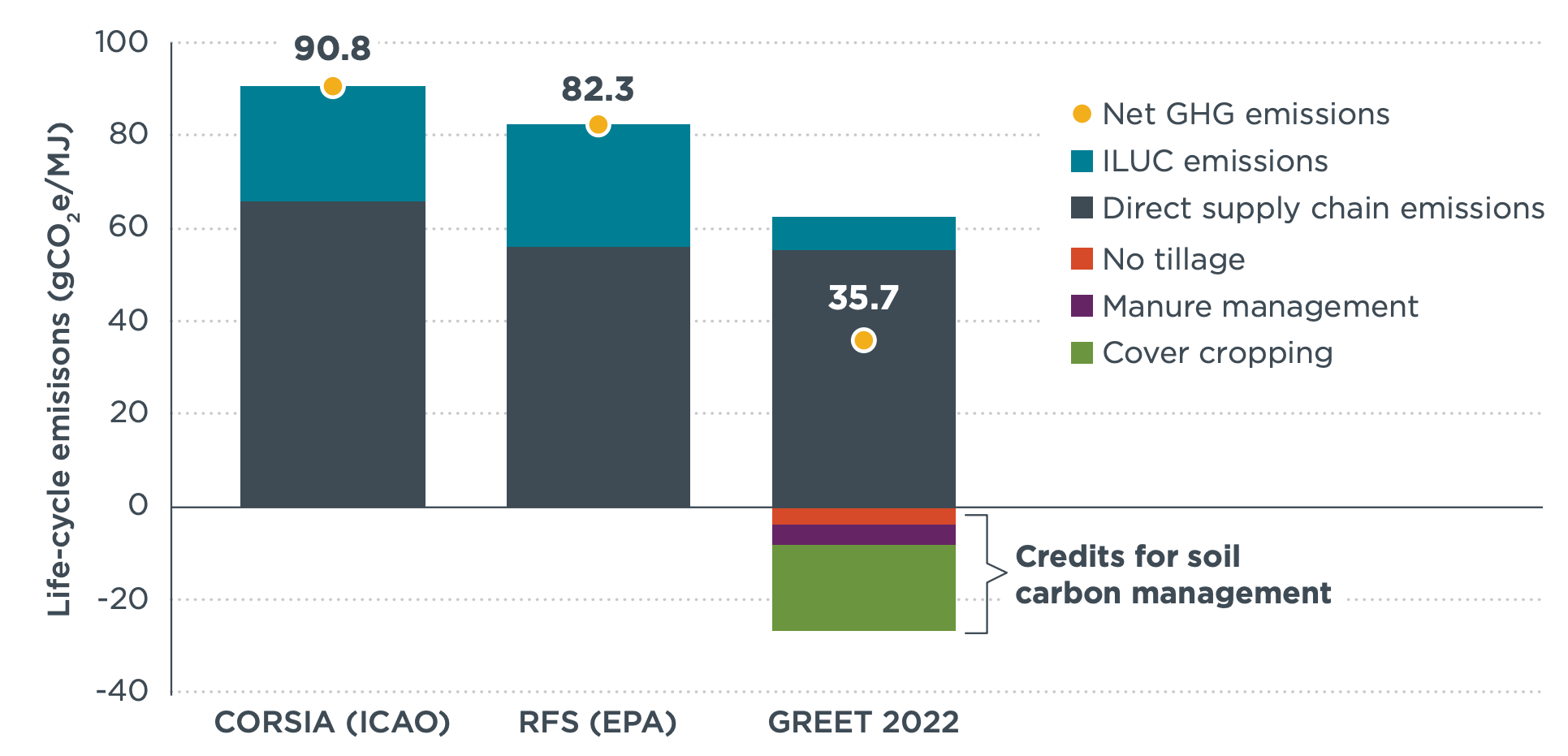

The Biden Administration released guidance for sustainable aviation fuel tax credit 40B, also on December 15th. Eligible fuels must produce lifecycle greenhouse gas emissions at least 50% below those of traditional jet fuels. The tax credit offers a credit of between $1.25 and $1.75 per gallon of fuel, based on life cycle emissions calculated using the Department of Energy's GREET model.

