Welcome to CTVC’s first long-form feature of 2025! Expect to see us in your inbox as usual every Monday and every other Friday. If you have any feature ideas or requests for us this year, feel free to reach out to [email protected].

You've seen our 2024 Investment Trends report looking at the current state of climate tech. This week, we’re hopping into our time machine and taking a look at the past — and the future — of climate tech.

It’s been a minute since we sent out our Climate Tech Oracle survey, asking you to gaze into your crystal balls and help us predict what 2025 has in store. It’s been even longer since we asked you to do the same for 2024. We asked, and more than 300 of you delivered! We've got a packed newsletter for you with:

What you’re predicting for 2025 — We sifted through your 2025 Climate Tech Oracle survey answers and collectedyour predictions for what’s in and out this year.

How your 2024 predictions performed — At the end of 2023, we asked you to send in your predictions for 2024. We’re comparing your answers with how the year actually went. Make sure you get to the bottom of this newsletter to see the results!

Before diving in, mark your calendars for our upcoming webinar on Thursday, January 23, where we'll share key insights from the reports and our outlook for 2025. Register here.

Climate Tech Ins and Outs for 2025

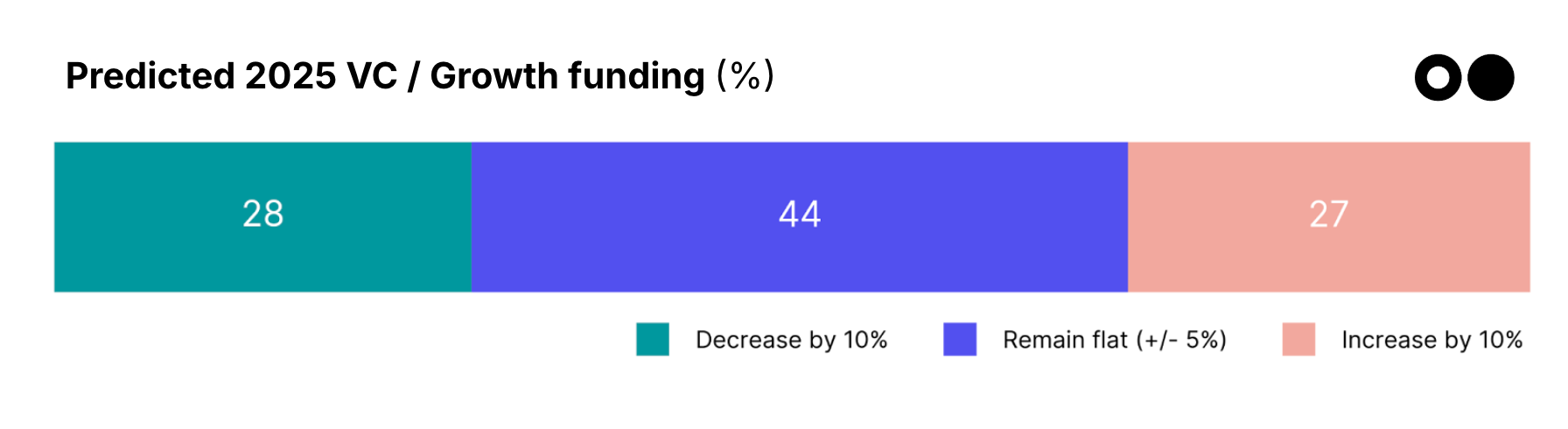

What will happen with climate tech venture / growth?

Venture and growth investment totaled $30bn in 2024, down 14% from 2023 — a smaller decrease than the previous year’s 24% drop. What’s next?

Source: Sightline Climate

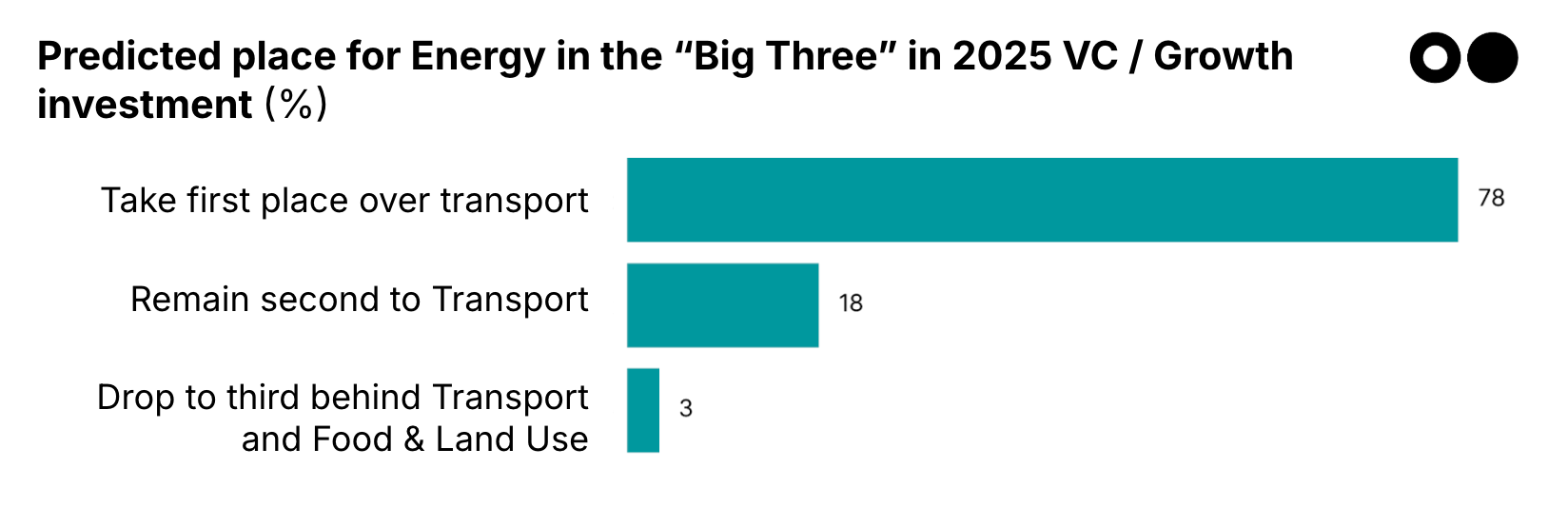

How will Energy VC / Growth investment rank in the “Big Three”?