Winners: The aviation industry, whose net zero goals will rely heavily on SAF development, could see their ESG ratings take flight. Technology companies developing new fuels approved by the EPA Renewable Fuel Standard now fall under the tax credit umbrella (e.g. Lanzajet Freedom Pines) and corn ethanol-to-jet aviation fuels are evaluated more favorably under the GREET model to meet the qualification threshold.

Losers: Environmentalists worry the credit guidelines will make soybean- and corn-based fuels newly eligible for SAF credits. Some studies show such fuels decrease crop diversity and questionable climate credentials.

Steps for success: Regulators are making the bet that ethanol and soy-based fuels are climate positive. Either novel fuel technologies will have to win out or the government’s thesis will have to pan out for 40B to be considered a success.

Special credit to James Prussing from Boundary Stone for his tactful tax takes.

⚡Octopus Energy Group, a London, UK based energy company raised $800m from Origin Energy, Tokyo Gas, Canada Pension Plan Investment Board (CPP Investments), and Generation Investment Management.

🌾NewLeaf Symbiotics, a St. Louis, Missouri based bio agriculture company, raised $45m in Series D funding from Gullspång Re:food, Otter Capital Partners LP, S2G Ventures, Leaps by Bayer and others.

🚗 RevFin, a Delhi, India-based eV lending platform, raised Rs 92.3 crore ($11m) in Series B funding from Omidyar Network, with Asian Development Bank and Green Frontier Capital.

🏗 Lingrove, a San Rafael, California-based sustainable composite materials company, raised $10m in Series B funding from Lewis & Clark Agrifood, Diamond Edge Ventures, Bunge Ventures and SOSV.

⚡Sweetch Energy, a Rennes, France-based osmotic energy company, raised €25m ($27.3m) in Series A funding from Révolution Environnementale et Solidaire, Demeter Investment Managers, Go Capital, Positive Future Capital, and CNR.

🛵 BluSmart Mobility, an Ahmedabad, India-based electric ride hailing company, raised $24m in funding from BP Ventures and Survam Partners.

🌾 Agtonomy, a San Francisco, California-based software and services provider for autonomous agriculture, raised a $22.5m Series A from Momenta, Doosan Bobcat North America, and Toyota Ventures

🛵 Swap, a Jakarta, Indonesia-based swappable batteries for e-motorcycles company, raised $22m in Series A funding from Qiming Venture Partners, GGV Capital, and Ondine Capital.

🛵Ampersand, a Kigali, Rwanda based battery-swapping motorcycle startup, raised $12m in equity funding from Ecosystem Integrity Fund, Acumen, and Hard Edged Hope Fund and $7.5m in debt from Africa Go Green Fund.

⚡ SolarDuck, a Rotterdam, Netherlands-based solar developer, raised €15m ($16.4m) in funding from Katapult Ocean, Green Tower, Energy Transition Fund Rotterdam and Invest-NL.

🌍Future, a Silver Springs, Maryland-based climate-focused fintech startup, raised $6.5m in Seed funding.

⚡Green Eagle Solutions, a Madrid, Spain-based automation software developer for the renewables sector, raised in €6m ($6.6m) Series A funding from Spanish private bank A&G, Kibo Ventures, and SET Ventures.

✈️Cloudline, a Cape Town, South Africa-based aerospace startup, raised $6m in Seed funding from Schmidt Futures, Raba Partnership, Verod-Kepple Africa Ventures, and 4D.

🔋BatX Energies, an India-based lithium battery recycling company, raised $5m in Seed funding from Zephyr Peacock, Lets Venture, Family Office of Mankind Pharma, and JITO Angel Network.