The “big three” verticals — Transport, Energy, and Food & Land Use — have always made up the majority of funding for climate tech (~80% of investment). For the first time in the last five years, Energy overtook Transport as the most-funded vertical in 2024. Can it continue?

Source: Sightline Climate

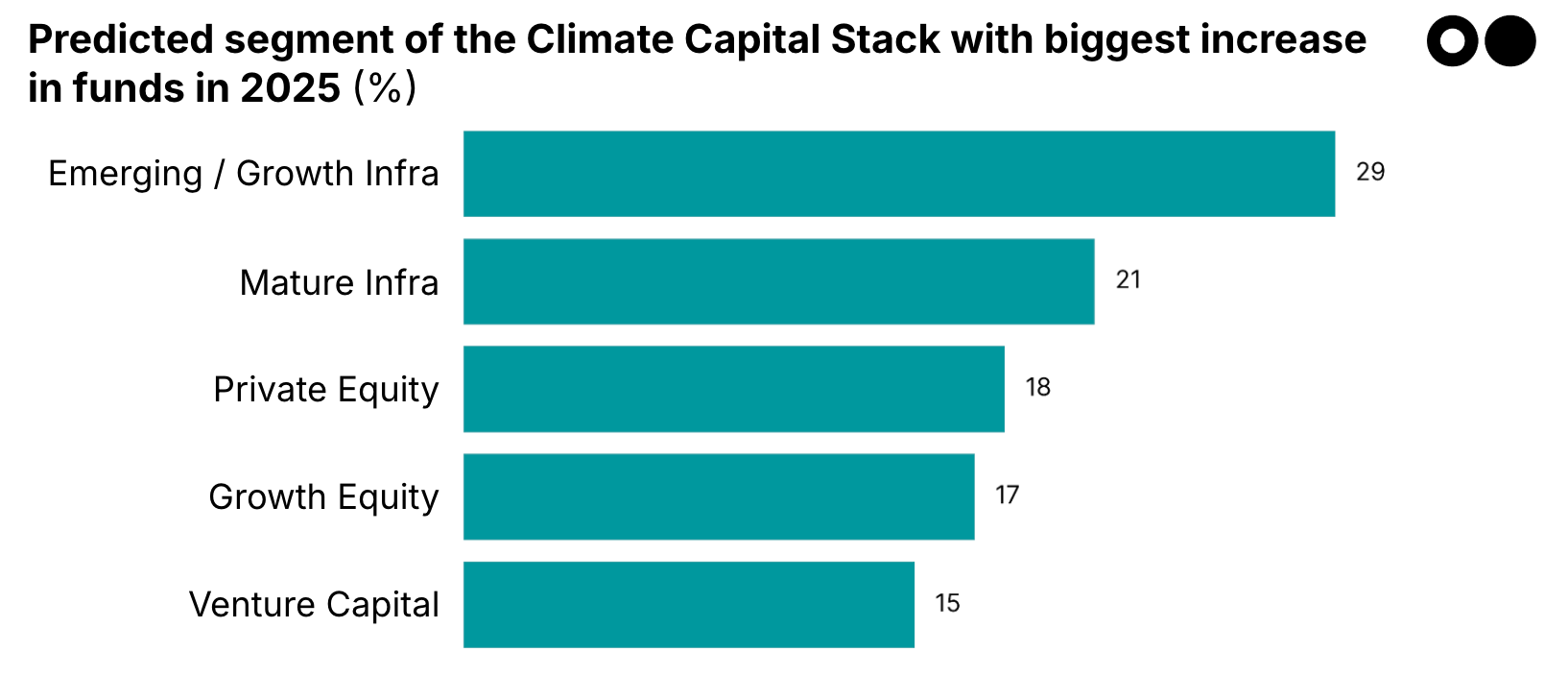

Which segment of the Climate Capital Stack will see the largest increase in funds raised?

As the capital stack for climate tech matures, you all expect the later-stage segments to play a bigger role in the year ahead. In 2024, the stack of investable dry powder accumulated to $86bn, and Infrastructure funds made up almost 60% of the new climate AUM raised over the year. You expect that to continue, with a special nod to Emerging and Growth Infra to (hopefully!) meet that missing middle.

Source: Sightline Climate

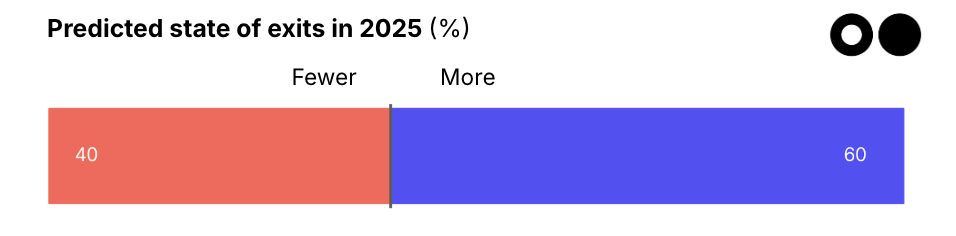

Will exits increase or decrease?

Exits surged 136% in 2024, driven by acquisitions, which made up 92% of all exits and hit a record high, though most were undisclosed, confirming a buyer’s market with more tuck-in acquisitions.

Source: Sightline Climate

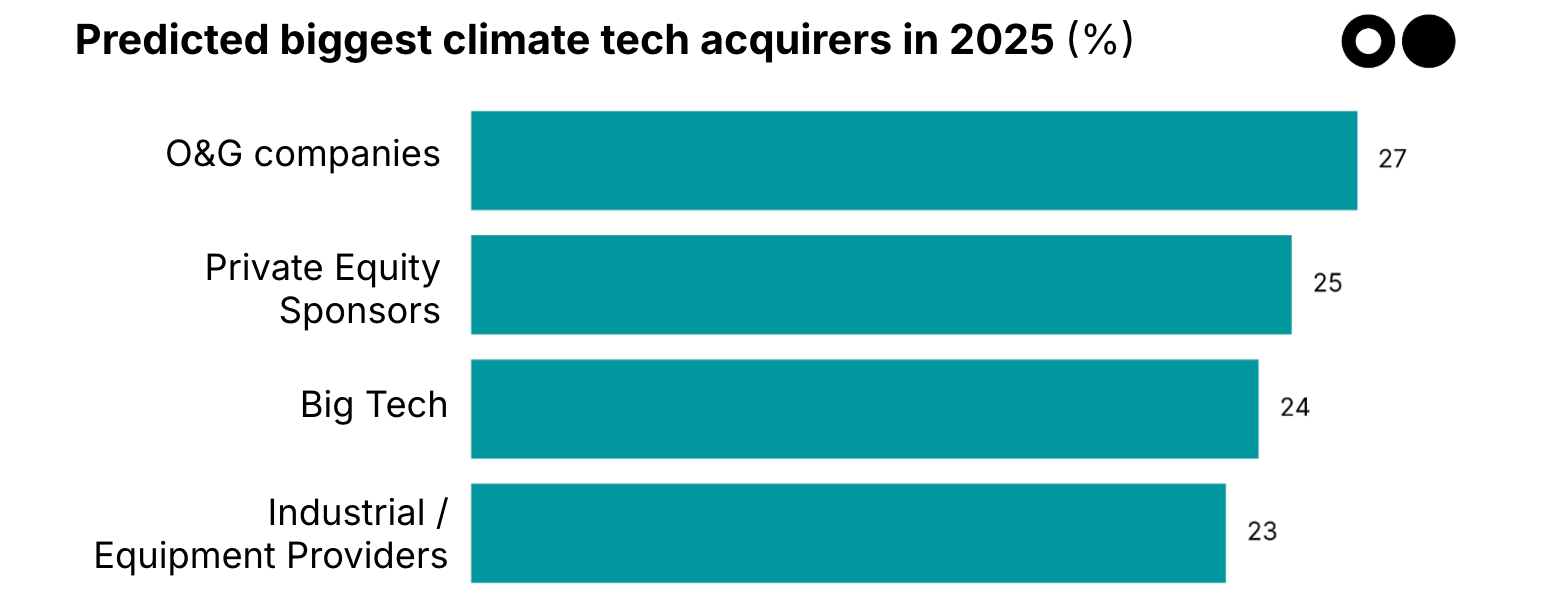

Which types of companies will be the most active climate tech acquirers?

In terms of acquisitions, 2 out of the 3 most active acquirers in climate tech since 2021 have been O&G companies. In 2024, that number dropped to 3 out of 5.

Source: Sightline Climate

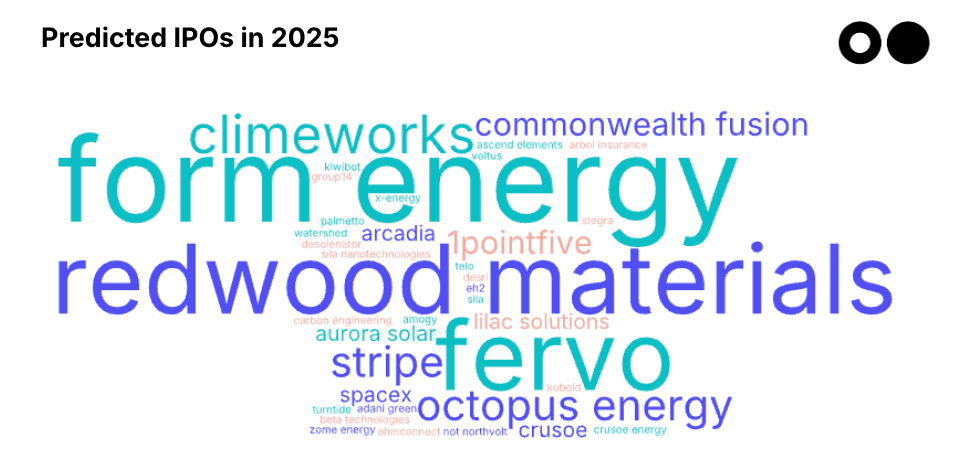

Which company is most likely to IPO?

IPOs rose slightly to 6 from 5 in 2023 but remained below 2020-2021 levels, with two large IPOs in India. Here’s who you think is next.