📦Friendlier, a Toronto, Canada-based reusable packaging company, raised $5m in a Seed extension from Relay Ventures and Garage Capital.

⚡Suena, a Hamburg, Germany-based energy-trading services provider, raised €3m ($3.3m) in Seed funding from Santander InnoEnergy Climate Fund, Energie 360, EIT InnoEnergy, Raakwark Kaptaal, and Business Angels.

⚡AEInnova, a Barcelona, Spain-based wireless IoT company, raised €3m ($3.3m) in Series A funding from the European Innovation Council (EIC) Fund.

🏠 Lumian, a Beşiktaş, Turkey-based ioT-based energy management company, raised $3.2m in Seed funding from DOMiNO ventures.

🏭 LivNSense, a Bengaluru, India-based industrial AI platform solutions company, raised $2.8m in Seed funding from Pavestone Technology Fund.

☁️Excarta, a San Mateo, California-based AI weather prediction company, raised $2.5m in Seed funding from Village Global, Ubiquity Ventures, and Converge VC.

🚗BRUDELI, a Hokksund, Norway-based electric truck startup, raised NOK€15.3m ($1.5m) in Seed funding from Hexagon Composites ASA and Leax Group AB.

🚗 Munro Vehicles, a Scotland, UK-based electric SUV maker, raised £1m ($1.3m) in Seed funding from Elbow Beach Capital, a London-based investment firm.

🌾 Fasal, a Bengaluru, India-based smart farming technology company, raised an undisclosed amount of Series A funding from TDK Ventures and British International Investments.

⚒️ Element3, a Fort Worth, Texas-based critical material extraction technology company, raised an undisclosed amount of Seed funding from EIC Rose Rock.

🚗Nio, a Chinese electric car maker, raised $2.2bn in strategic investment from Abu Dhabi-backed fund CYVN.

Vast Renewables, a Sydney, Australia-based concentrated solar energy developer, completed its SPAC merger with Houston-based Nabors Energy Transition Corp, at a valuation of $9.1bn.

New Era Helium, a Midland, Texas-based helium exploration and production company, agreed to go public via SPAC via Roth CH Acquisition V at an implied valuation of $90m.

Sennen, a Bristol, UK-based energy asset operation management software provider, was acquired by Kraken, a software provider part of Octopus Energy Group.

Unico Solar Investors, a Seattle, Washington-based solar energy solutions provider company, was acquired by Altus Power.

Diagram, a Montreal, Canada-based venture builder, secured C$50m ($37.3m) for a new fund targeting innovation in the climate tech industry.

Cambia Capital, a Seattle, Washington-based sustainability-focused real estate investment firm, launched with a $20m investment.

MOL Switch, a Palo-Alto, California-based fund announced the launch of a new $100m fund to invest in decarbonisation technologies.

Can’t get enough deals? See full listings and deal analytics on Sightline Climate

Kicking off the new year with new transmission, an $11bn investment was made into SunZia Transmission, a 550-mile ± 525 kV high-voltage direct current (HVDC) transmission line between New Mexico and Arizona with the capacity to transport 3,000 MW across the Western US. This monumental project represents one of the first and largest new HVDC lines in the US.

The US treasury unveiled new battery sourcing requirements for the EV tax credit, aimed at weaning the U.S. electric vehicle supply chain away from China. The new guidelines slashed the list of qualifying EV models from 43 to 19, with notable models from Tesla, Nissan, and GM on the chopping block.

BYD overtook Tesla for the first time, on par with our prediction back in October. In Q4’23, BYD outpaced Tesla with 526K new EV sales compared to Tesla's 484K, mostly driven by robust expansion in foreign markets.

Continued tailwinds and headwinds for offshore wind. Vineyard Wind, the first commercial-scale offshore wind farm in the US, produced power for the first time last week and Orsted received the green light via a final investment decision on what would be the world’s largest offshore wind farm in the North Sea. Meanwhile, Equinor and BP were forced to dump yet another offshore wind project, citing economic changes across the industry.