Source: Sightline Climate

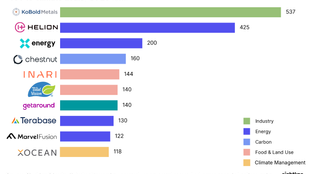

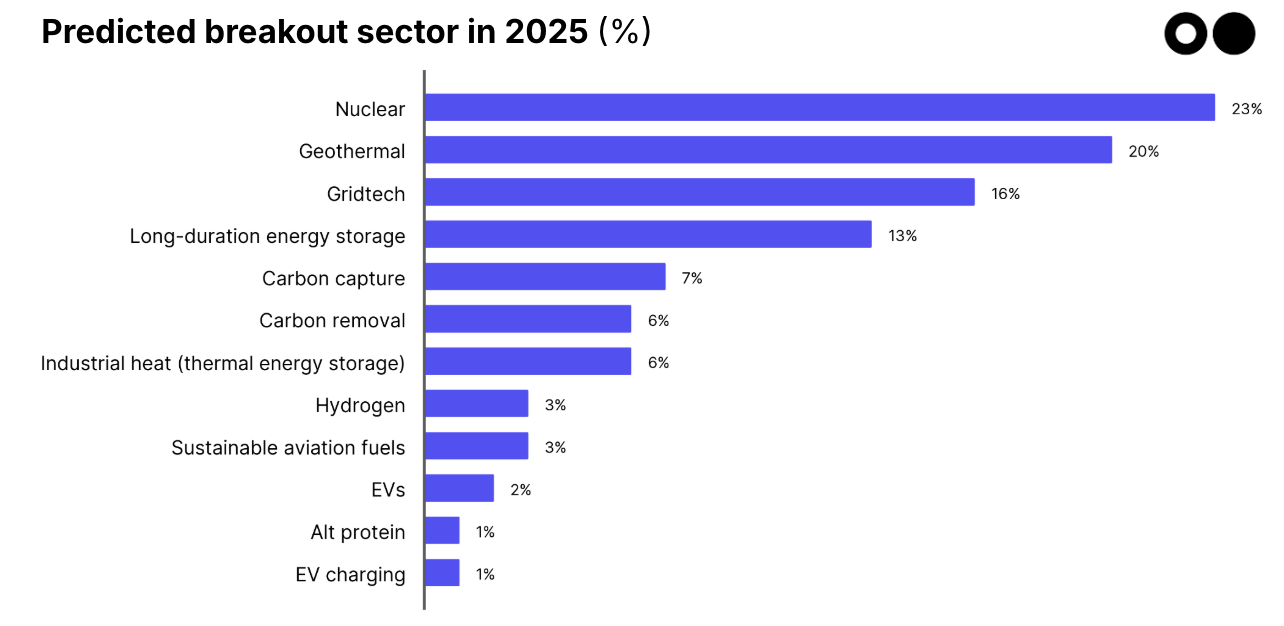

Which sector will break out?

In 2024, new VC/growth investment sectors emerged: Geothermal nearly tripled ($558m) and nuclear almost doubled ($1.9bn). Aviation and low-carbon fuels quadrupled. Mega-deals focused on clean firm power and data centers, with standout deals for SMR company X-energy and LDES startup Form Energy.

Source: Sightline Climate

You gave us some reasons for your choices, saying that nuclear energy is gaining traction as a reliable, green baseload option to power energy-intensive sectors like AI, with global momentum from countries like China and increasing regulatory support. Geothermal energy has been benefiting from innovations in drilling and heat extraction, as well as legacy oil and gas expertise transitioning to renewable applications. Gridtech could also expand as utilities and governments prioritize grid modernization to support renewable integration and improve resilience, with bipartisan backing and high spending forecasts.

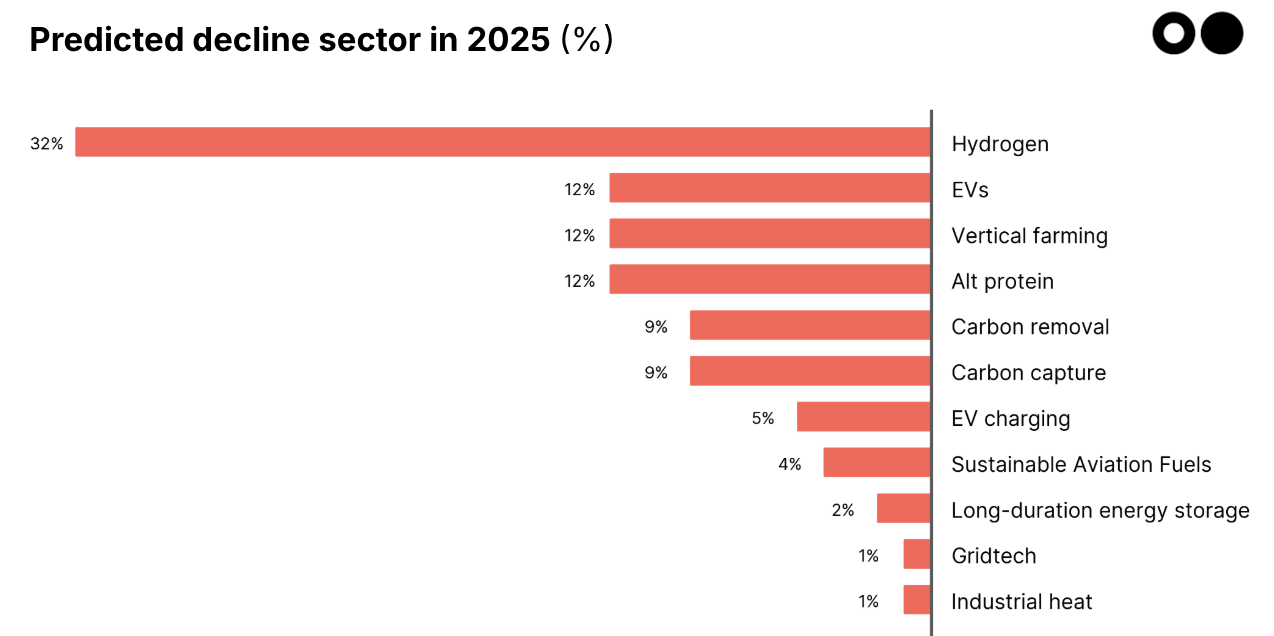

What sectors will decline?

The funding freeze hit some sectors hard in 2024: Battery investments (in Transportation) plummeted 79%, from $6.2bn to $1.3bn. In Industry, steel funding nosedived 80%, from $1.9bn to $0.4bn, while mining & metals fell 74%, from $0.8bn to $0.2bn.

Source: Sightline Climate

Your reasoning here? For hydrogen, overreliance on government funding, unclear business models, high costs, and skepticism about its scalability. You also noted vertical farming's struggles with high energy intensity, low ROI, and competition from subsidized traditional agriculture. Carbon removal and carbon capture technologies are seen as underdeveloped, costly, and heavily reliant on policy incentives, with market adoption progressing slowly.

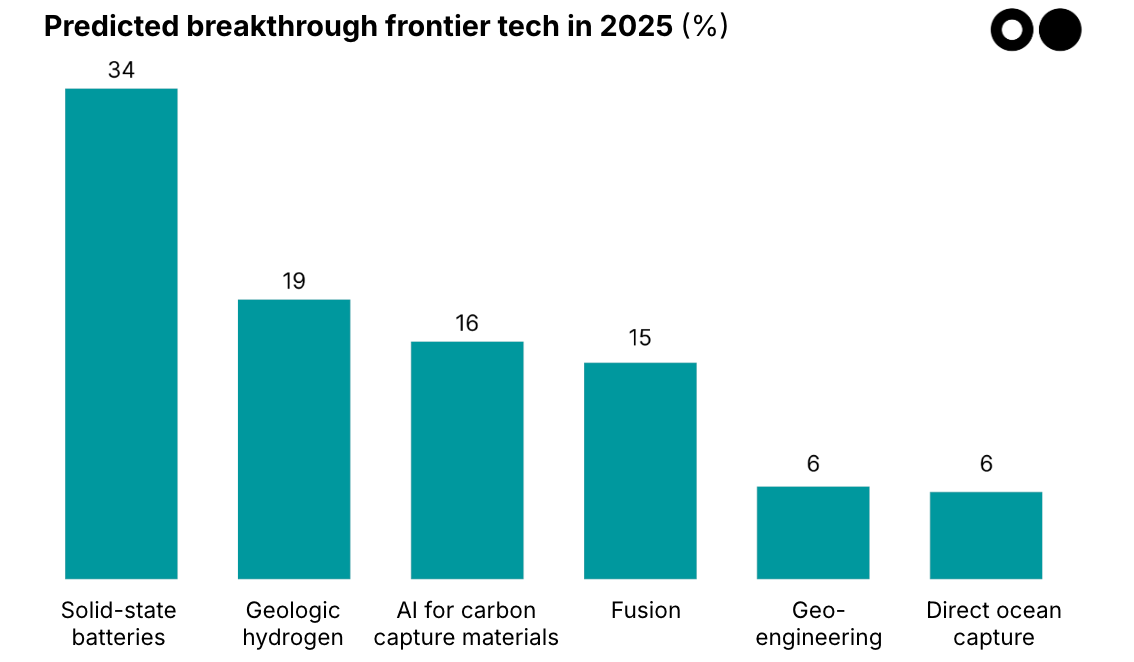

What frontier tech will achieve a breakthrough?

Source: Sightline Climate

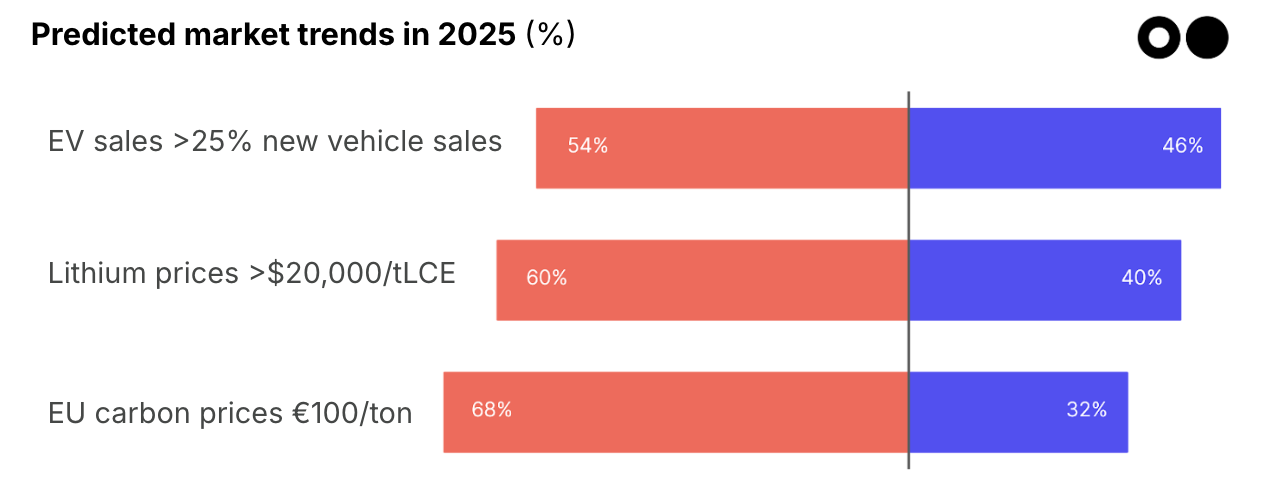

What is the market for solutions? Will EV sales reach 25% of global new car purchases? Will lithium prices end above $20,000/tLCE? Will EU carbon prices break €100/ton?

Building markets for emerging climate tech is no easy task. Here’s what you expect about a select few markets.

Source: Sightline Climate

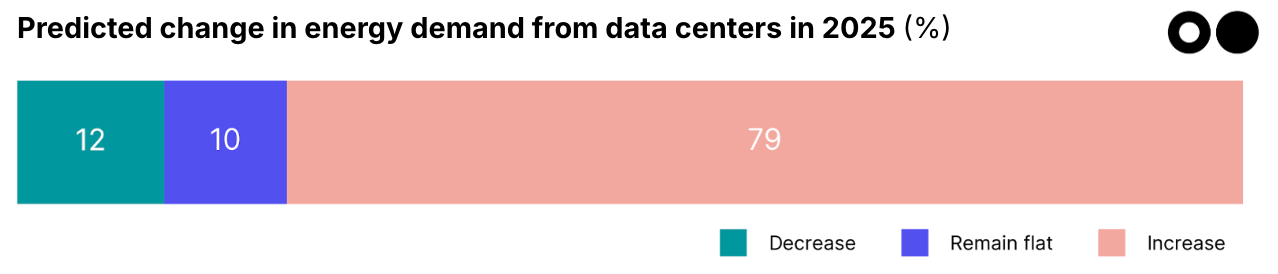

Will energy demand forecasted from data centers increase or decrease?

AI and “the electrification of everything” drove up demand for energy, especially reliable, 24/7 clean energy in 2024. Forecast power demand from data centers, for instance, has been revised up significantly in recent years (the IEA’s 2024 forecast was for 800 TWh in 2026 – up from 460 TWh in 2022).

Source: Sightline Climate

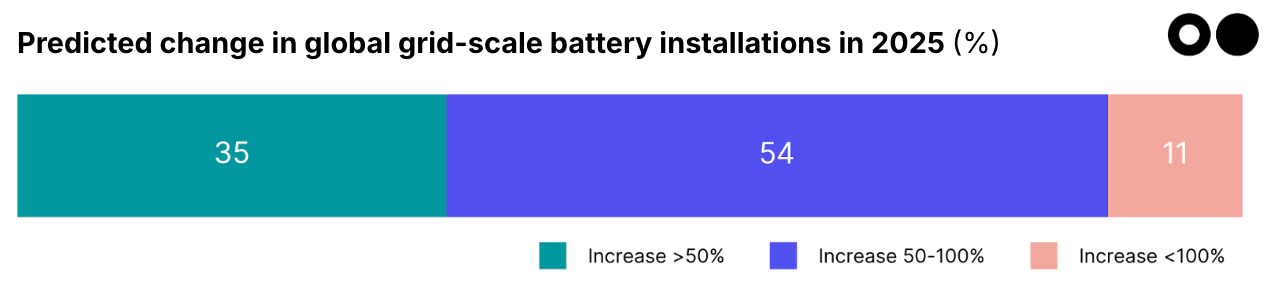

What will global grid-scale battery installations do in 2025?