Just before the new year, First Solar sold $700m of 45X credits for 96 cents on the dollar. This is the first significant tax credit transfer of its kind in the solar manufacturing industry, and came weeks after the IRS finalized guidance on transferable credits, pointing to a huge year for the transferability market in 2024. [Read more about transferability here].

Meanwhile, solar equipment manufacturer, Enphase, cut 10% of its staff and closed multiple factories across the country. High interest rates and California’s new net metering policy led to a significant drop in rooftop solar demand and forced Enphase to shutter a number of facilities.

The UK is instituting its own version of CBAM, following in the EU’s footsteps. However, the UK’s policy won’t go into effect until 2027 unlike the EU CBAM which entered into effect last October. The UK’s policy excludes electricity generation, but includes ceramics and glass which the EU does not.

ADNOC doubled down on hydrogen and ammonia with a $3.6bn deal to acquire Fertiglobe, the leading exporter of ammonia by sea, in a bid to dominate the growing clean ammonia market, which is poised to serve as a crucial shipping fuel and mode for transporting clean hydrogen.

Another state-owned enterprise, China's State Power Investment Corp (SPIC) announced a $6bn investment to generate SAF and Methanol from wind power and expects first fuel from their pilot by late 2025. China also just assembled the Nuclear Fusion dream team in the global quest to commercialize fusion energy.

Energy Fuels opened three new Uranium mines in the US driven by surging uranium prices, now reaching more than $80 per pound for the first time in over fifteen years.

Following the COP28 Sultan Al Jaber controversy, Azerbaijan named COP29 President, Mukhtar Babayev, an oil veteran who spent nearly three decades in state oil company Socar.

Wildlife photos of the year are out! We’re partial to fireflies and spores.

Reflect forwards by looking backwards with MIT Tech Review’s 6 takeaways from Cleantech 1.0.

WSJ calls belly up in 2023 for at least 18 EV startups on a cash crunch collision course.

This 1908 electric car review is too much…

More projects, more interactive maps of clean tech projects.

Spice! Iran’s desert gold Saffron supply dwindles thanks to climate change.

Meanwhile, Australia’s booming water trade leaves wells dry in favor of crops, and California quenches thirst with recycled wastewater.

Floating FOAK, the next frontier for North Sea wind?

Too big to fail? Great Lake goldfish.

Prolific Swedes top Sifted’s European climate tech review.

70% of US wind power blows in Red states, with real implications for the ’24 election.

Itsy Bitsy Teenie Weenie, UK’s first DAC machine.

📅 Sightline Climate: Investment Trends 2023 Webinar*: Join us on Jan 25th to hear about Sightline Climate's Investment Trends 2023 analysis, insights, and predictions for the year ahead.

📅 Blue Tech Happy Hour: Attend SF Blue Tech’s happy hour on Jan 10th to interact with other passionate individuals interested in improving our ocean and waterways.

💡 Sustainability Open Innovation Challenge: Apply to SOIC to develop sustainable solutions across various sectors within climate change by Jan 31st.

📅 FusionXInvest: Attend FusionXInvest from Feb 21st-22nd to learn about milestones and investment opportunities within the fusion energy industry.

Editor @Sightline Climate

Senior Cloud Software Engineer @Quilt

Director of Finance @Infravision

Grants & Contracts Lead @Pioneer

Natrium Market Strategy MBA Intern @TerraPower

Program Manager, Climate Operations @Google

Sr. Associate, Structured Investments & Tax Equity @Generate Capital

Communications Manager @Carbon Removal Alliance

Summer Associate, Regenerative Agriculture @Rockefeller Foundation

Visiting Partner @Gigascale Capital

📩 Feel free to send us deals, announcements, or anything else at [email protected]. Have a great week ahead!

Trump’s coal push ignores economic reality and attractive alternatives

The tariffs' toll, explained sector-by-sector

The AI company’s debut shows where the chips are falling

Newsletter

Newsletter