At the end of 2023, the world had approximately 56 GW / 200 GWh of grid-scale battery storage installed, up from just 3 GW 5 years ago. 2024 was an even bigger year, and here's what you see next.

Source: Sightline Climate

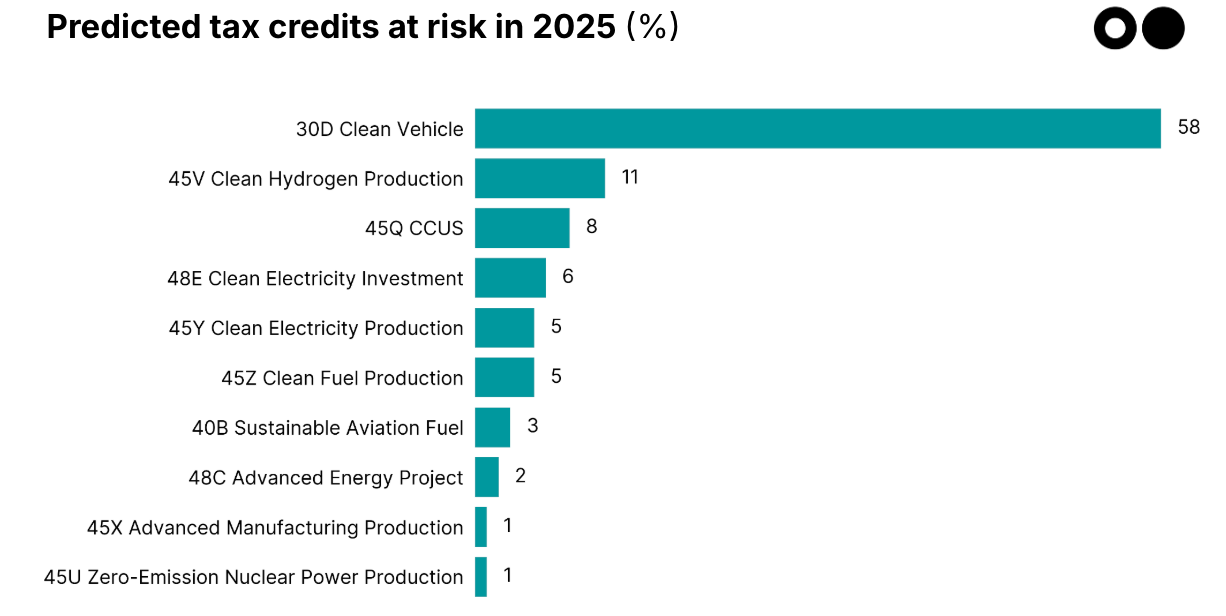

Which tax credit is most likely to be repealed?

Trump’s inauguration is next week, and questions remain around if/how his administration might target clean energy incentives from the IRA that have boosted investment.

Source: Sightline Climate

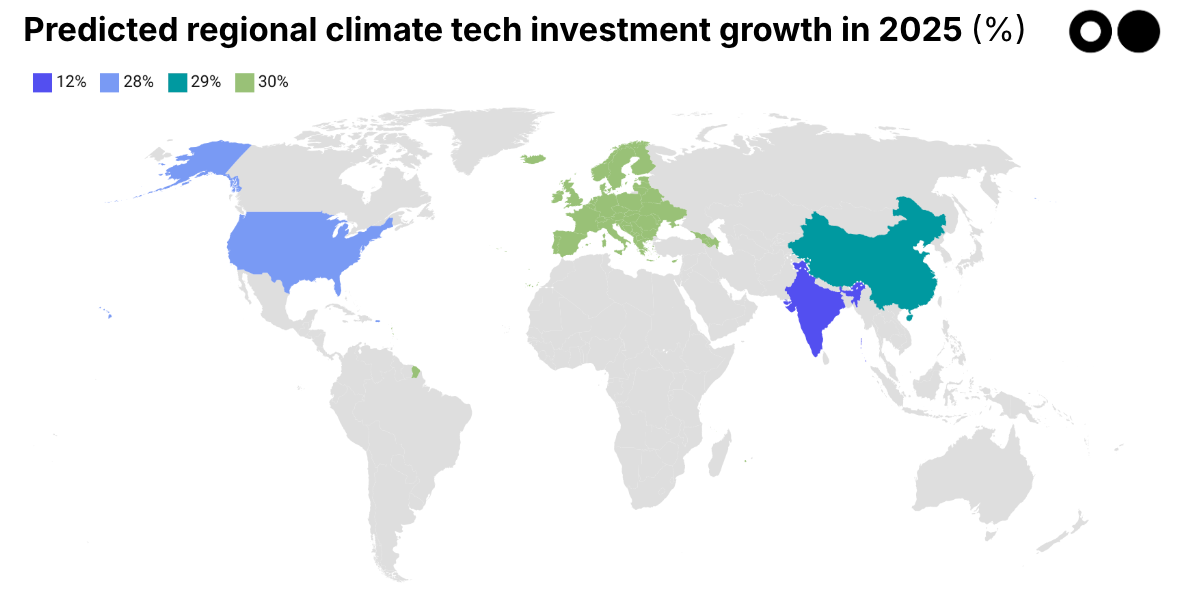

Which region will see the fastest climate tech investment growth?

The climate tech story is different around the world, as the European startup gap vs. the US shrank significantly, with a 62% rise in new companies fueled by government innovation funding last year. Plus, in Asia in 2024, India dominated with 38% of regional startups, while China saw 152% investment growth. And in South America, Brazil had the biggest % rise in investment, up 187% in 2024 (among countries with over $1bn in cumulative climate tech funding).

Source: Sightline Climate

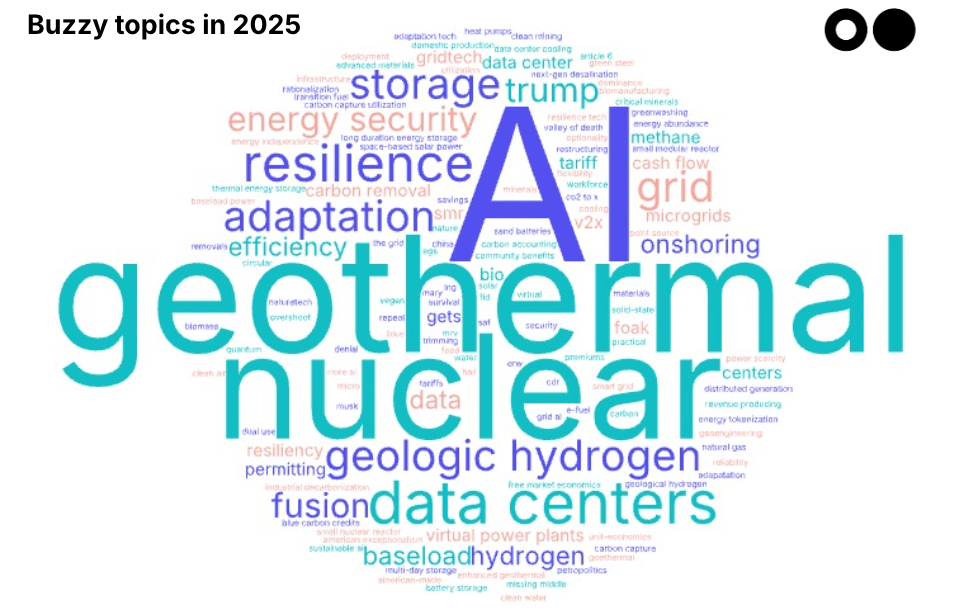

Wildcard! What’s the climate tech buzzword of 2025?

Source: Sightline Climate

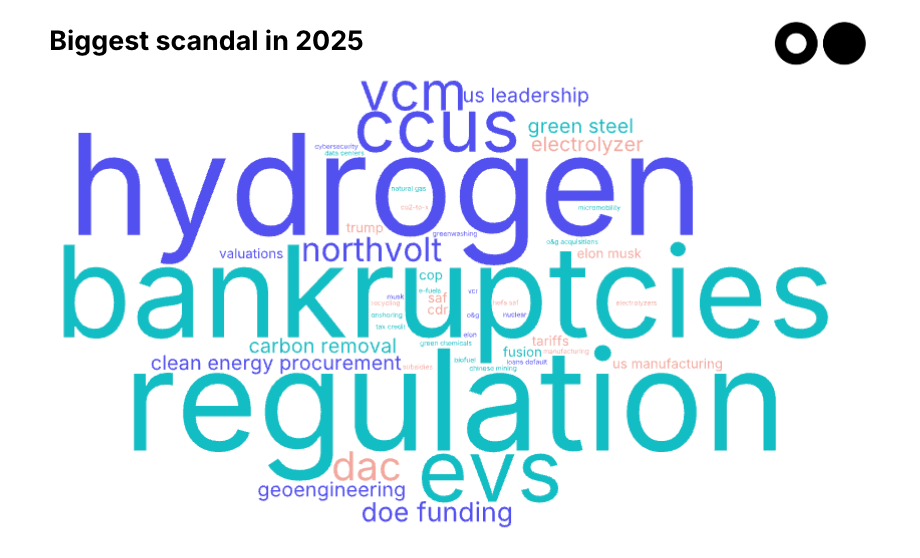

What will be the biggest failure or scandal in climate tech?

Source: Sightline Climate

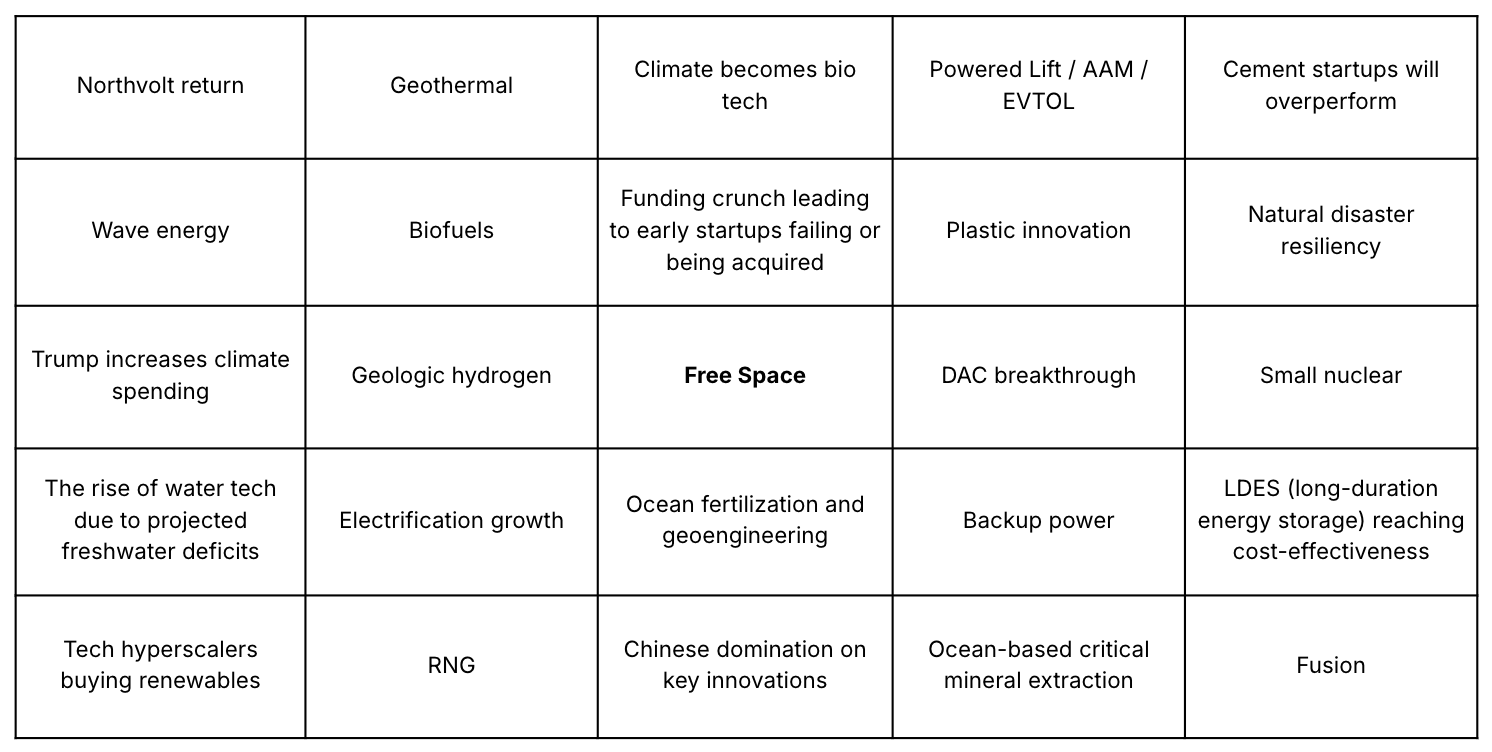

What’s not on anybody’s 2025 bingo card — your most unexpected prediction that everyone else is missing?

Your 2024 predictions: The results are in

How did your 2024 predictions turn out? Well, most of your guesses were pretty evenly split, but we're going to grade based on the majority answer. You got 60% correct — not too bad!

1. Will climate tech venture/growth funding increase?

Prediction: An overwhelming 89% believed funding would rise in 2024, citing expectations of falling interest rates, supportive policies, and sustained public interest in climate issues. The 11% who disagreed pointed to political instability and the lure of AI as potential drags on investment.

Outcome:Wrong. Climate tech funding fell 14%, contrary to optimistic predictions. The macroeconomic pressures of high interest rates, delayed IRA funding rollouts, and geopolitical uncertainties created significant headwinds. The "wait-and-see" investor crowd from 2023 held back, stalling the anticipated restart in 2024. However, it wasn’t all doom and gloom — climate tech increasingly relies on more mature types of funding.

2. More flat/down rounds in climate tech in 2024?

Prediction: 54% said yes, expecting a reset in 2024, guessing high valuations in 2023 would course-correct due to sustained high interest rates. Meanwhile, 46% trusted in "climate exceptionalism" and rate cuts.

Outcome:Correct. Average deal size dropped 14% to $23.6m in 2024, although results by stage are mixed (Seed and Series B rounds saw growth, although Series B deal sizes are being distorted by IM Motor’s $1.1bn raise).

3. Oil & gas companies as top climate tech acquirers, maintaining status as top 2 out of 3 climate acquirers from 2021-2023?

Prediction: With 51% voting "Yes," the razor-thin majority anticipated O&G companies would remain dominant, to diversify revenue streams or reinforce their fossil fuel capabilities. The other 49% argued that high oil prices would incentivize these companies to double down on their traditional business rather than embrace climate tech.

Outcome:Correct. Oil and gas companies continued to position themselves as major players in the energy transition. In 2024, three of the five most active acquirers of climate tech start-ups came from this sector.

4. US election signaling IRA incentive changes?

Prediction: 61% predicted change, hinging on potential Trump policies.

Outcome:Unclear, but likely. As of today, with the Trump administration not yet in power, it all remains speculative. It’s likely that some pieces of the IRA are targets, but we will see (and CTVC will be tracking).

5. Will the S&P Global Clean Energy Index return to above $1,200?

Prediction: At the start of 2024, 58% of readers expected the index to bounce back, driven by optimism around falling interest rates and cheaper financing for green infrastructure. The 42% who were skeptical pointed to persistent high rates and political uncertainty as barriers to a rebound.

Outcome: Wrong. The index climbed to$961 by May, a notable improvement but still far from the $1,200 mark.

6. Voluntary carbon market shrinking?

Prediction: After a turbulent 2023 for the $2B VCM, 41% predicted contraction, citing exposed flaws in carbon offset projects and a loss of trust. Some of these skeptics saw a potential for future growth, but only after significant restructuring. Meanwhile, 59% argued that the market’s troubles would lead to a "flight to quality," with better standards and more robust projects emerging, ensuring its resilience.

Outcome: Wrong. The size of the global carbon credit market remained relatively flat in 2024, according to industry reports, with credit demand relatively similar to that of 2023.

7. Direct Air Capture (DAC) under $600/ton?

Prediction: Only 37% expected this announcement in 2024, split between those optimistic about readiness and those doubting viability. The majority (63%) thought the technology wasn’t ready, though breakthroughs might come within a few years.

Outcome:Commercially, yes, technically, no. Holocene signed a deal with Google for credits at $100 per ton, though scalability remains uncertain. Climeworks maintained current costs at $600 per ton, with plans to reach $100 per ton by 2025-2030. But these are pre-purchase agreements, and costs remain high as of today.

8. EV sales hitting 25% of global car sales?

Prediction: 44% saw supportive policy and infrastructure tipping sales upward, while 56% cited supply chain and cost barriers. (In 2022, 14% of all new cars sold were electric, up from 9% in 2021 and less than 5% in 2020.)

Outcome:Correct. It was close, but no cigar.EV research firm Rho Motion reports global EV passenger car and light-duty vehicle sales (including plug-in hybrids) rose 25% over the year to reach 17.1 million in 2024, a new annual record. Different totals of global car sales are reported, so estimates of EV proportions are tricky. but they come in around 20-22%.

9. New geologic hydrogen production sites?

Prediction: Interest in geologic hydrogen extraction grew in 2023, buoyed by $20M in US DOE funding and venture-backed startups like Koloma. While 46% believed a project launch was possible in 2024, many doubted its relevance, citing the rarity of the resource. The majority (54%) argued that the timelines were too long, noting that key projects, such as Utah’s, are years from completion, with targets set for 2027-2028.

Outcome:Correct — no production sites reported. Interest grows, but timelines remain long.